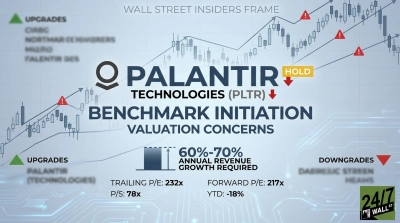

On April 30, Oppenheimer initiated coverage of Palantir (NASDAQ:PLTR) stock with an Outperform rating and a $200 price target. The bullish call rests on Palantir’s Ontology-anchored architecture, which the firm believes creates considerable switching costs once embedded, alongside defense technology tailwinds and rapid commercial expansion. For long-term investors, the initiation lands as a fresh institutional vote at a moment when software multiple compression has weighed on the artificial intelligence (AI) cohort.

Palantir stock trades around $139, down 22% year to date (YTD), even after a five-year gain of roughly 504%. Oppenheimer sees the premium valuation as justified given Palantir’s lead in AI application deployment across U.S. government and commercial sectors.

| Ticker | Company | Firm | Action | Old Rating | New Rating | Old Target | New Target |

|---|---|---|---|---|---|---|---|

| PLTR | Palantir | Oppenheimer | Initiation | N/A | Outperform | N/A | $200 |

The Analyst’s Case

Oppenheimer argues that Palantir’s Ontology-anchored applications create durable lock-in, since custom workflows built on the platform are costly to replace. The firm also sees Palantir positively aligned to growing defense technology spend by the U.S. and its allies.

On the commercial side, the analysts highlight Palantir’s rapid expansion within traditional enterprise organizations and its “best-in-class” status in its segment. While the premium multiple remains a concern, Oppenheimer views it as warranted given Palantir’s leadership in AI application deployment.

Company Snapshot

Palantir Technologies builds Gotham, Foundry, and the Artificial Intelligence Platform (AIP), serving U.S. Commercial and U.S. Government segments. Palantir’s Q4 2025 revenue rose 70% year-over-year (YoY) to $1.41 billion, with U.S. commercial revenue up 137% YoY to $507 million.

Moreover, Palantir’s full-year 2025 revenue reached $4.475 billion, up 56%, with free cash flow of $2.27 billion. Palantir Technologies CEO Alex Karp asserted, “Palantir’s Rule of 40 score is now an incredible 127%… We are an n of 1, and these numbers prove it.”

Why the Move Matters Now

Palantir stock trades at a trailing P/E ratio of 219x and a forward P/E ratio of 108x, multiples drawing skepticism as software peers re-rate lower. The 50-day moving average of $144.93 sits below the 200-day at $164.38, reflecting the recent pullback.

Even so, Palantir’s FY 2026 guidance calls for revenue of $7.182 billion to $7.198 billion, roughly 61% YoY growth, with U.S. commercial revenue topping $3.144 billion. That accelerating profile anchors Oppenheimer’s defense of the premium.

What It Means for Your Portfolio

Prudent investors weighing Palantir stock face a clear tension: durable platform economics and AI application leadership against an extreme valuation. The analyst consensus target of $184.47 sits below Oppenheimer’s $200 call, with 17 Buy, 10 Hold, and 2 Sell ratings.

The bears flag recent insider selling, Palantir’s heavy stock-based compensation of $684 million in FY 2025, and government contract concentration. The bulls counter with a record $4.262 billion in total contract value closed in Q4 2025, up 138% YoY.

Position sizing matters with PLTR stock. Oppenheimer’s initiation is a credible bull marker, yet the multiple leaves little room for execution stumbles, making moderate exposure the more research-supported approach for prudent investors watching FY 2026 commercial bookings unfold.