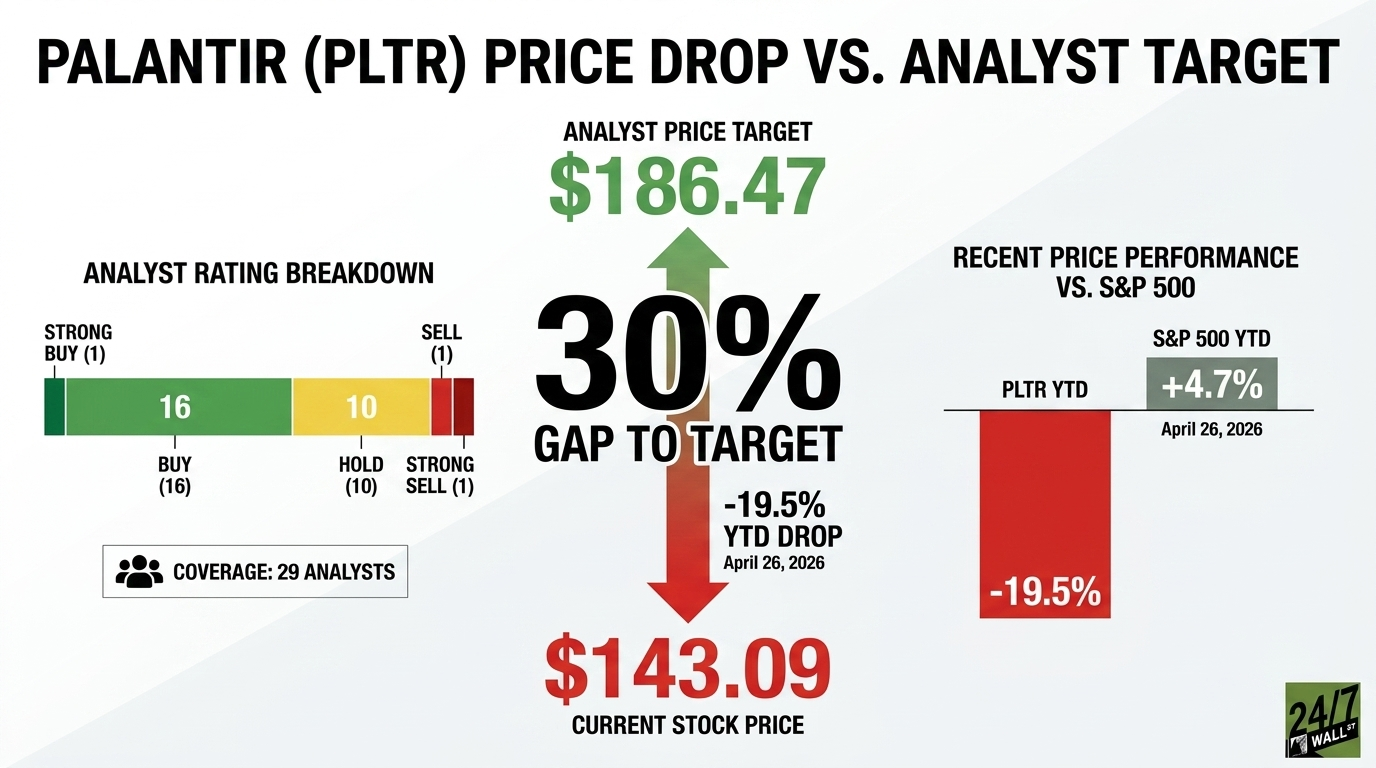

Palantir Technologies (NASDAQ:PLTR | PLTR Price Prediction) builds enterprise software platforms, including Gotham for defense and intelligence customers and Foundry and AIP for commercial AI deployments. Palantir stock currently trades at $143.09, while the average Wall Street price target sits at $186.47, which implies the stock has roughly 30% upside today if analysts are right. It has become a bellwether for whether AI software spend converts into durable, high-margin revenue, and the stock’s outsized run made it one of the most-watched names on the tape. The dislocation matters because Palantir is still printing growth that few software peers can match, yet shares have rolled over hard while the broader market keeps grinding higher. Either the market is wrong, or the bull case is breaking.

An AI Leader Facing a Reality Check

Palantir is down 19.5% year to date and 7.66% in the past month, even after delivering one of the cleanest earnings beats in software last quarter. The stock now trades roughly 31% below its 52-week high of $207.52. The primary reason for this selloff was an overall multiple compression across many AI leaders. Multiple sell-side notes flagged Palantir and other top leaders as “priced for perfection” at “euphoric and unsustainable levels”, and Palantir’s forward P/E near 111x leaves little room for error.

This is stock-specific pressure occurring against a rising broader market. The S&P 500 is up 4.7% year to date, so Palantir is bleeding alpha against the index even as Reddit sentiment in r/investing has flipped to bearish, with scores hovering in the 22 to 28 range through late April.

Why the Bull Case Hasn’t Broken

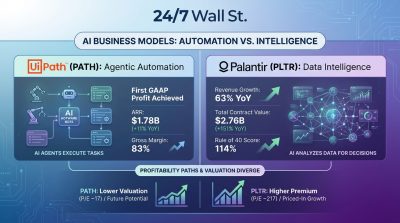

Analysts are still largely bullish on Palantir because the company’s operating model keeps improving. Q4 2025 revenue grew 70% year over year to $1.406 billion, adjusted EPS came in at $0.25, topping the $0.18 consensus estimate, and the Rule of 40 score hit 127%. U.S. commercial revenue rose 137% year over year, and total contract value closed reached $4.262 billion, up 138%.

The company’s forward outlook is particularly interesting for bulls. Management guided for 2026 revenue of $7.182 billion to $7.198 billion, implying roughly 61% growth, with U.S. commercial revenue projected above $3.144 billion. CEO Alex Karp stated: “We are an n of 1, and these numbers prove it.” Recent contract wins, including a $300 million USDA agreement and the launch of the OneMedNet Foundry-based platform, support the commercial expansion thesis.

Analysts are largely bullish on the stock, with 27 out of 29 analysts rating the stock a Hold or better:

- 1 Strong Buy

- 16 Buy

- 10 Hold

- 1 Sell

- 1 Strong Sell

What Needs to Go Right for Palantir From Here

The bull case rests on Palantir’s 2026 guidance proving conservative and U.S. commercial revenue continuing to compound above 100%. If that happens, the stock has a credible path to reach analysts’ average price target of $186. The bear case rests on whether a forward P/E of 111x can survive a normal-rate environment. If any deceleration in U.S. commercial bookings, any large government contracts slip, or any broader AI sentiment unwinds, it could result in the stock falling to a lower multiple. The fundamentals are doing their job, and the 30% gap to consensus is real, but the valuation premium means execution must remain near-flawless to justify current levels.