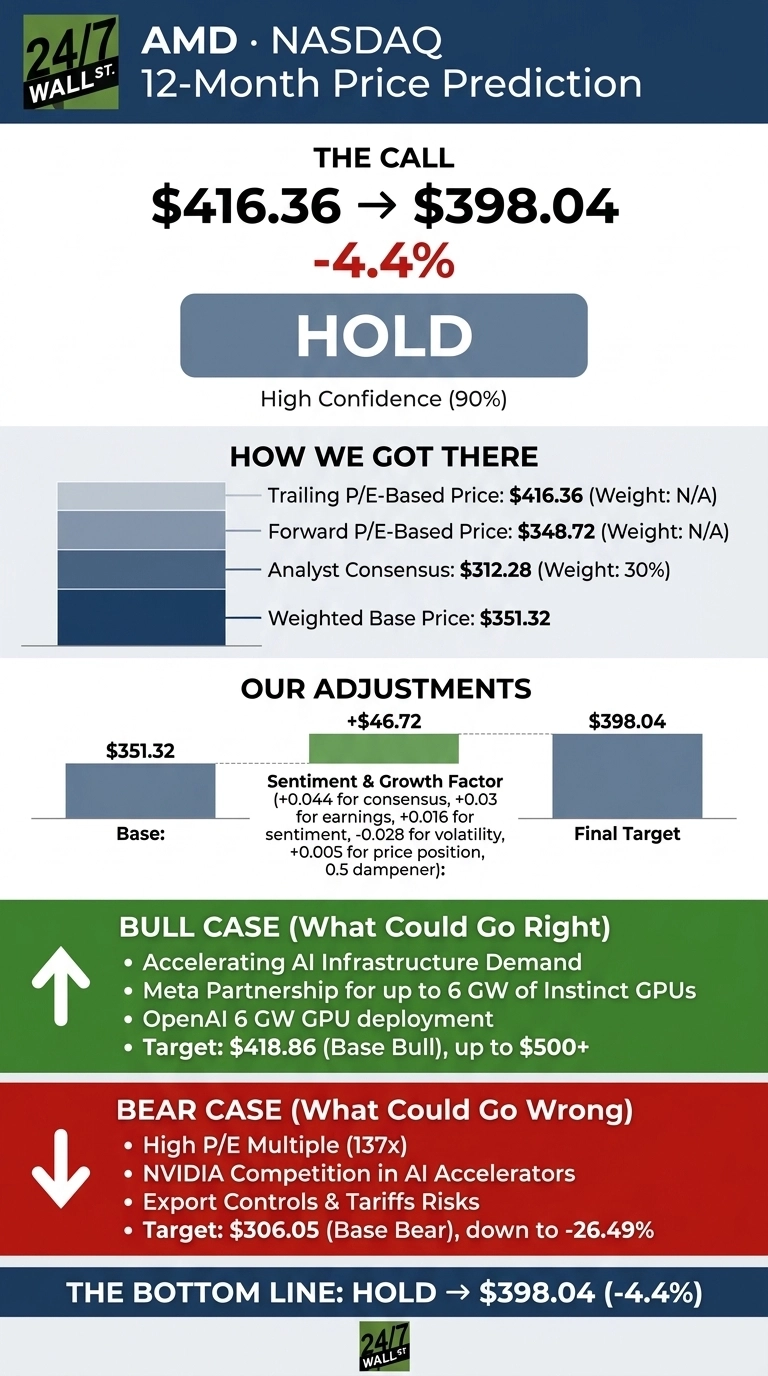

Our 24/7 Wall St. price target for Advanced Micro Devices (NASDAQ:AMD | AMD Price Prediction) is $398.04, which sits modestly below where shares currently trade after a blistering rally. With AMD changing hands at $416.36 and the model implying roughly -4.4% from here, the recommendation is hold with 90% confidence. Near fair value is the cleanest way to describe AMD today.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $416.36 |

| 24/7 Wall St. Price Target | $398.04 |

| Upside/Downside | -4.4% |

| Recommendation | HOLD |

| Confidence Level | 90% |

Why We Could Be Wrong

Before going further, our price target sits below where AMD trades today, and AMD is one of the most divisive names in semis. Real upside could come from MI450 deployments scaling faster than modeled, or from a fresh gigawatt-scale customer announcement beyond OpenAI and Meta. Treat our number as one datapoint. A detailed bull case follows.

The Q1 Earnings Report That Reset the Narrative

AMD has been on a tear, gaining 9.92% in the past week, 63.34% over the past month, and 253.18% over one year.

Q1 FY2026 results, reported May 5, 2026, drove a +17.46% day-of move. Revenue hit $10.253 billion, up 37.85% YoY, with non-GAAP EPS of $1.37. Data Center alone delivered $5.775 billion, up 57%. Q2 guidance of roughly $11.2 billion implies about 46% YoY growth.

The Case for $500+

Bulls have plenty of ammunition. Bernstein upgraded AMD to Outperform with a $525 target, up from $265, citing over $14 in 2027 EPS and approaching $20 in 2028 if the AI boom continues.

Barclays raised its target to $500 from $300 on agentic AI attach, Cantor Fitzgerald moved to $500, and BofA went to $450, flagging AMD’s low 6% market share in a $1.5T market by 2030.

The Meta partnership for up to 6 GW of AMD Instinct GPUs, the OpenAI deployment, and Oracle’s 50,000 GPU Helios supercluster could each justify a re-rate. If MI450 ramps cleanly, $500-plus is very much in play.

The Risks Worth Watching

The bear case starts with valuation. AMD trades at a 137x P/E, leaving zero margin for execution slips. NVIDIA still dominates AI accelerators, and U.S. export controls already cost AMD material charges in Q2 2025.

Jefferies, while bullish, set a more measured $415 target, essentially flat to spot. A bear-case path takes shares to $306.05, a -26.49% drawdown. Bulls would argue the elevated multiple reflects forward EPS power closer to $14 by 2027, which compresses today’s optics dramatically.

Hold for Now, but Stay Close

The model output: hold. The 24/7 Wall St. price target of $398.04 with 90% confidence reflects a strong business at a stretched price after a one-month 63.34% run. A pullback into the $340s alongside rising MI450 customer forecasts would improve the setup, while softer hyperscaler capex guidance or tighter export controls would weaken it. The risk/reward looks balanced from current levels.

AMD Price Prediction 2026-2030

Looking further out, here is where the 24/7 Wall St. price target model projects AMD could trade in the coming years, assuming current growth trajectories hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $398.04 |

| 2027 | $405.85 |

| 2028 | $414.12 |

| 2029 | $402.86 |

| 2030 | $425.65 |

These projections assume AMD keeps executing on the AI roadmap. Significant upside or downside could result from MI450 ramp velocity or a sharper-than-expected AI capex digestion cycle.