Every cannabis trader’s feed is buzzing about SNDL (NASDAQ:SNDL) because the company’s Q1 2026 release on April 28, 2026 delivered a tidy little EPS beat that retail can rally around. The underlying numbers tell a different story.

SNDL shrank. Revenue arrived at $143.29 million (U.S. dollars), a 4.4% year-over-year decline that missed consensus by 31.87%. Every segment shrank, including Liquor Retail at $76.13 million, Cannabis Retail at $56.57 million, and Cannabis Operations at $21.53 million. That headline EPS surprise was manufactured by a SunStream JV swing from loss to profit, a $1.09 million tax recovery, and lower impairments. The stores themselves sold less of everything to fewer people.

SNDL is perpetually shrinking

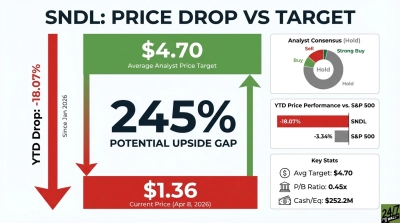

The strategic backdrop is weaker than the headline EPS suggests. SNDL is a sprawling Canadian liquor-and-cannabis conglomerate whose largest segment is shrinking liquor retail (Q4 2025 same-store sales fell 4.0%), whose Cannabis Retail same-store sales turned negative at 0.7%, and which decided this was the right moment to repurchase stock at a $2.13 weighted average price. The current price is $1.32. SNDL’s Altman Z-Score at 0.84, squarely in the distress zone, and the five-year chart, down 83.63%, has been telling you this for a long time.

What you should buy instead

The redirect is High Tide (NASDAQ:HITI), the largest cannabis retail chain in Canada and a smaller, more focused operator. Three reasons it deserves a seat at the table while everyone day-trades SNDL’s narrative.

One: it actually grows. High Tide’s Q1 2026 revenue climbed 25.2% year over year to $130.29 million, operating income flipped positive to $1.73 million against SNDL’s $6.67 million operating loss, and adjusted EBITDA rose 62% to $8.37 million. Q4 2025 same-store sales advanced 5.5%. While SNDL’s traffic sags, High Tide’s 218 Canna Cabana locations command roughly 12% of the Canadian cannabis market.

Two: there is a real international story. The Remexian Pharma GmbH acquisition contributed $18.25 million in the first quarter alone and plugs High Tide directly into Germany’s medical cannabis market, with a UK entry planned within 12 months. By comparison, SNDL’s full-year 2025 international cannabis sales totaled $12.6 million. One company is going abroad. The other is a Canadian liquor store with a cannabis sideline.

Three: the loyalty moat does real work. Cabana Club membership hit 2.58 million Canadians, up 47% year-over-year, and the paid Elite tier doubled to 162,000 members. Those members buy white-label SKUs that High Tide is pushing toward 20% of sales from 1.6% today, a mix shift that expanded brick-and-mortar gross margin to 28% from 25%. At High Tide, the loyalty program functions as a genuine margin engine.

Wall Street has noticed

Analysts carry an average price target of $5.67 on High Tide against a recent price of $2.42, with one Strong Buy and five Buys and zero Holds or Sells. The composite prediction sentiment reads bullish at 64.66; SNDL’s reads bearish at 34.48. The risks on the High Tide side are real, including an Altman Z-Score of 1.33, declared material weakness in internal controls, and equity that has eroded from $73.48 million to $64.17 million between October 2024 and January 2026. Cannabis stocks are speculative by nature. The choice on offer is a focused growth retailer with margin expansion and an international runway, versus a diversified Canadian holding company whose best quarter came from accounting adjustments.

HITI stock also comes with a more established floor price ~$2.2 and further support levels through to $1.5. For SNDL, the stock could keep diluting more and more. High Tide is simply the safer and better long-term pick. I would buy it instead of trying to time the bottom on SNDL stock.