24/7 Wall St. Key Takeaways:

- While growth is wonderful to see in a 401(k), it’s important not to become too invested in a single company.

- Managing the taxes on this growth can also require a bit of finesse.

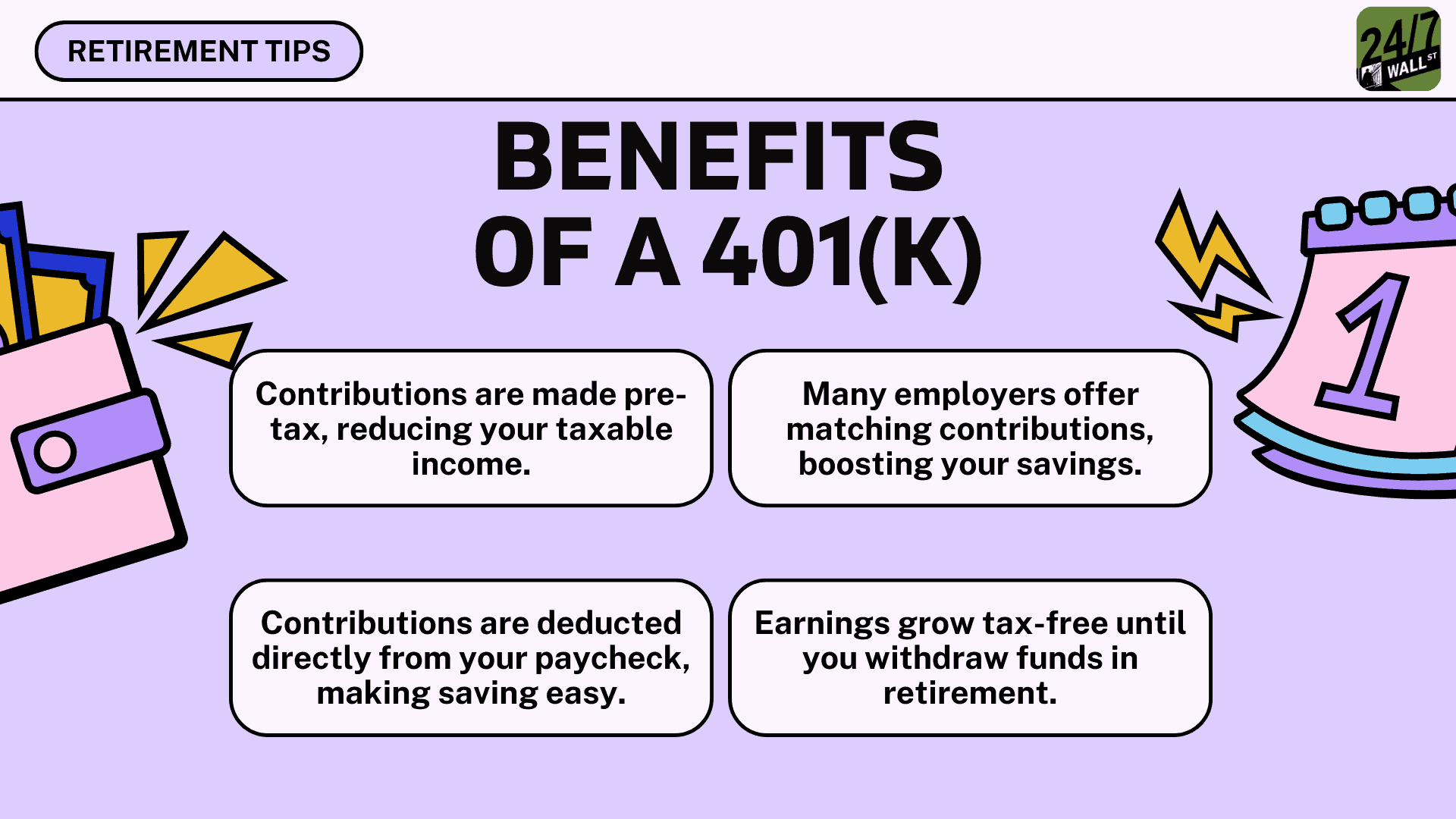

Managing the taxes on a growing 401(k) as you approach retirement can be daunting, especially if you’re seeing a large amount of growth. For one Reddit user, a $5 million 401(k) is projected to grow to $8-9 million by age 62, and they’re looking for smart ways to handle the potential tax burden.

With the company’s stock swelling in value, strategic tax planning is essential to ensure that this portfolio remains beneficial without being eaten up by a high tax rate. Several options, like diversification and Roth conversion, can help reduce this tax liability.

In this article, we’ll explore the potential ways to manage the taxes on this growing retirement portfolio.

Why We’re Covering This

When it comes to finance, learning from others’ situations is one of the best ways to develop a wise financial plan. According to a recent study by Vanguard, the average 401(k) balance for Americans between the ages of 55 and 64 is $244,750. So, while you might not be in this exact situation yourself, you never know when some wisdom gleaned from another’s situation will help yours. And if $5 million seems like an unattainable amount, remember… Just $600 contributed per month for 40 years, at a 11.50% rate of return (the nominal annualized total of the S&P 500 from 1983 to 2023) would have grown to around $5 million today!

The Situation

- Our Reddit poster is 56 years old with nearly $5 million in a 401(k), largely due to company stock growth.

- If the stock continues to increase, the poster projects that their portfolio could reach $8-9 million by age 62.

- The poster was seeking advice on how to manage taxes when they retire +.

Our Response

Seeing someone’s 401(k) perform so well is amazing, especially with the continued growth that’s expected. Approaching retirement with $5 million, and potentially $8-9 million, is a fantastic position to be in! However, there are several suggestions we’d recommend keeping in mind to help manage taxes at retirement:

Pros of the Poster’s Current Situation

- Strong Company Stock Growth: Having a large portion of your retirement savings growing rapidly is great for building wealth.

- Long-Term Potential: With continued growth, the poster is well on track to a comfortable retirement by age 62 (or even earlier).

Potential Concerns

- Overconcentration in Company Stock: Relying too heavily on one stock can increase risk. Over time, more and more of their wealth will be tied into a single stock, potentially leading to large losses in the future.

- Tax Implications of Withdrawals: Since the 401(k) will be taxed as ordinary income upon withdrawal, large distributions may push the poster into a higher tax bracket during retirement.

Considerations

There are several potential approaches the poster could take:

- Net Unrealized Appreciation Strategy: One approach would be to explore the NUA tax strategy. This approach allows you to move company stock from your 401(k) into a taxable brokerage account, paying capital gains tax rather than income tax. This strategy can reduce your tax burden when a stock has grown heavily.

- Roth Conversions: Another potential strategy is to convert some of the 401(k) into a Roth IRA before you start withdrawals. You’ll pay taxes at your current rate, but future withdrawals would be tax-free. If you expect the money to grow even further in the future, this could be beneficial.

- Required Minimum Distributions: Once you reach the age of 73, you must take the minimum amount required from your 401(k). It’s worth considering how large those distributions will be and how that may impact your tax situation. Plan your withdrawals around these future requirements.

- Timing Your Withdrawals: You can be careful with your withdrawals to stay in a lower tax bracket, minimizing the amount of taxes you’re required to pay.

Talk to a Pro

Lastly, this individual could benefit significantly from working with a financial advisor due to the complexities of managing a rapidly growing 401(k) heavily invested in company stock. A financial advisor can help diversify the portfolio to mitigate risks associated with overconcentration. They can also provide strategic tax planning, such as exploring Net Unrealized Appreciation (NUA) strategies and Roth conversions, to reduce tax liabilities upon withdrawal.

With potential large distributions that may push them into higher tax brackets and required minimum distributions to consider, professional guidance is crucial to optimize their retirement funds and ensure long-term financial security.