Argus has flipped bullish on Palantir Technologies (NASDAQ:PLTR | PLTR Price Prediction), upgrading the stock to Buy from Hold with a $190 price target after a sharp post-earnings sell-off. The call lands the same day Citi reiterated a Buy rating and lifted its target to $225 from $210, signaling that Wall Street views the recent weakness as a sentiment problem rather than a fundamentals problem.

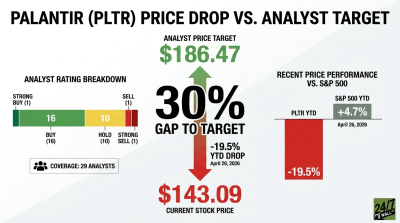

With Palantir stock trading near $133 and down 25% year to date, the question for prudent investors is whether $130 represents a credible floor or simply the next stop on a multiple compression path. The answer hinges on whether operating leverage can outrun multiple compression.

| Ticker | Company | Firm | Action | Old Rating | New Rating | Old Target | New Target |

|---|---|---|---|---|---|---|---|

| PLTR | Palantir Technologies | Argus | Upgrade | Hold | Buy | n/a | $190 |

| PLTR | Palantir Technologies | Citi | Price Target Raise | Buy | Buy | $210 | $225 |

The Analyst’s Case

Argus argues that Palantir Technologies’ revenue growth has accelerated and operating margin has vaulted, creating an attractive entry point after the pullback. The firm also raised its FY2026 EPS view by 15 cents to $1.47 and FY2027 view by 25 cents to $1.94, an operating leverage thesis built on the Q1 2026 results.

Citi’s logic runs parallel. The firm views the Q1 report as strong, sees AI demand accelerating Palantir’s U.S. business, and raised estimates post-earnings.

Company Snapshot

Palantir Technologies builds Gotham, Foundry, and AIP, the Artificial Intelligence Platform behind much of its recent commercial momentum. Q1 2026 revenue came in at $1.633 billion, up 85% year over year, with U.S. commercial revenue jumping 133%.

Management raised full-year 2026 revenue guidance to $7.65 to $7.662 billion, a 71% growth rate, alongside a Rule of 40 score of 145. Palantir Technologies CEO Alex Karp called the demand backdrop one where “we just cannot meet demand.”

Why the Move Matters Now

The disconnect is the story. PLTR stock fell hard despite a blowout report, and Argus is effectively saying the sell-off overshot. The valuation, however, remains demanding: shares trade at a trailing P/E ratio of 154x and a forward P/E ratio of 114x.

The split between Citi’s $225 and Argus’s $190 captures that tension. Both are bullish, yet they disagree on how much upside remains for PLTR stock once multiple compression risk is factored in. The prediction markets are even more cautious, assigning just a 0.06 probability to PLTR hitting $180 in May.

What It Means for Your Portfolio

For long-term Palantir Technologies investors, the bull case rests on durable operating leverage: 60% adjusted operating margins, 150% net dollar retention, and AIP traction across both commercial and government books. The bear case is straightforward, namely that even strong fundamentals can be overwhelmed by sentiment when the multiple is this stretched.

Argus’s $190 target signals confidence that the post-earnings drawdown has reset risk/reward. However, with PLTR stock well below its 200-day moving average of $164.26 and insider activity tilting toward selling, the floor thesis remains a research thesis, not a guarantee.

Prudent investors weighing the analyst upgrade should treat $190 as one credible scenario among several for Palantir Technologies stock. It’s wise to size your positions accordingly, and watch upcoming guidance prints for confirmation that the operating leverage story still has room to run.