Shopify (NASDAQ:SHOP | SHOP Price Prediction) has pulled back sharply from recent highs. The stock is down 21.14% year-to-date as of mid-April 2026, yet the underlying business has never looked stronger. Here are three reasons the stock may be worth watching.

Reason 1: The Revenue Growth Is Relentless

Shopify has now posted 11 consecutive quarters of 25%+ revenue growth, and that streak is not slowing. Full-year 2025 revenue reached $11.55 billion, up 30.14% year over year. Q4 2025 alone delivered $3.67 billion in revenue, up 30.6% year over year, beating the consensus estimate by 2.34%.

Revenue has grown to 3.9 times its 2020 level. Growth is broad-based: Merchant Solutions grew 35% in Q4 2025, B2B gross merchandise volume surged 96% in 2025, Shop Pay Gross Merchandise Value jumped 62% in Q4 2025, and international revenue expanded 36% in 2025.

When growth is this consistent across segments, it reads as structural rather than cyclical. Management guided for low-thirties percentage revenue growth in Q1 2026, extending the streak further.

Reason 2: The Free Cash Flow Machine Is Real

Many high-growth tech companies promise profitability “someday.” Shopify is already there. The company generated $2 billion in free cash flow in 2025, up 25.67% year over year. That marks 10 consecutive quarters of double-digit free cash flow margins.

Q4 2025 alone produced $715 million in free cash flow at a 19% margin. Operating income reached $1.46 billion for the full year, up 36.56% year over year.

The balance sheet reflects this strength: total liabilities fell 27.47% year over year to $1.716 billion, while shareholders’ equity grew 16.57% to $13.473 billion. Management backed this confidence with a $2 billion share repurchase program effective February 17, 2026. Companies that generate real cash and return it to shareholders tend to attract sustained institutional interest.

Reason 3: The Valuation Has Reset to a More Interesting Level

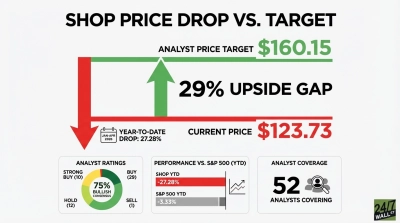

The trailing P/E sits at 135x, which demands respect. But the forward P/E compresses to 68x as earnings scale, and the analyst community remains firmly behind the thesis: 39 buy ratings and 10 strong buy ratings versus just 1 sell rating, with a consensus price target of $159.70.

The stock traded as high as $182.19 over the past 52 weeks and now sits at $126.94.

The company holds over 14% of U.S. ecommerce market share and a platform moat that compounds with every merchant added. Monthly recurring revenue reached $205 million in Q4 2025, up from $178 million a year earlier. That recurring revenue base signals high merchant retention and platform lock-in.

What Could Go Wrong

Tariff disruptions, softening consumer sentiment (the University of Michigan index sat at 56.6 in February 2026, a historically low reading), and rising loan losses as Shopify Capital scales are real risks. But Shopify’s revenue growth has held above 25% through multiple macro cycles, its free cash flow provides flexibility to absorb pressure, and its diversification into B2B, international markets, and offline commerce means no single headwind can derail the platform.

Shopify is building the infrastructure layer of global commerce, and the stock has pulled back 21.14% year-to-date while the business grew revenue at 30.14% in its most recent full year. That gap between price and business performance is a dynamic that long-term investors may find worth monitoring.