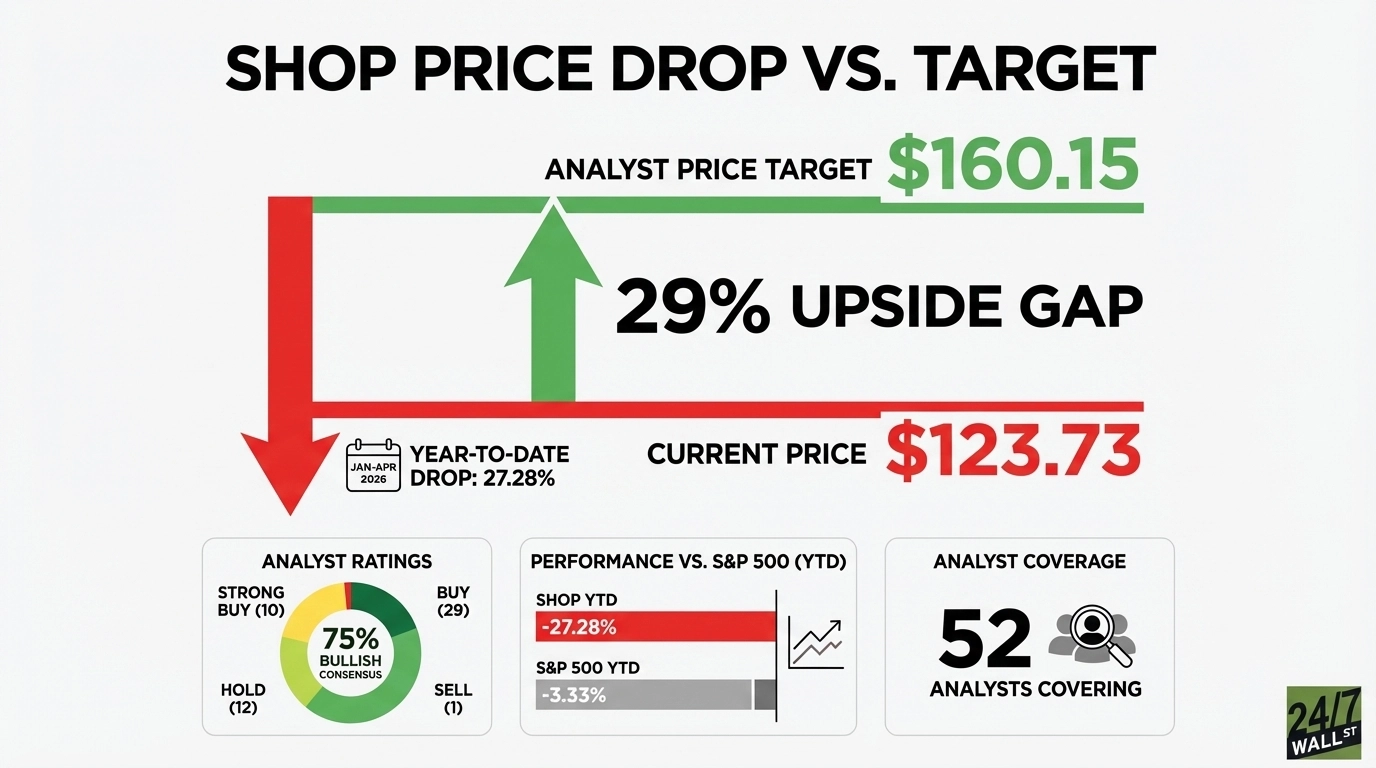

Shopify (NASDAQ:SHOP | SHOP Price Prediction) currently trades around $123.73, while the average Wall Street analyst price target sits at $160.15, which points to roughly 29% upside for the stock today.

Shopify dominates e-commerce infrastructure in the United States, commanding over 14% of the US e-commerce market share and serving millions of merchants across 175+ countries, from solo entrepreneurs to global brands like SKIMS and Supreme. The company generates revenue through subscription plans and merchant services, including payments, capital, and shipping. The current dislocation between price and target warrants examination, given Shopify’s rapid, consistent growth.

A Year-End Peak Followed by Sharp Reversal

Shopify’s stock peaked near $163.14 in mid-December 2025 and has pulled back sharply since then. Year to date, SHOP is down 27.28%, which is a much steeper decline than the S&P 500’s 3.33% drop over the same period. That gap suggests the selloff has been driven by more than just a weak market backdrop.

The latest earnings report was not really the main problem. Revenue for the quarter came in at $3.672 billion, ahead of the $3.588 billion consensus estimate by 2.34%. Instead, investors appear to be repricing the stock against a tougher macro backdrop, with tariff exposure, shifting consumer spending, and uncertainty around AI adoption all weighing on sentiment. With a beta of 2.822, Shopify tends to amplify broader market moves, and Q1 2026 has mostly worked against the stock.

The drop in net income added another layer of concern. Q4 net income fell 42.54% year over year, and full-year net income declined 39.03%, but those figures were distorted by equity investment comparisons rather than weakness in the underlying business. In a risk-off environment, though, that kind of nuance often gets ignored.

Why 39 Analysts Still Have Buy Ratings

The bull thesis rests on impressive operating fundamentals. Shopify has posted 6 consecutive quarters of 25% or greater revenue growth, which is a streak few large-cap technology companies currently match. Operating income grew 35.7% year-over-year in Q4, free cash flow hit $715 million at a 19% margin, and a $2 billion share repurchase program signals management sees the current share price as an opportunity.

Of the 52 analysts covering SHOP, 10 rate it a Strong Buy, 29 rate it a Buy, 12 rate it a Hold, 1 rates it a Sell. That means 75% of analysts are bullish with virtually no one on Wall Street bearish. Analysts focus on specific catalysts like B2B GMV momentum (which surged 96% in 2025), Shop Pay’s expanding role as a standalone payment network (GMV up 62%), and international revenue growth of 36% as Shopify Payments reaches 60 countries. These represent significant addressable market expansion not yet fully priced in.

The Valuation Gap

SHOP trades at $123.73, against a consensus analyst target of $160.15, implying roughly 29% upside. The stock is down 27.28% year-to-date versus the S&P 500’s 3.33% decline, reflecting a risk premium on high-multiple growth names. SHOP’s trailing P/E stands at 127x and its forward P/E at 63x, leaving little room for execution misses.

The stock’s 52-week high is $182.19 illustrates the sentiment-driven volatility of recent months. On a one-year basis, SHOP is still up 48.52%, underscoring recent weakness rather than long-running deterioration. Guidance for low-thirties percentage revenue growth in Q1 2026 suggests the underlying business is still growing rapidly.