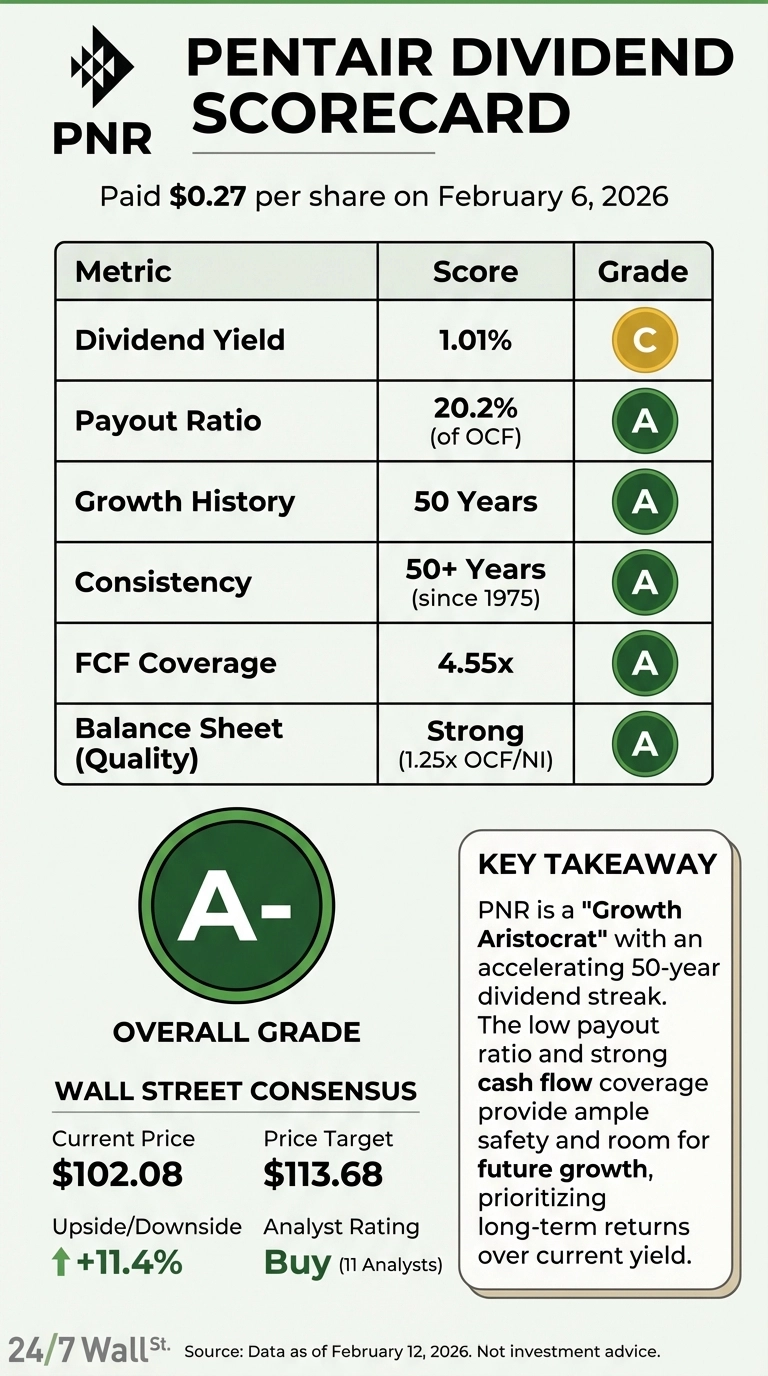

Pentair plc (PNR) delivered its latest quarterly dividend of $0.27 per share on February 6, 2026, marking another milestone in a streak that now spans 50 consecutive years of annual dividend increases. At a current price of $102.08, the water treatment specialist offers a modest yield that reflects its growth-oriented profile rather than income maximization – but the dividend’s rock-solid foundation and accelerating growth rate tell a more compelling story than the headline number suggests.

The Dividend Scorecard: Quality Over Quantity

PNR’s current quarterly dividend of $0.27 translates to an annualized payout of $1.08, producing a yield of approximately 1.01% at today’s share price. That’s well below the yields offered by traditional dividend aristocrats like Johnson & Johnson (2.16%) and Procter & Gamble (2.63%), and even trails 3M’s 1.68%. But yield alone misses the point.

What matters is the trajectory. Pentair raised its dividend 8.0% in early 2026, following an 8.7% increase in 2025. That’s meaningful acceleration compared to the mid-single-digit increases typical of mature dividend payers. Johnson & Johnson, for instance, raised its dividend 4.8% in 2025, while Procter & Gamble delivered a 5.0% increase. Even 3M’s recent 6.8% bump—coming off a lower base after dividend policy adjustments—doesn’t match PNR’s recent momentum.

Cash Flow Coverage: Room to Run

The sustainability picture is equally impressive. Pentair generated $814.8 million in operating cash flow for fiscal 2025, while paying out just $164.3 million in dividends. That’s a payout ratio of 20.2% of operating cash flow—exceptionally conservative by any standard. Even after accounting for $68.8 million in capital expenditures, free cash flow of $746.0 million covered the dividend 4.55 times over.

Compare that to Johnson & Johnson’s 50.5% payout ratio or 3M’s earnings-based concerns (net income declined 19.9% year-over-year while maintaining a $2.92 annual dividend). Pentair’s cushion provides not just safety, but flexibility to continue aggressive dividend growth without sacrificing reinvestment in the business or share repurchases (the company bought back $225 million worth of stock in 2025).

Earnings Quality Supports the Story

The cash flow strength is backed by improving profitability. Pentair posted net income of $653.8 million in fiscal 2025, up 4.5% from the prior year, on revenue of $4.18 billion. Operating margin expanded to 20.5%, and the company’s operating cash flow to net income ratio of 1.25x indicates strong cash conversion with minimal working capital strain.

The company’s recent Q4 results support the momentum. Adjusted EPS of $1.18 beat estimates of $1.17, while revenue of $1.02 billion matched expectations. More importantly, segment performance showed balanced strength: the Flow segment grew 9%, Pool jumped 11%, offsetting a 10% decline in Water Solutions.

Total Return Context: Growth Plus Income

The modest yield becomes more attractive when paired with capital appreciation potential. Over the past five years, PNR shares have returned 103.18%, doubling investors’ money. That compares favorably to Johnson & Johnson’s 68.0% five-year return and Procter & Gamble’s 43.58%.

The stock has faced near-term pressure—down 1.73% year-to-date and off 0.87% over the past month—but that creates entry opportunities for investors who understand the underlying fundamentals. At a forward P/E of 18.87x against 2026 EPS guidance of $5.25 to $5.40, the valuation is reasonable for a company delivering high-single-digit dividend growth and double-digit earnings growth potential.

The 50-Year Streak in Context

Pentair’s half-century dividend growth streak places it in elite company. From a quarterly payment of $0.08 in 1999 to today’s $0.27, the company has delivered 237.5% total growth over that period alone. The dividend survived the 2008 financial crisis, the pandemic, and various business restructurings—including a notable 2018 policy adjustment that didn’t break the growth streak.

What’s particularly encouraging is the recent acceleration. After years of 3-5% annual increases, the company shifted into a higher gear in 2024-2025, suggesting management’s confidence in the business trajectory and commitment to returning more cash to shareholders.

The Verdict: Growth Aristocrat, Not Income Play

Pentair’s dividend profile won’t satisfy investors hunting for maximum current income. Realty Income’s monthly payments of $0.27 (totaling $3.24 annualized) deliver three times PNR’s annual payout at a similar share price. But that comparison misses the fundamental difference in business models and growth potential.

PNR offers something more valuable for long-term investors: a sustainable, accelerating dividend backed by conservative payout ratios, strong cash generation, and improving profitability. The 50-year growth streak isn’t just a historical achievement – it’s a forward-looking signal. With operating cash flow covering dividends nearly 5x over and management guiding toward continued earnings growth, the company has ample room to maintain its recent 8% annual dividend growth rate.

For investors willing to accept a 1% starting yield in exchange for reliable growth and capital appreciation potential, Pentair’s dividend scorecard earns high marks. The latest $0.27 payment isn’t the largest check in the dividend aristocrat universe, but it’s one of the most dependable and fastest-growing.