Pfizer (NYSE:PFE | PFE Price Prediction) and Moderna (NASDAQ:MRNA) just closed the books on Q4 2025, and the contrast is striking. Pfizer leaned on a diversified non-COVID portfolio and a fresh push into obesity drugs.

Moderna leaned on cost cuts and international expansion to soften a steep COVID revenue cliff. Two very different pharma stories, both shaped by life after the pandemic windfall.

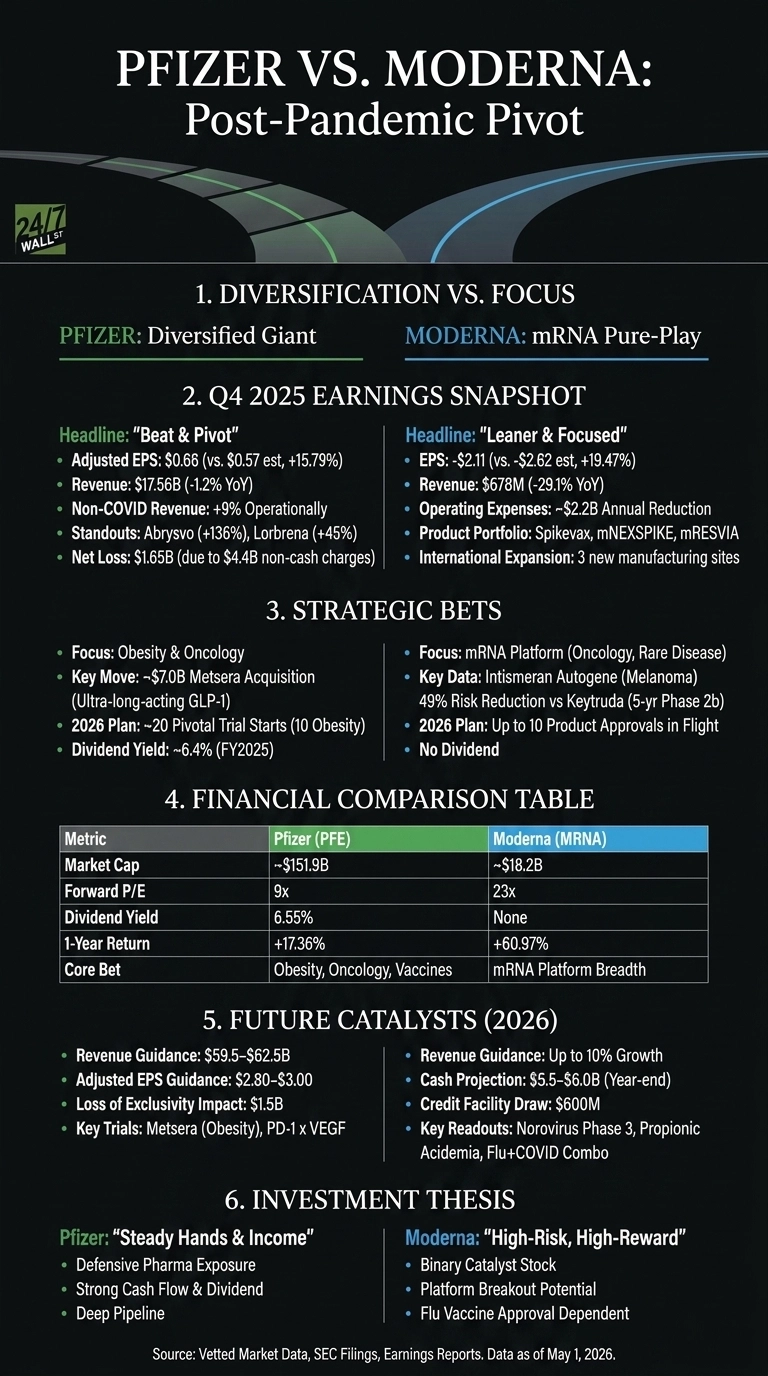

Diversified Drugmaker Beats. mRNA Pure-Play Survives.

Pfizer posted adjusted EPS of $0.66 against a $0.57 consensus on $17.56 billion in revenue, with the top line dipping just 1.2% year over year. The non-COVID book did the heavy lifting, growing 9% operationally.

Standouts included Abrysvo at +136% and Lorbrena at +45%. The bruise: a $4.4 billion non-cash impairment tied to pipeline revisions dragged the GAAP line into a $1.65 billion net loss. Ugly optics, but largely accounting noise.

Moderna told a leaner story. Revenue landed at $678 million, down 29.08% year over year, while the loss per share of $2.11 still beat the $2.62 estimate.

CEO Stéphane Bancel pointed to “approximately $2.2 billion” in annual operating expense reductions, calling out three new international manufacturing sites in the UK, Australia, and Canada. The product story is thin: Spikevax, mNEXSPIKE, and mRESVIA. The pipeline story is wide.

Obesity Bets vs Oncology mRNA

Pfizer’s strategic pivot is unmistakable. Albert Bourla closed the $7 billion Metsera deal for ultra-long-acting GLP-1 obesity assets and is planning 10 pivotal trial starts in 2026 from that platform alone. He framed 2026 as “an important year rich in key catalysts” with roughly 20 pivotal study starts.

| Lens | Pfizer | Moderna |

| Market Cap | ~$151.9B | ~$18.2B |

| Forward P/E | 9x | 23x |

| Dividend Yield | 6.55% | None |

| 1-Year Return | +17.36% | +60.97% |

| Core Bet | Obesity, oncology, vaccines | mRNA platform breadth |

Moderna is doubling down on what it knows: mRNA. The intismeran autogene melanoma program with Merck showed a 49% reduction in risk of recurrence or death versus Keytruda alone in the five-year Phase 2b readout. The science is persuasive, though the FDA refusal-to-file letter on the mRNA-1010 flu vaccine remains a clear overhang.

The Next Test Is Catalyst Execution

Pfizer guides 2026 revenue to $59.5 to $62.5 billion and adjusted EPS of $2.80 to $3, baking in $1.5 billion in loss-of-exclusivity headwinds plus Most-Favored-Nation pricing pressure. Bourla’s recent phantom stock unit acquisitions through April 2026 read as quiet confidence.

Moderna projects up to 10% revenue growth with cash falling to $5.5 to $6 billion, after drawing $600 million on a $1.5 billion credit facility. Norovirus Phase 3 data and propionic acidemia readouts are the catalysts I would circle.

Why I Lean Toward Pfizer for Steady Hands, Moderna for Risk Tolerance

For me, Pfizer fits the income-and-stability investor. A 6.55% yield, a forward P/E of 9x, and a real obesity and oncology pipeline give it room to compound.

Moderna is a different animal: a binary catalyst stock, up 55.78% year to date on hopes that melanoma data and international growth offset US weakness. For defensive pharma exposure with cash flow, Pfizer screens better on the numbers. Moderna’s profile fits a higher-risk, catalyst-driven setup, with bigger upside tied to a platform breakout. Moderna’s setup arguably hinges on the FDA flu situation clearing.