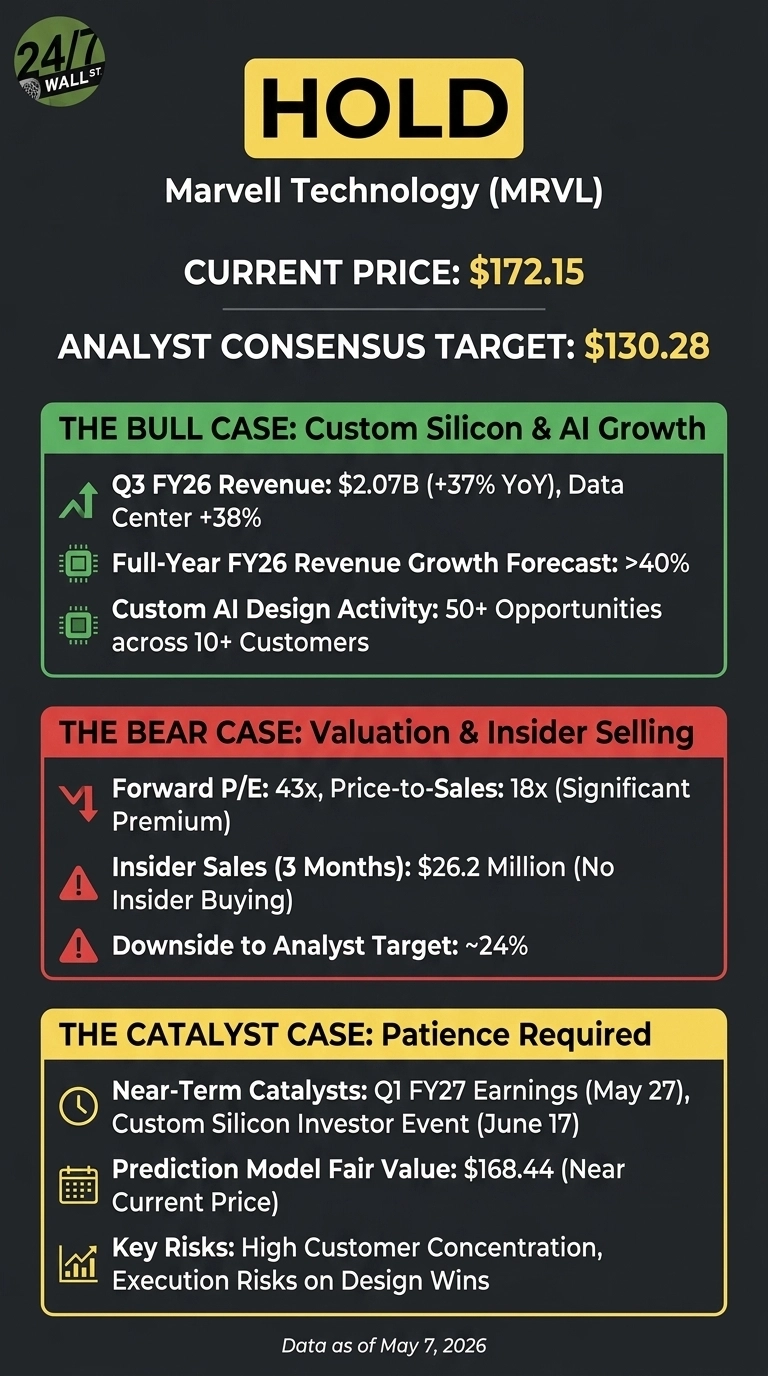

Marvell Technology (NASDAQ:MRVL | MRVL Price Prediction) is a hold at $172.15, with the stock at its 52-week high of $175.79 after a parabolic rally that has fundamentals racing to catch up to price. The question is whether the next leg of the custom AI silicon story is already priced in.

Marvell designs custom AI accelerators, optical interconnects, and networking silicon for hyperscale data centers, with that end market generating 73% of Q3 FY2026 revenue. The move from the high $70s in February to the mid-$170s was fueled by a reported $2 billion NVIDIA investment, a custom chip engagement with Alphabet, and the Celestial AI acquisition aimed at optical interconnect leadership.

The Bull Case: Custom Silicon Is Just Getting Started

Marvell is executing through one of the cleanest growth windows in semiconductors. Q3 FY2026 revenue hit a record $2.07 billion, up 37% YoY, with non-GAAP EPS of $0.76 versus $0.43 versus a year earlier. Data center revenue rose 38%, carrier infrastructure 98%, and enterprise networking 57%.

Q4 guidance calls for $2.20 billion in revenue and EPS of $0.79, putting full-year growth above 40%. CEO Matt Murphy told investors “our data center revenue growth forecast for next year is now higher than prior expectations.” With 50-plus custom AI design opportunities across 10-plus customers and three-nanometer wafer capacity locked in, multi-year revenue visibility is unusually strong.

The Bear Case: Valuation Has Outrun Fundamentals

The Street’s average price target sits at $130.28, implying roughly 24% downside from current levels. Marvell trades at a forward P/E of 43 and price-to-sales of 18. GuruFocus pegs the stock as 62.8% overvalued versus a $101.43 intrinsic value.

Insider behavior reinforces caution. Total insider sales reached $26.2 million over three months with no buying activity, including CEO Murphy’s 318,944-share disposal at $134.60 and EVP Mark Casper’s 10,000-share sale at $135.50 near the 52-week high. The recent cancellation of POET Technologies orders tied to the Celestial AI deal raised execution questions, and gross margin has compressed as lower-margin custom silicon scales.

The Case for Patience

Both sides hold real ground. The fundamental trajectory is accelerating, yet price has sprinted ahead of every published target. Marvell’s prediction model places fair value at $168.44, just 2.2% below current, suggesting the stock is fairly valued at current levels.

Two near-term catalysts will shape the verdict. The custom silicon investor event on June 17 should quantify design-win pipeline and market share goals, and Q1 FY2027 earnings on May 27 will test whether momentum persists. Buying ahead of those proof points means paying peak multiples; selling means abandoning a structural AI winner.

The Numbers in Context

At $172.15, Marvell carries a market cap near $147.6 billion, a trailing P/E of 55, and EPS of 3.08. Of 43 analysts covering the name, 36 rate it Buy, 6 Hold, and 1 Strong Sell, the consensus target of $130.28 sits well below current levels.

Performance has been historic: shares are up 102.82% YTD and 181.96% over one year, against a S&P 500 YTD gain near 6%. April alone delivered a 66.7% surge.

At $172.15, Marvell Technology Is a Hold

The bull thesis is real but priced in. Custom AI silicon, NVIDIA NVLink Fusion integration, and optical interconnect leadership justify a premium, yet not one requiring every catalyst to land perfectly. With analyst targets 24% below current and insiders selling from $99 to $135, the asymmetry has flipped against new buyers.

The path to a Buy upgrade runs through the June 17 investor event and the May 27 earnings report. Concrete custom silicon revenue guidance for FY2027, expanding gross margins, and visible hyperscaler diversification beyond the lead customer would change the math. The path to a Sell runs through hyperscaler in-housing, a custom program loss, or a broader AI capex reset.

The cost of patience is missing further upside in a momentum name with a beta of 2.25. The cost of acting prematurely is buying a 43x forward earnings stock at the moment management and insiders are monetizing.

Marvell remains a structural AI winner, but at the 52-week high with the Street’s average target a quarter below the price, the disciplined call is to wait for the next reset rather than chase the rally.