Key Points from 24/7:

- The father-in-law, in this case, is very controlling.

- The parent is worried the FIL will make a mistake investing in a college fund.

- The Redditor also doesn’t want to annoy the father-in-law.

- Also: Are You On Track to Retire? Take This Quiz and Find Out (Sponsored)

When it comes to family money, understanding how it should be dealt with can lead to more questions than answers. This is especially true when setting up trusts or college funds for families. For better or worse, instead of just writing a blank check, many grandparents like to open up accounts and let the money grow. This is exactly the case this Redditor explains with his post in r/personalfinance.

As much as this should be easy, the Redditor quickly points out that his father-in-law isn’t open to suggestions. We’ve all been there with family when we should just shut up, but we also want to have a voice when our children are involved.

What I love about this scenario is that I have already been down this road. My in-laws have already established a college fund for my children, and I had no say in how it was established.

The Scenario

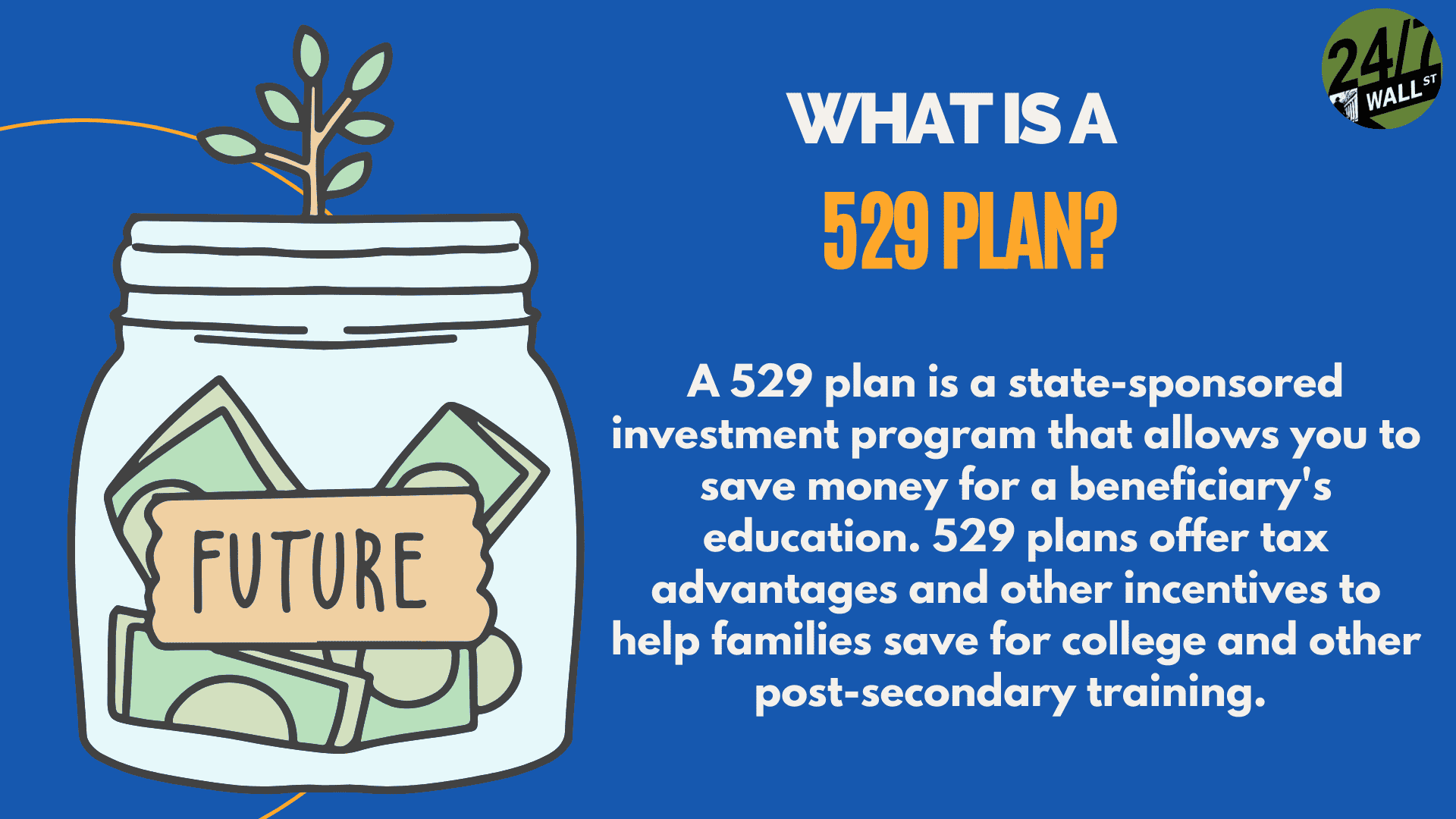

In this particular scenario, the Redditor finds himself in a position where the family can add to existing 529s he and his wife have already established. However, the father-in-law isn’t interested in contributing to what already exists. Instead, he wants to set up something on his own that he alone has total control over. He sounds like a really fun person.

Here, we have a case where the Redditor is trying to help his father-in-law choose between two scenarios: a UMTA or another 529 that the father-in-law sets up independently.

As both have benefits and a negative or two, it is a situation worth discussing with the father-in-law. However, if the person you are talking with isn’t reasonable, it’s hard to “make” a recommendation, no matter how well thought or intended it might be.

The Recommendation

I should emphasize that I am not a financial advisor and don’t play one on television. So, any recommendation I give is based on personal experience and understanding of these issues. If you want concrete answers, talk with a financial advisor.

With that little disclaimer out of the way, I, like the rest of the Reddit comment section, agree that the poster should stop getting involved and let the FIL open a 529. As it offers no tax implications and would allow the father-in-law direct involvement, it sounds like a win-win for both the children and the grandparents.

On the flip side, you have a UMTA, which, on the positive side, allows the money to become the children’s when they turn 18. Of course, this means they are not only responsible for any taxes but also don’t need to use the money for college. In addition, because it becomes their money and goes into a bank account, it may affect any requests for financial aid as the child would show they have the means to pay for school.

A 529 wouldn’t immediately exclude financial aid, which is more likely with a UMTA, depending on its size. Personally and again, my recommendation is to give the father-in-law as much space as possible to make this decision but gently, and I do mean gently, steer him toward a 529.

The Takeaway

The most important thing to remember is that this isn’t about you or the father-in-law. It’s about your children. The best thing that can happen is that the combination of the money the Redditor has already put aside in a 529 plus that of the father-in-law would be enough to completely fund an education without additional loans, financial aid, etc.

Even if the father-in-law isn’t going to make a significant contribution, as the poster mentions, it’s likely more in the thousands than tens of thousands, it’s the thought counts. Instead of worrying about how to guide him, thank him for the help and move on. This is the best move the Redditor can make.