I keep hitting the buy button on Oracle (NYSE:ORCL | ORCL Price Prediction) because I have rarely seen a backlog like the one this company is sitting on, and I want to own as many shares as I reasonably can before the market fully prices it in.

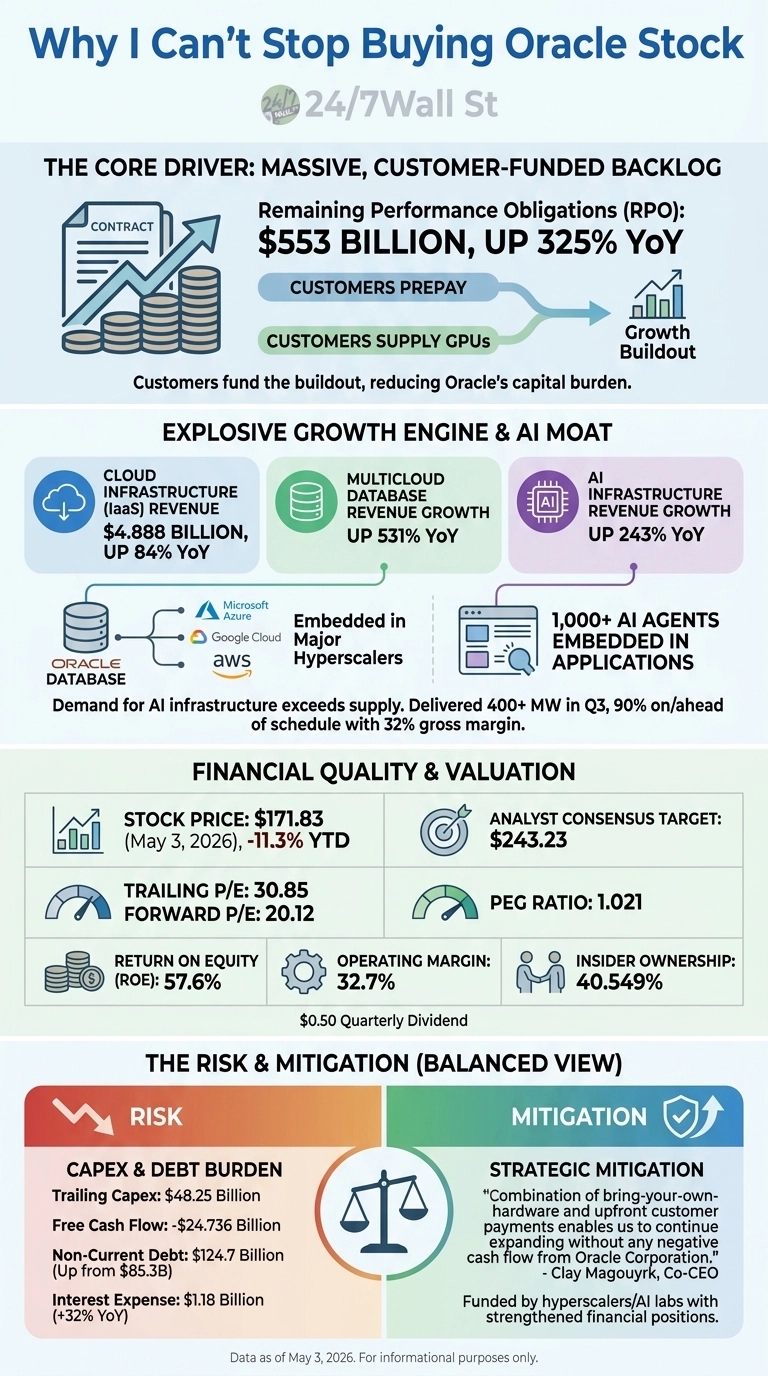

The thing that pulls me back, again and again, is a single number on the balance sheet: Remaining Performance Obligations of $553 billion, up 325% year over year. That is contracted future revenue. Customers have already signed. Many of them prepay or supply their own GPUs, which is the opposite of how most people imagine a hyperscaler funds its growth. I am buying a company whose customers are helping fund the buildout.

The data that keeps me adding

First, the growth profile. Q3 FY2026 was the first quarter in over 15 years where organic total revenue and non-GAAP EPS both grew 20% or more. Cloud Infrastructure revenue rose 84% to $4.888 billion, and Multicloud Database revenue grew 531%. EPS came in at $1.79 on $17.19 billion in revenue. Management raised FY2027 revenue guidance to $90 billion.

Second, the moat. Co-CEO Clay Magouyrk told investors that “Multi-cloud database revenue grew 531% year over year. AI infrastructure revenue grew 243% year over year. Both also have demand that exceeds supply.” Oracle Database is embedded inside Microsoft Azure, Google Cloud, and AWS, and Magouyrk added that “In Q3, we delivered more than 400 megawatts to customers. 90% of that committed capacity was delivered on or ahead of schedule.” The economics are holding too: gross margin on delivered AI capacity came in at 32%, above the 30% guidance.

Third, valuation and quality. Trailing P/E is 31, forward P/E is 20, and PEG sits at 1.021. Return on equity is 57.6%, operating margin is 32.7%, and insiders own 40.549% of the company. The $0.50 quarterly dividend is small, but it is consistent, and at $171.83, the stock is trading 11.3% below where it started the year.

The risk I refuse to wave away

Capex is the honest concern. Trailing capital spending hit $48.25 billion, free cash flow swung to negative $24.73 billion, and non-current debt climbed to $124.7 billion from $85.3 billion. Interest expense grew 32% to $1.18 billion. Oracle then raised $30 billion in investment-grade bonds and mandatory convertible preferred stock with intent to raise up to $50 billion for data center expansion.

What keeps me adding anyway is that Magouyrk explicitly framed the model: “A combination of bring-your-own-hardware and upfront customer payments enables us to continue expanding without any negative cash flow from Oracle Corporation.” The RPO is the proof. The customers funding this are the same hyperscalers and AI labs whose financial positions have strengthened over the last year.

Why the buy button stays active

Larry Ellison’s framing of “ecosystems” automation, combined with over 1,000 AI agents already embedded in Oracle applications, tells me the database franchise is becoming the connective tissue of enterprise AI.

Analyst targets sit at $243.23, though my horizon stretches well beyond 12 months. I am buying because Oracle has turned its 50-year database moat into a capital-light AI infrastructure annuity, and I plan to keep adding shares for as long as that remains true.