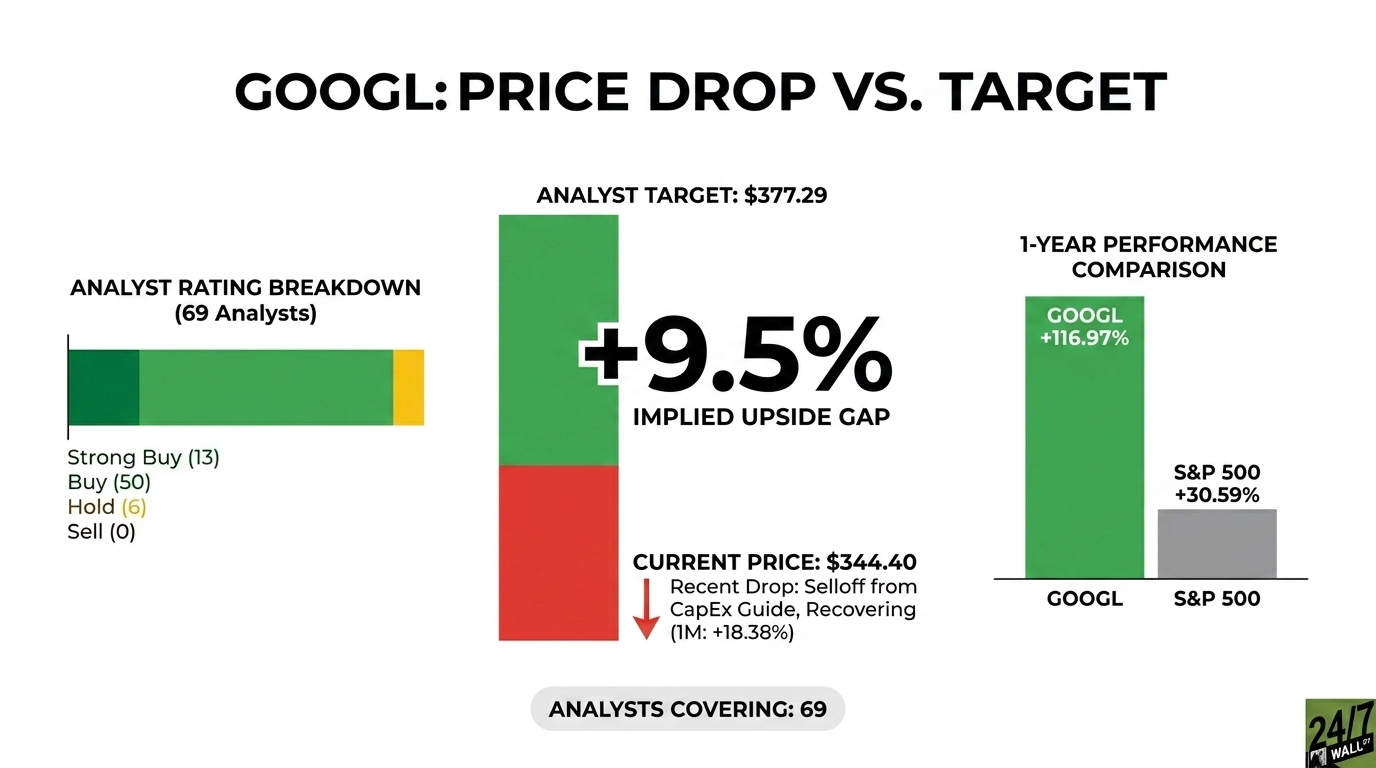

Alphabet (NASDAQ: GOOGL) trades at $344.40, while Wall Street’s consensus price target sits at $377.29, implying the stock has roughly 9.5% upside. Alphabet owns Google Search, YouTube, Google Cloud, Waymo, and the Gemini AI platform. The stock remains a focal point as AI and cloud growth accelerate at scale, while management commits unprecedented capital to infrastructure to maintain that lead. Shares are up 116.97% over the past year and recently touched a 52-week high of $348.75. Even after that run, analysts still see upside.

Q1 Results Show the Business Accelerating

Alphabet’s first quarter results reinforced why analysts are largely bullish. Revenue grew 22% to $109.9 billion, marking the 11th straight quarter of double-digit growth. Operating income rose 30%, with margins expanding to 36.1%, showing strong leverage despite rising investment. Google Cloud was the standout, with revenue jumping 63% to $20.0 billion, while operating income jumped to $6.6 billion, nearly tripling year over year.

Search also remained strong, with revenue up 19%, while YouTube ads and subscription businesses continued to grow steadily. AI usage is scaling quickly. Gemini is now processing over 16 billion tokens per minute, and paid subscriptions across the ecosystem reached 350 million. The takeaway is that growth is accelerating across core segments, while profitability continues to expand.

Why Analysts Remain Bullish

Of the 69 analysts covering Alphabet stock, 63 rate the stock Buy or Strong Buy, with 6 Holds and no Sells. The thesis that analysts are excited about is that the company’s current heavy CapEx spending is driving a multi-year growth cycle. Cloud is scaling rapidly, AI usage is increasing, and Alphabet’s full-stack approach positions it across infrastructure, models, and applications.

Free cash flow remains strong at over $64 billion on a trailing basis, even as capital spending ramps. Google trades at a forward P/E multiple of about 30x, which is right around the average multiple the stock has traded at in the past year.

My Take: A Quality Compounder Trading Near Fair Value

The bull thesis rests on the $175 to $185 billion CapEx cycle driving durable cloud share gains, Gemini monetization scaling beyond the current 350 million paid subscriptions, and Waymo’s $16 billion funding round eventually delivering a real autonomy business. The bear case centers on CapEx ROI compressing operating margins, antitrust remedies meaningfully altering search economics, or higher losses in Anthropic and Other Bets losses, which was already $2.1 billion in Q1.