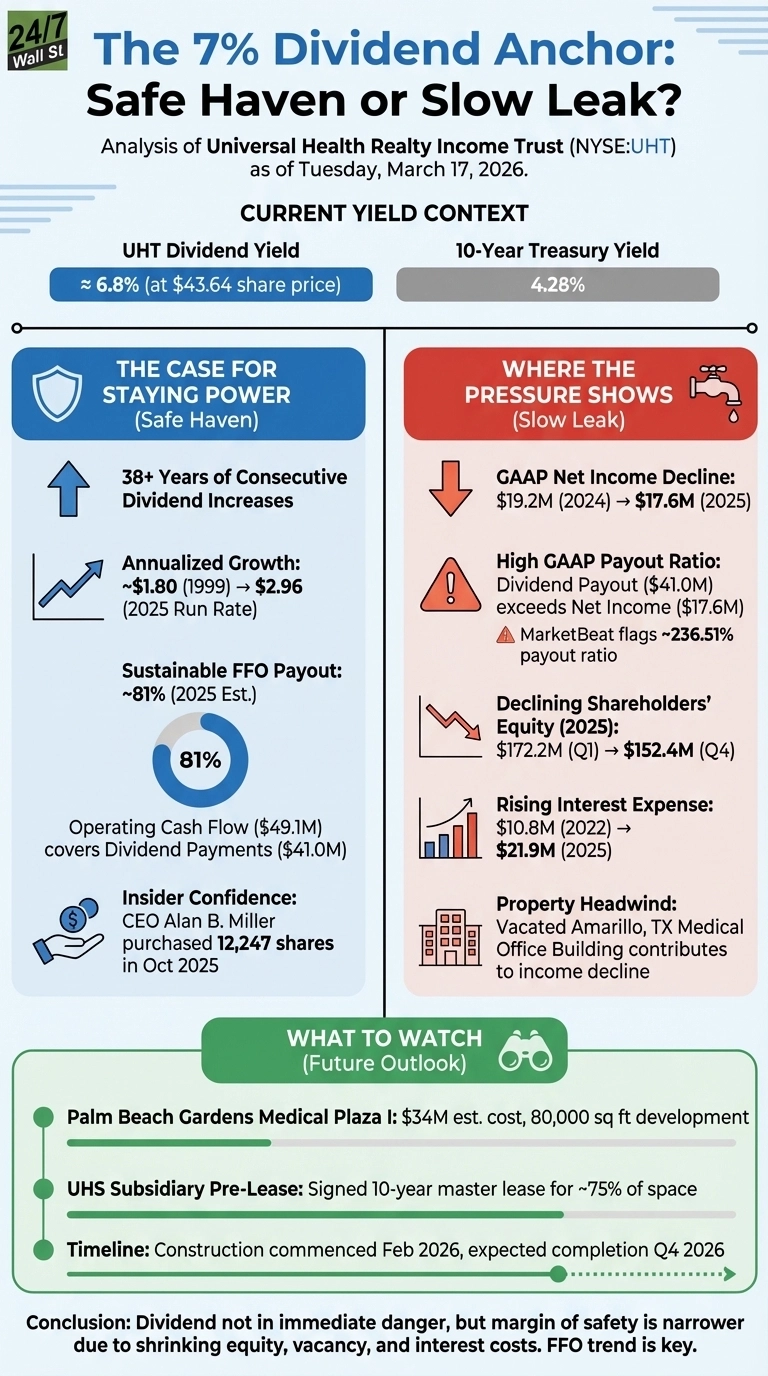

Universal Health Realty Income Trust (NYSE:UHT) has delivered an unbroken streak of quarterly dividend increases spanning over three decades. That dividend yields roughly 6.8% at the current share price of $43.64. Against a 10-year Treasury yield of 4.28%, that spread looks compelling. The harder question is whether the income is as durable as the track record implies.

The Case for Staying Power

It should go without saying that the dividend history is genuinely remarkable as UHT has paid a higher dividend every single year since at least 1999, growing from roughly $1.80 annualized to a current run rate of $2.96 per share. The most recent increase, announced December 10, 2025, moved the quarterly payout from $0.74 to $0.745. Small, but consistent.

The more relevant sustainability metric for a REIT is funds from operations, not GAAP earnings. On that basis, the picture is reassuring. The FFO payout ratio for 2025 is expected to be around 86%, and the full-year operating cash flow of $49.1 million covered $41.0 million in dividend payments at a ratio of 83.6%. That is not a company on the edge of a cut.

CEO Alan B. Miller reinforced confidence with action: he purchased 12,247 shares in October 2025, bringing his stake to 182,104 shares. Insiders buying near multi-year lows is a signal worth noting.

Where the Pressure Shows

The GAAP view is less comfortable, as net income fell from $19.2 million in 2024 to $17.6 million in 2025, while the dividend payout consumed $41.0 million over the same period. This gap largely results from non-cash depreciation charges, which is why MarketBeat flagged a payout ratio of 236.51% as a sustainability concern. For investors who prioritize net income over cash flow, these optics create a difficult narrative despite the underlying strength of the funds from operations.

Shareholders’ equity has declined every quarter in 2025, falling from $172.2 million in Q1 to $152.4 million in Q4. Cumulative dividends are outpacing retained earnings, steadily eroding book value.

The Amarillo, Texas, medical office building sits empty after both tenants let their leases expire, contributing to a 7.2% year-over-year decline in Q4 net income. Meanwhile, interest expense has surged from $10.8 million in 2022 to $21.9 million in 2025, a structural drag that does not disappear quickly even as the Fed has held rates at 3.75%.

What to Watch

The Palm Beach Gardens Medical Plaza I project, an 80,000-square-foot development with an estimated cost of $34 million, broke ground in February 2026 and targets a Q4 2026 completion. A UHS subsidiary has already signed a 10-year master lease covering roughly 75% of the space, limiting leasing risk. Assuming this project delivers on schedule, it adds a meaningful revenue stream at a time UHT needs it.

Thankfully, the dividend and its streak of increasing are not in immediate danger. But with shareholders’ equity shrinking, a vacant Texas property, and elevated interest costs, the margin of safety is narrower than the 38-year streak might suggest. The FFO trend and the Amarillo re-leasing timeline are the key metrics that will determine whether the dividend streak continues into 2027.