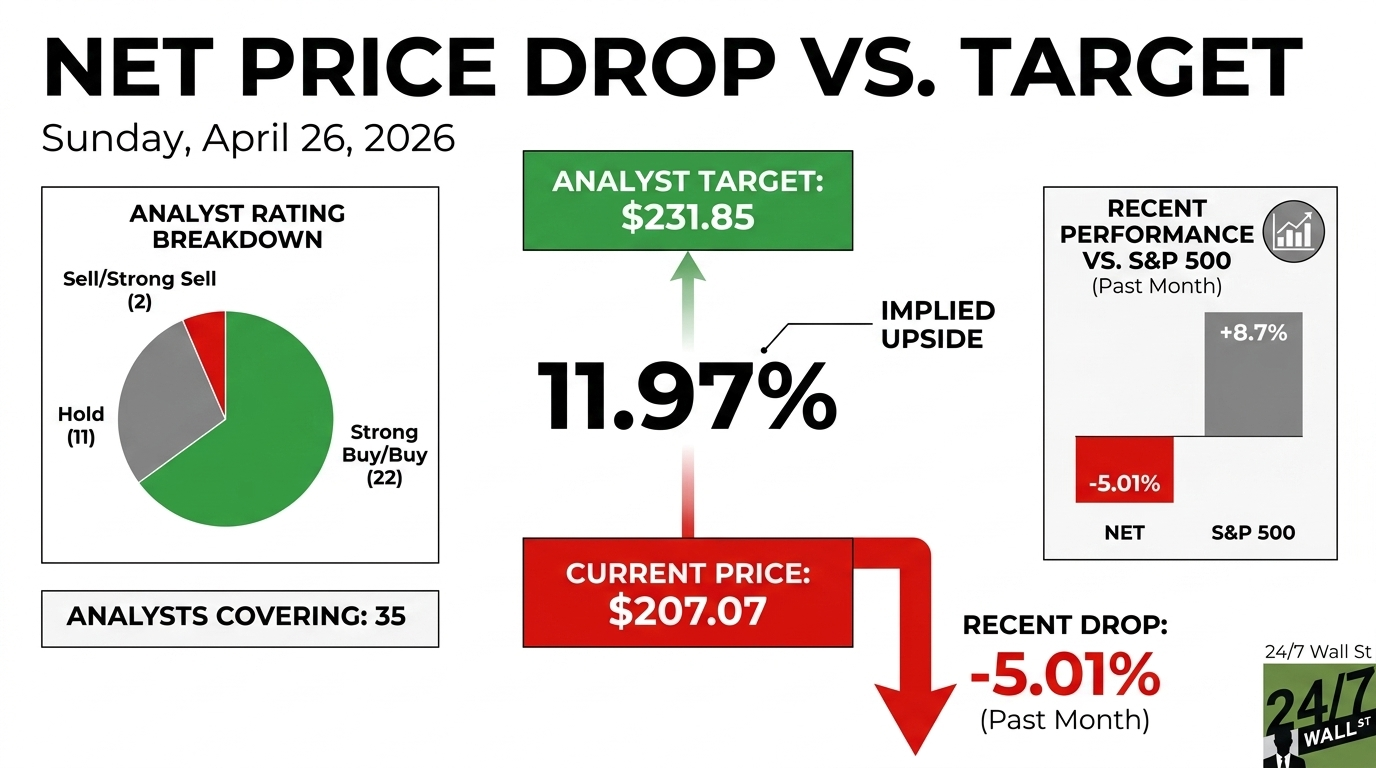

Cloudflare (NYSE:NET | NET Price Prediction) currently trades around $207.07, while the average Wall Street price target sits at $231.85, implying roughly 12% upside. Cloudflare operates a global connectivity cloud that delivers content, secures traffic, and increasingly serves as infrastructure for AI workloads. CEO Matthew Prince has positioned the company as the platform powering the “agentic Internet,” where AI agents run and interact across networks. Cloudflare is one of the most-watched infrastructure names in software. Still, the stock isn’t cheap by any means, trading at 182x forward earnings.

Cloudflare’s Stock Price is Roughly Flat Over 2026

Cloudflare’s latest earnings initially pushed shares higher, but the move quickly reversed. The company reported revenue of $614.5 million, up 33.6% year over year, with non-GAAP EPS of $0.28, beating expectations. On the surface, the quarter looked strong. The issue was underneath. GAAP gross margin declined to 73.6% from 76.4%, the operating loss widened to $49.2 million, and stock-based compensation rose to $132.4 million. On a stock trading at a forward multiple near 179x earnings, margin pressure matters.

Then came insider selling. From February to April, CEO Matthew Prince offloaded roughly $63.8 million in stock under a 10b5-1 plan, President Michelle Zatlyn sold about $45.6 million, and CFO Thomas Seifert added another $12.1 million. This totaled over $121.5 million sold in executive sales.

Analysts are Largely Bullish

Despite the volatility, analysts have largely maintained a bullish outlook on Cloudflare. The company closed its largest-ever deal in Q4, averaging $42.5 million annually, while total new ACV grew nearly 50% year over year. Remaining performance obligations increased 48%, and free cash flow margin improved to 16%. Firms like Robert W. Baird and Piper Sandler remain positive, pointing to growth in AI infrastructure, security, and serverless compute. Cantor Fitzgerald remains more cautious, citing valuation.

Of the 35 analysts covering the name, 22 rate it a Buy or Strong Buy, 11 rate it a Hold, and 2 rate it a Sell or Strong Sell. The catalyst they are watching is the FY2026 guidance of $2.785 to $2.795 billion in revenue and non-GAAP EPS of $1.11 to $1.12, expected to be reported on May 7. Prediction markets assign an 82% probability that the company will beat guidance, which would reset sentiment.

Tempting Story, But Trading at a Demanding Multiple

The bull case rests on Cloudflare successfully monetizing the “agentic Internet.” If workers’ adoption scales, AI workloads drive incremental usage, and contract growth holds near recent levels, the company can grow into its valuation and push toward analyst targets. The bear case rests on execution risk. Continued margin pressure, high stock-based compensation, and a premium valuation leave little room for error. Insider selling adds to the perception that the stock may already reflect much of the upside.

At current levels, the setup is tight. The story remains compelling, but a 12% upside doesn’t leave much room for error on a stock trading at 182x forward earnings. The next earnings report will be key in determining whether the company’s growth can support the valuation.