Key Points from 24/7:

-

- This Redditor recently hit their own magic net worth number.

- The question here is whether or not to hire a financial planner.

- There is also some fear over the wife leaving a high-paying job.

While we all dream of hitting the day when we have millions of dollars in the bank, it might feel overwhelming when it arrives. In the case of one Redditor in the r/fatFIRE subreddit, they’ve hit a magic number of $2 million and now have to decide if it’s time to hire someone to help manage how to continue growing family wealth.

This post shows a working couple with small children and a now sizable liquid net worth. The wife is also looking to leave her job. So, we step into an age-old question about when it may be right for someone to shift away from a job to care for the family’s small children.

What intrigues me most about this post is that I’ve been down this road, minus the $2 million net worth. My wife and I waited until I hit a certain income level before she felt comfortable stepping away from her career to raise a family.

The Scenario

With this scenario, we only have a few things to consider to answer the original poster’s question. First and foremost, he and his wife, both in their mid-30s, just hit a $2 million liquid net worth. The wife, currently a partner in her law firm, is looking to leave her job to focus on raising the couple’s small children. Unsurprisingly, there are some nerves about losing what is likely a sizable income and going to a one-income lifestyle.

The Redditor asks his fellow r/fatFIRE members when they may have considered utilizing a financial advisor. He notes that he generally focuses the family’s money on Vanguard index funds, and by all accounts, this has worked well for them.

What’s notable here is that this individual clearly did something right to get a $2 million liquid number. If it were that easy, everyone would be doing it, so somewhere along the way, some intelligent decisions were made about investments.

The Recommendation

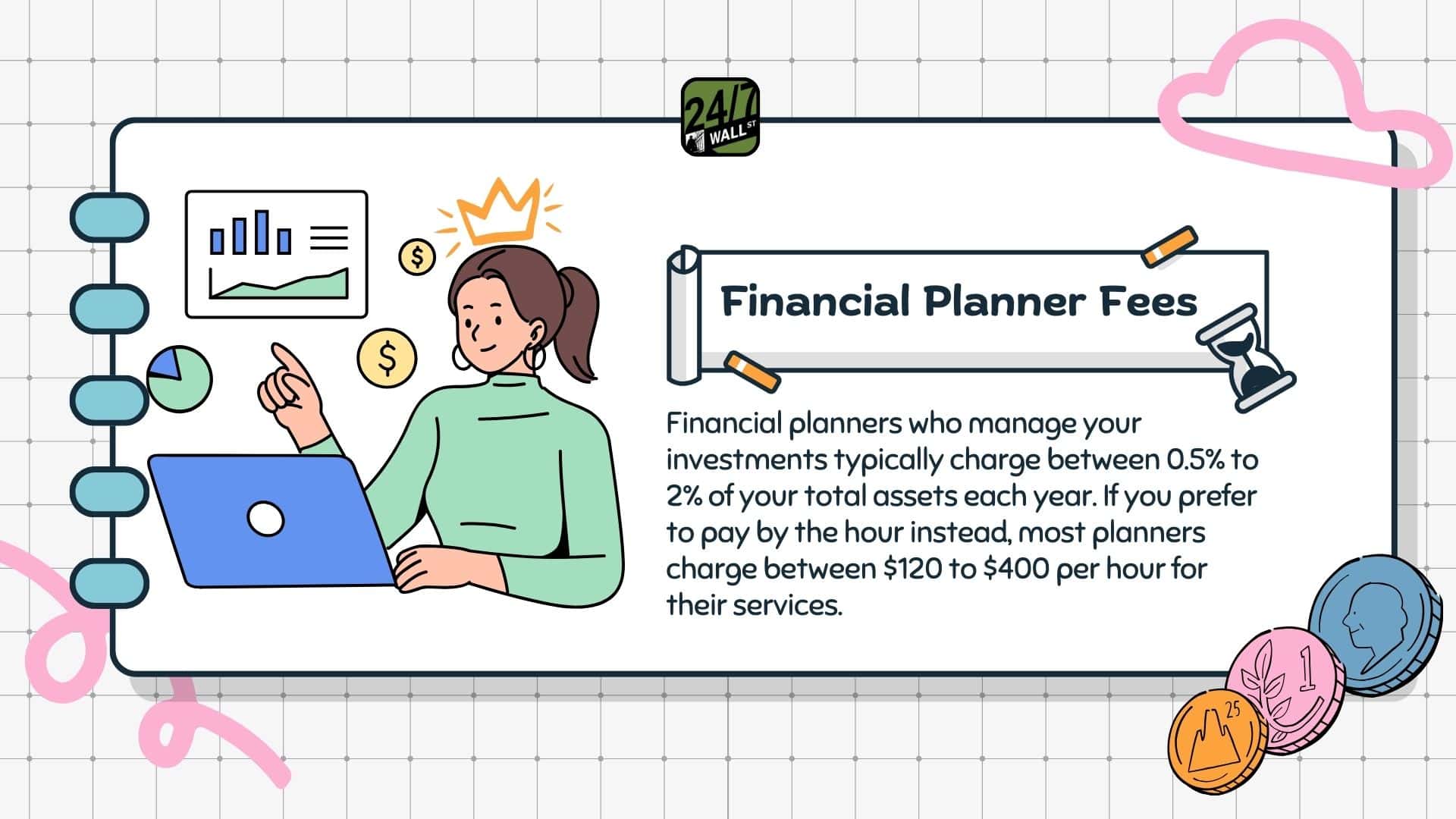

I emphasize that I am not a financial planner, so this should not be considered financial advice, but I agree with one comment in this post above all others. In this case, someone notes there are more than just two options here: using a financial advisor or not. Instead, you can find someone to review the family’s current economic status and devise a plan. This would be a one-time deal and not require you to pay 1% annually to someone to manage your money.

In other words, you can start small by at least seeing if there is advice you may need to become more familiar with. If so, then you have some additional knowledge to make a decision. However, as other commenters point out, a financial advisor may not be the most necessary move here. Instead, hiring an estate planning attorney and a tax consultant is the first move. Understanding if there are ways the family can take advantage of different write-offs to offset taxes from things like capital gains is a wise move.

The Takeaway

Here’s the good news and my takeaway from this post: This Redditor is already setting up his family for life. While there is no doubt that the wife’s missing income will have some shock value and cause the family to reset its budget, it’s not the end of the world.

I read here that the original poster’s husband is already doing something right. Growing a net worth using Vanguard funds to $2 million is more than just picking and choosing random stocks. Some strategy and risk are involved, so it’s safe to say there is above-average knowledge of the market here. This said, for now, I’d say skip the financial advisor, at least one that requires an annual take, and instead speak with a tax consultant and start from there. However, if the family really wants peace of mind about their future, they should reach out to an advisor.