Berenberg analyst Michael Filatov initiated coverage of Mobileye Global Inc. (Nasdaq: MBLY | MBLY Price Prediction) with a Buy rating and $9.30 price target, calling the company the “dominant” global supplier of technology and software for camera-based advanced driver assistance systems. The initiation arrives as MBLY stock trades near multi-year lows, giving long-term investors a potentially compelling entry point into a name with deep technology roots and a growing pipeline.

So far this year, shares of MBLY down 34.33%, but on Wednesday the stock rallied 7.35%.

| Ticker | Company | Firm | Action | Old Rating | New Rating | Old Target | New Target |

|---|---|---|---|---|---|---|---|

| MBLY | Mobileye Global Inc. | Berenberg | Initiation | N/A | Buy | N/A | $9.30 |

The Analyst’s Case

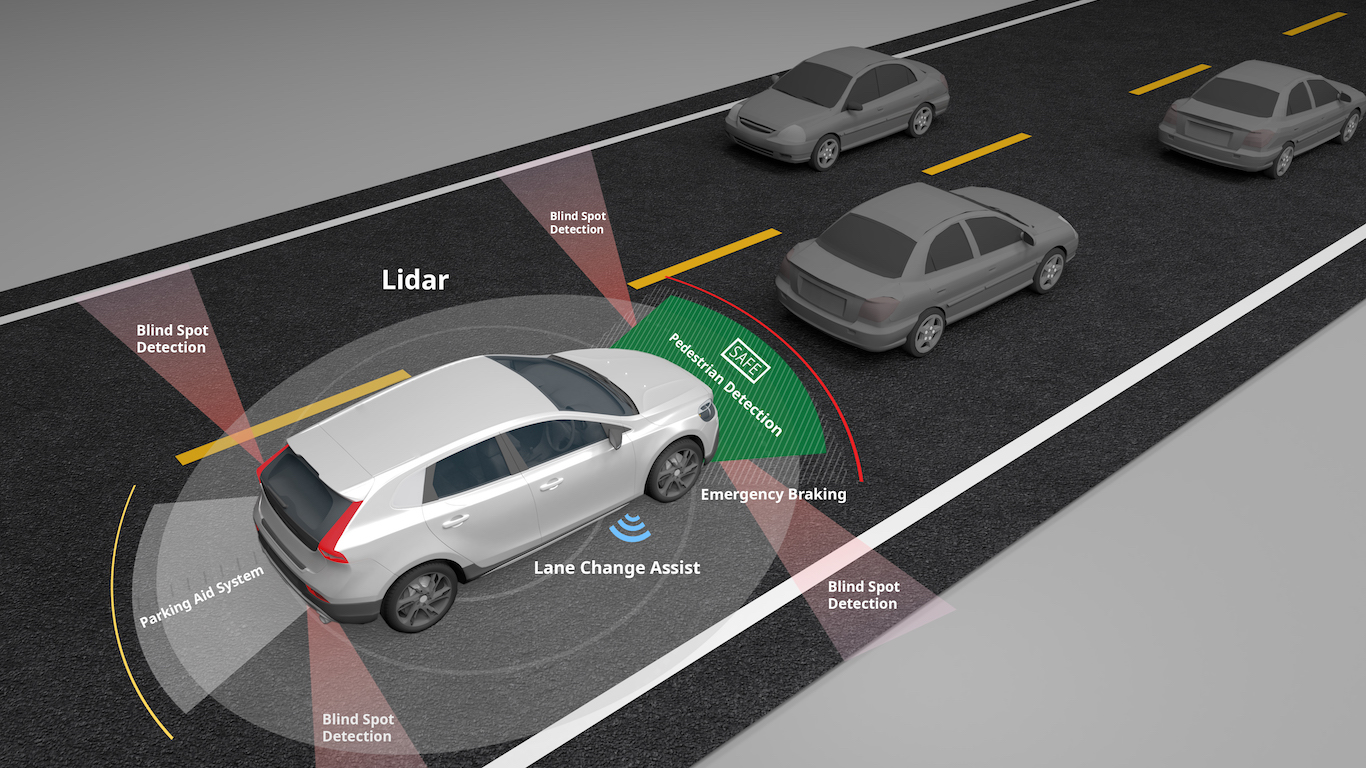

Filatov’s core thesis centers on Mobileye’s structural leadership in the high-volume L2-L2+ ADAS category, where OEMs are prioritizing cost, efficiency, and scale. Berenberg believes the company is well positioned to win additional awards in this segment, reinforcing its dominant market standing. With more than 230 million vehicles worldwide built with Mobileye’s EyeQ technology through 2025, the installed base alone underscores the company’s entrenched position across global automakers.

Supporting the bull case, Mobileye’s 8-year future expected automotive revenue pipeline stands at $24.5 billion, up 42% since year-end 2022. The company added two new OEMs to its customer base in 2025 and recorded follow-on wins with all top-10 customers, signaling broad commercial momentum.

Company Snapshot

Mobileye develops ADAS and autonomous driving technologies anchored by its EyeQ family of system-on-chip processors and the SuperVision hands-free driving system. The company reported full-year 2025 revenue of $1,894 million, up 15% year-over-year, with operating cash flow of $602 million, up 51% year-over-year. The balance sheet remains solid, with cash and equivalents of $1,836 million. Intel retains majority ownership following the 2022 IPO, a governance factor investors should weigh.

Why the Move Matters Now

MBLY shares have been under significant pressure, falling -34% year-to-date and -52% over the past year. The stock currently trades around $7.14, well below its 52-week high of $20.18. Berenberg’s initiation at Buy signals conviction that the selloff has been overdone relative to the company’s long-term positioning. The 2026 revenue guidance of $1,900-$1,980 million with Q1 2026 growth expected at approximately 19% year-over-year suggests a potential reacceleration ahead.

What It Means for Your Portfolio

For retirement-focused investors, Mobileye stock presents a classic risk-reward tension. The GAAP operating loss of -$440 million in FY2025 and persistent unprofitability are real concerns, as are geopolitical risks tied to the company’s Israel-based operations. The planned $612 million acquisition of Mentee Robotics further reduces near-term cash flexibility. That said, Berenberg’s Buy initiation from a position of deep technology dominance and a multi-billion-dollar pipeline warrants attention for investors with a long time horizon and tolerance for volatility.