24/7 Wall St. Key Points:

- Early retirement is a goal for many. But, for others, it may not happen on our terms. Still, that doesn’t mean that it can’t be fulfilling and successful.

- By adjusting financial goals, exploring part-time opportunities, and considering new investment strategies carefully, you can adjust your retirement strategy to a late job loss.

- Also: Take this quiz to see if you’re on track to retire (Sponsored)

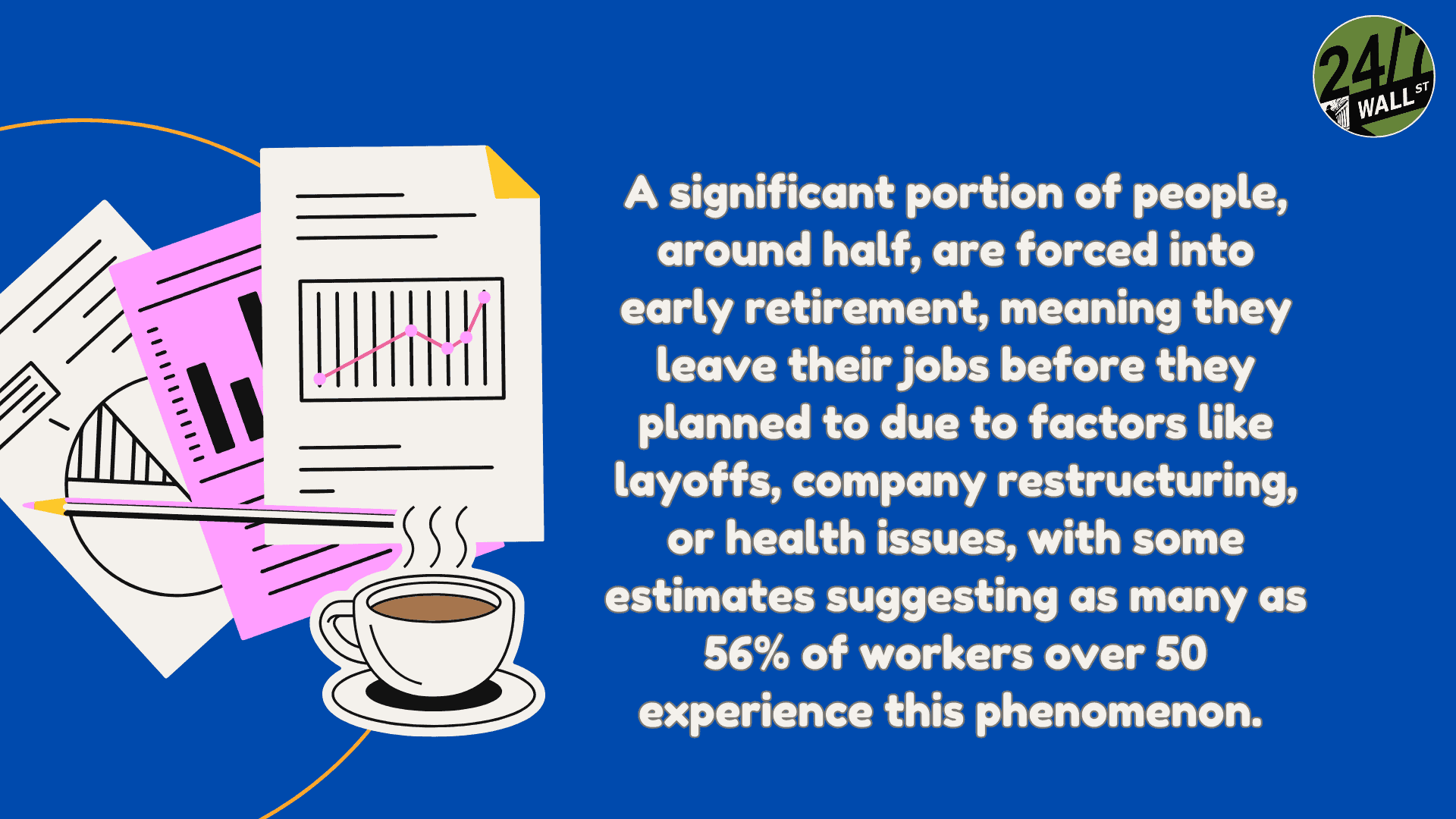

Finding yourself in an early, unexpected retirement situation—what some call “forced” Financial Independence, Retire Early (FIRE)—can feel overwhelming. If you’re close to retirement, suddenly losing your job can be both freeing and incredibly stressful!

A Reddit post I read sums this up perfectly. The Redditor shares a story many might relate to: being close to retirement goals, only to have circumstances change, pushing FIRE forward before reaching the target “number.”

Here’s my advice for this poster and others on a similar path. As always, this is my advice, not financial advice.

1. Reassess Your Target Number and Spending Needs

The poster planned on hitting a certain financial goal. However, does he really need that to retire? It’s now time to reassess his target number and figure out what he truly needs in his retirement versus what’s ideal.

His original goal might not be achievable, but that might be okay!

Consider if you’re on track to retire and if those few more years would make that much difference.

2. Explore New Work Possibilities

Because his role was eliminated, he now has the perfect opportunity to find a new, lower-stress role. He could even potentially shift into a different field that he finds more fulfilling, even if that means taking a few extra years to reach his goal. The extra income could provide some more oomph, and he could potentially lower his retirement goal to better match his new situation.

For the poster, exploring executive recruiting or related fields could offer flexibility without the pressure of a demanding corporate role.

There is also the potential for part-time or consulting work. This often lowers stress while providing some extra income to bridge any retirement gap.

3. Consider Alternative Investment Strategies

The poster mentions using a securities-backed line of credit (SBLOC) to reinvest in real estate or business opportunities. This is a good way to provide some extra cash flow without selling assets. However, it does come with risk, especially for those less familiar with real estate.

Before diving in, get a solid grasp of the risks and potential returns, and consider working with a financial advisor experienced in alternative investment strategies.

There are some strategies that may work better in this situation, but they aren’t without their risk! Anything with potentially higher gains is also going to be riskier.

4. Consider Lifestyle Adjustments

Sometimes, it’s easier to lower your spending than find more money. The poster has expressed reluctance to reduce spending. However, a slight financial adjustment can go a long way (such as taking one less vacation a year or eating out one fewer days per week).

You can make very small adjustments and pair these with a part-time job, potentially allowing the poster to meet his financial goals.

Consider what is truly adding value to your life. You may be surprised by the number of things you can cut.

5. Address Potential “Windfalls”

It’s easy to rely on a possible inheritance or other possible “windfalls” for retirement. However, I don’t recommend planning for any of these things until the money is in your bank account. You should not rely on the work of others to fund your lifestyle.

It’s best to have a plan that doesn’t rely on someone else to be fruitful!