Few stocks tell a more complicated story right now than Super Micro Computer (NASDAQ:SMCI | SMCI Price Prediction). The AI server maker just delivered a margin-driven earnings beat, raised full-year guidance, and saw shares rally, all while sitting under an export-control governance cloud. Investors want to know whether this rally has legs. Our 24/7 Wall St. price target frames the setup with data.

Our 24/7 Wall St. Price Target for Super Micro

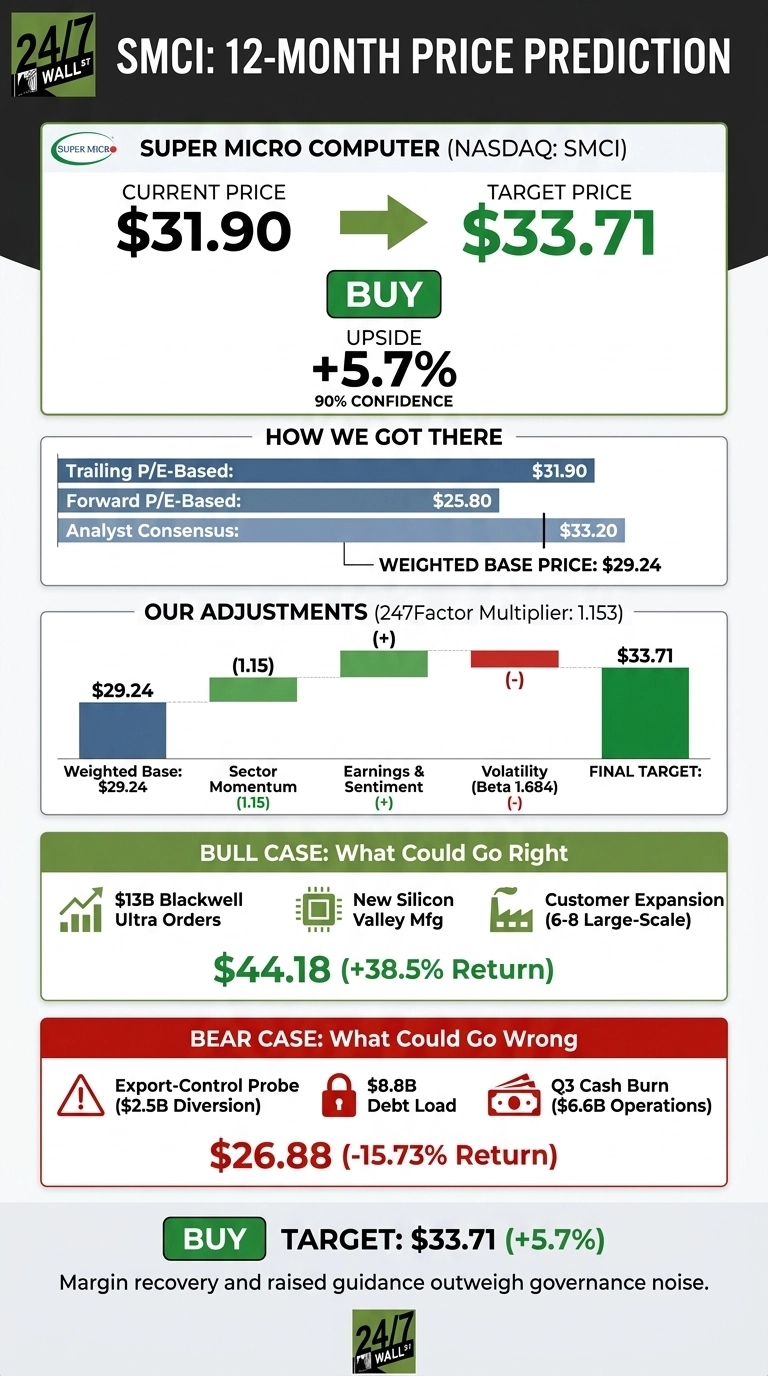

Based on our proprietary model, the 24/7 Wall St. price target for Super Micro is $33.71, implying a 5.7% upside from the current $31.90 price. We rate SMCI a buy with a high confidence level of 90%.

| Metric | Value |

|---|---|

| Current Price | $31.90 |

| 24/7 Wall St. Price Target | $33.71 |

| Upside | 5.7% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Margin Beat That Outshined a Revenue Miss

SMCI just rallied 14.61% intraday after fiscal Q3 results, extending a one-month gain of 19.85%. Despite that bounce, shares are still down 13.49% over the past year and sit roughly 47% below the 52-week high of $62.36.

Q3 FY26 revenue of $10.24 billion missed the $12.45 billion consensus, but non-GAAP EPS of $0.84 beat by 34.51%. GAAP gross margin recovered to 9.9% from 6.3% sequentially, and net income surged 344.38% YoY. Management raised full-year FY26 guidance to $38.9 billion to $40.4 billion. Offsetting this: the results are preliminary and unaudited, with the board reviewing export-control matters tied to a $2.5 billion server diversion to China.

The Case for $44 and Higher

Our bull case puts SMCI at $44.18 within 12 months, a 38.5% total return. The setup is real: a $13 billion Blackwell Ultra order book, expansion from 4 to 6 to 8 large-scale datacenter customers, and new Silicon Valley manufacturing capacity. CEO Charles Liang said “Supermicro’s transformation into a total datacenter infrastructure provider is accelerating”. Recent insider activity skews bullish across 66 transactions.

What Could Go Wrong

Our bear case targets $26.88, a 15.73% drawdown. Co-founder Wally Liaw was charged with conspiring to illegally route $2.5 billion in Nvidia-chipped servers to China, and securities fraud class actions are pending with a May 25, 2026 lead plaintiff deadline. The balance sheet is also stretched: $8.8 billion in bank debt and convertibles and $6.6 billion in Q3 cash used in operations.

Bulls would counter that working capital intensity reflects the inventory build needed to ship the $13 billion Blackwell Ultra backlog, not deteriorating fundamentals. They would also note that JPMorgan raised its price target to $32 from $28 and Citi raised its target to $31 from $25, both citing the margin recovery, even while keeping Neutral ratings on governance.

Our Take on Super Micro, With Eyes Open

Our price target of $33.71 and buy rating reflect a 90% confidence read that margin recovery and the raised $38.9 billion to $40.4 billion FY26 guide should outweigh governance noise over 12 months. The bullish path strengthens if SMCI completes its independent review without a material restatement. The bearish path strengthens if the export-control investigation expands or hyperscaler order cancellations are confirmed. With a forward P/E near 10x, the risk-reward skews favorable.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $33.71 |

| 2027 | $35.50 |

| 2028 | $37.40 |

| 2029 | $39.30 |

| 2030 | $41.33 |

These projections assume Super Micro continues to execute on its DCBBS roadmap and resolves its governance review without major financial impact. Significant upside or downside could result from the outcome of the export-control investigation, AI server demand cycles, and gross margin trajectory.