Wall Street is divided on Microsoft (NASDAQ:MSFT | MSFT Price Prediction) after the company’s fiscal Q3 2026 report. Barclays trimmed its price target to $545 from $600 while keeping an Overweight rating, and Wells Fargo raised its price target to $625 from $615, also keeping Overweight. Both firms see the same Azure acceleration and artificial intelligence (AI) tailwinds, yet disagree on what investors should pay for them.

| Ticker | Company | Firm | Action | Old Rating | New Rating | Old Target | New Target |

|---|---|---|---|---|---|---|---|

| MSFT | Microsoft | Barclays | Price target cut | Overweight | Overweight | $600 | $545 |

| MSFT | Microsoft | Wells Fargo | Price target raised | Overweight | Overweight | $615 | $625 |

Microsoft stock is reacting to the split, with shares down 5% on Thursday to $404 after the report. The tension between durable enterprise demand and rising capital expenditure (CapEx) frames the entire Microsoft stock debate today.

The Analyst’s Case

Wells Fargo argues the investments are more clearly paying off, with Microsoft 365 (M365) and Azure each guided to acceleration. The firm highlights Microsoft’s AI business reaching $37 billion in annualized run rate and a Copilot narrative improving given the pace of seat additions and confidence around usage.

Barclays, while still bullish, asserted that Microsoft’s spending commentary “show healthy expansion driven by ongoing AI capacity shortage” and that shares are “starting to react better again.” The lower target reflects a more disciplined view on the multiple, even as the firm believes Microsoft remains well positioned to benefit from AI momentum.

Company Snapshot

Microsoft posted Q3 FY2026 revenue of $82.89 billion, growing 18% year over year (YoY), with earnings per share (EPS) of $4.27 topping consensus. Intelligent Cloud revenue rose 30% to $34.68 billion, with Azure and other cloud services up 40%.

Microsoft CEO Satya Nadella declared, “Our AI business surpassed an annual revenue run rate of $37 billion, up 123% year-over-year.” Commercial remaining performance obligations stand at $627 billion, up 99%, signaling deep long-term demand visibility.

Microsoft’s CapEx, however, jumped to $30.88 billion, up 84% YoY. That figure is a focal point of the bear case on Microsoft stock.

Why the Move Matters Now

Microsoft trades at a P/E ratio of 27x with a market cap near $3.01 trillion. Despite today’s sell-off, shares are up 13% over the past month, reflecting the rally into earnings.

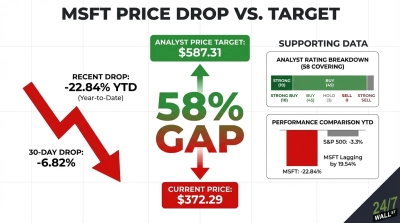

The Wall Street consensus on Microsoft stock remains constructive, with 55 buy ratings, 3 holds, and zero sells. The Barclays cut signals that even bulls are recalibrating valuation in a market wary of broader software multiple compression, a theme explored in this AI CapEx cycle and cloud winners.

What It Means for Your Portfolio

The Microsoft bull case hinges on AI capacity shortages, durable enterprise franchises in M365 and Azure, and accelerating Copilot adoption. The bear case centers on CapEx intensity pressuring free cash flow and margins if AI returns lag the buildout.

For prudent investors, Microsoft stock can remain a core holding with visible demand and improving AI monetization. Position sizing matters more than timing here, and staggered entries can buffer near-term volatility tied to the CapEx debate.

Watch for whether Azure growth sustains its acceleration next quarter and whether Microsoft’s CapEx growth begins to moderate. Those two data points will likely settle the analyst split between Barclays and Wells Fargo.