Meta Platforms (NASDAQ:META | META Price Prediction) just delivered one of the strongest quarters in its history, yet the stock sold off hard. That dislocation is exactly where our model finds opportunity.

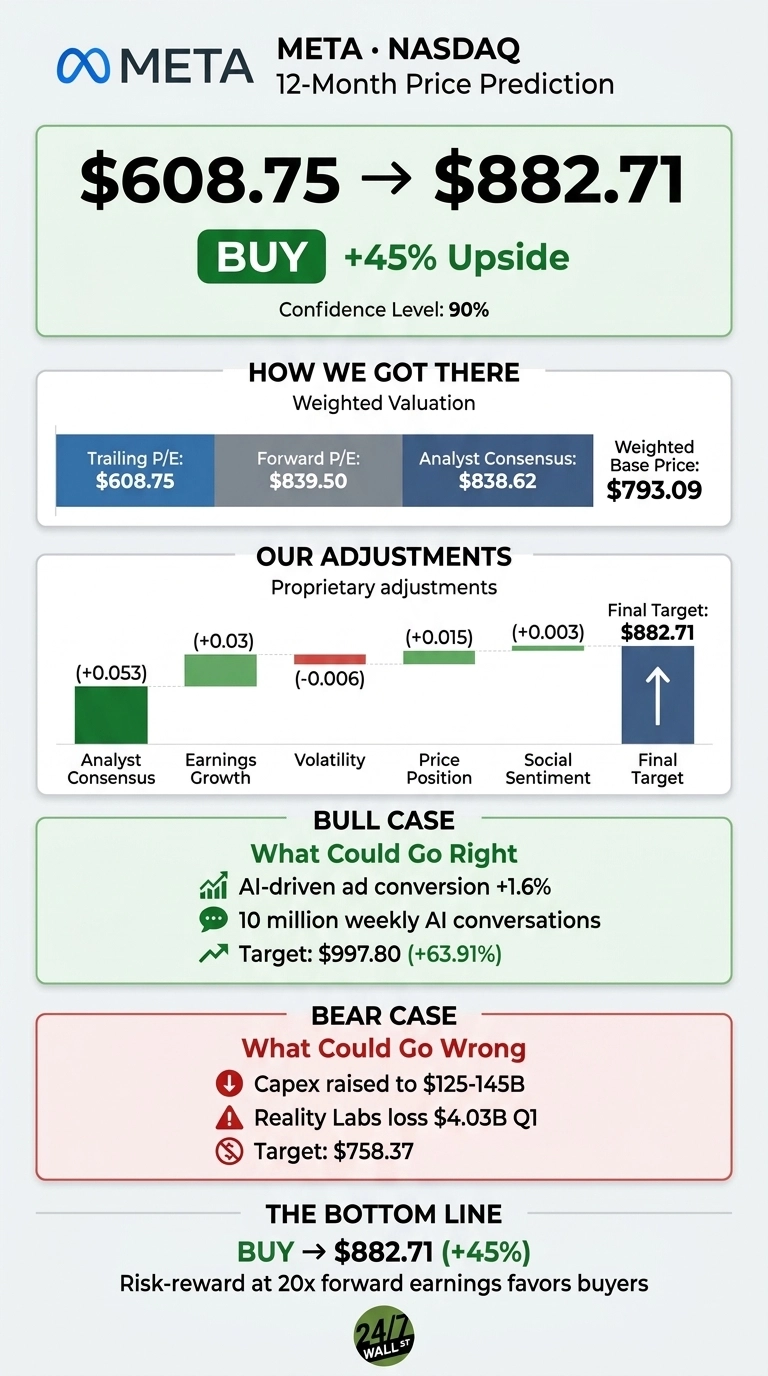

Our 24/7 Wall St. price target for Meta is $882.71 over the next 12 months, implying roughly 45% upside from the recent $608.75 close. Our model assigns Meta a buy rating with high confidence.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $608.75 |

| 24/7 Wall St. Price Target | $882.71 |

| Upside | 45% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Strong Earnings Report Met With a Sharp Selloff

Meta posted Q1 2026 revenue of $56.31 billion, growing 33.08% year over year, with EPS of $10.44 beating consensus by 56.79%. Ad impressions rose 19% and price per ad climbed 12%, a powerful combination. Yet shares fell from $671.77 at the filing to $608.745 within a day, after Meta raised 2026 capex guidance to $125 to $145 billion.

Year to date, META is down 7.7% and trades roughly 6% below its 52-week high of $794.38.

The Case for $1,000+

The bull case rests on AI compounding into both ad pricing and engagement. CFO Susan Li noted the adaptive ranking model drove a 1.6% increase in conversion rates, and the value optimization suite now runs at over $20 billion in annual revenue. Engagement gains are equally striking: Instagram Reels time spent rose 10% and Facebook video time jumped more than 8% in a single quarter.

Layer in 10 million weekly business AI conversations, AI glasses daily users tripling, and Mark Zuckerberg’s claim Meta is “on track to deliver personal superintelligence to billions of people”, and our bull case scenario lands at $997.80, a 63.91% total return.

Wedbush, Bank of America, and Morgan Stanley sit among the 57 buy ratings backing this thesis.

The Risks Worth Watching

The bear case centers on capex digestion. Meta raised 2026 capex to $125 to $145 billion, a massive step up, while Reality Labs lost $4.03 billion in the quarter alone. Free cash flow grew just 11.74% despite blistering revenue growth. Add in youth-related litigation trials in 2026 and EU regulatory pressure, and our bear case lands at $758.37.

Bulls would counter that $107 billion in new contractual commitments reflects internal demand signals management trusts. Susan Li also confirmed Meta has “continued to underestimate our compute needs”, which signals genuine compute demand if AI monetization keeps compounding. Insider activity also leans constructive, with 196 recent transactions netting to buying.

The Bottom Line

The 24/7 Wall St. price target of $882.71 with 90% confidence reflects a simple read: Meta grew revenue 33% while the market punished it for spending to defend that growth.

The bull thesis hinges on AI capex translating into higher ad ROI within 18 months. The bear thesis assumes 2027 capex resets even higher and operating margins compress below 35%. The risk-reward at 20x forward earnings favors the buyers.

Looking further ahead, here is where our 24/7 Wall St. price target model projects Meta could trade in the coming years, assuming current growth trajectories hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $882.71 |

| 2027 | $1,112.87 |

| 2028 | $1,361.68 |

| 2029 | $1,525.48 |

| 2030 | $1,702.49 |

These projections assume Meta keeps converting AI investment into ad and engagement gains. Meaningful upside or downside could result from regulatory action, a recession that crimps ad budgets, or a faster-than-expected Reality Labs path to profitability.