Key Points from 24/7 Wall St.

- A high-yield savings account could help you earn a nice return on your money without taking on the risks associated with investing.

- Shop around for a great rate and choose your bank carefully.

- Understand what a savings account can and cannot do for your finances.

- The best high-yield savings accounts are paying way more than most Americans realize, with some offering cash bonuses for new accounts. Click here to see our top pick today. (Sponsored)

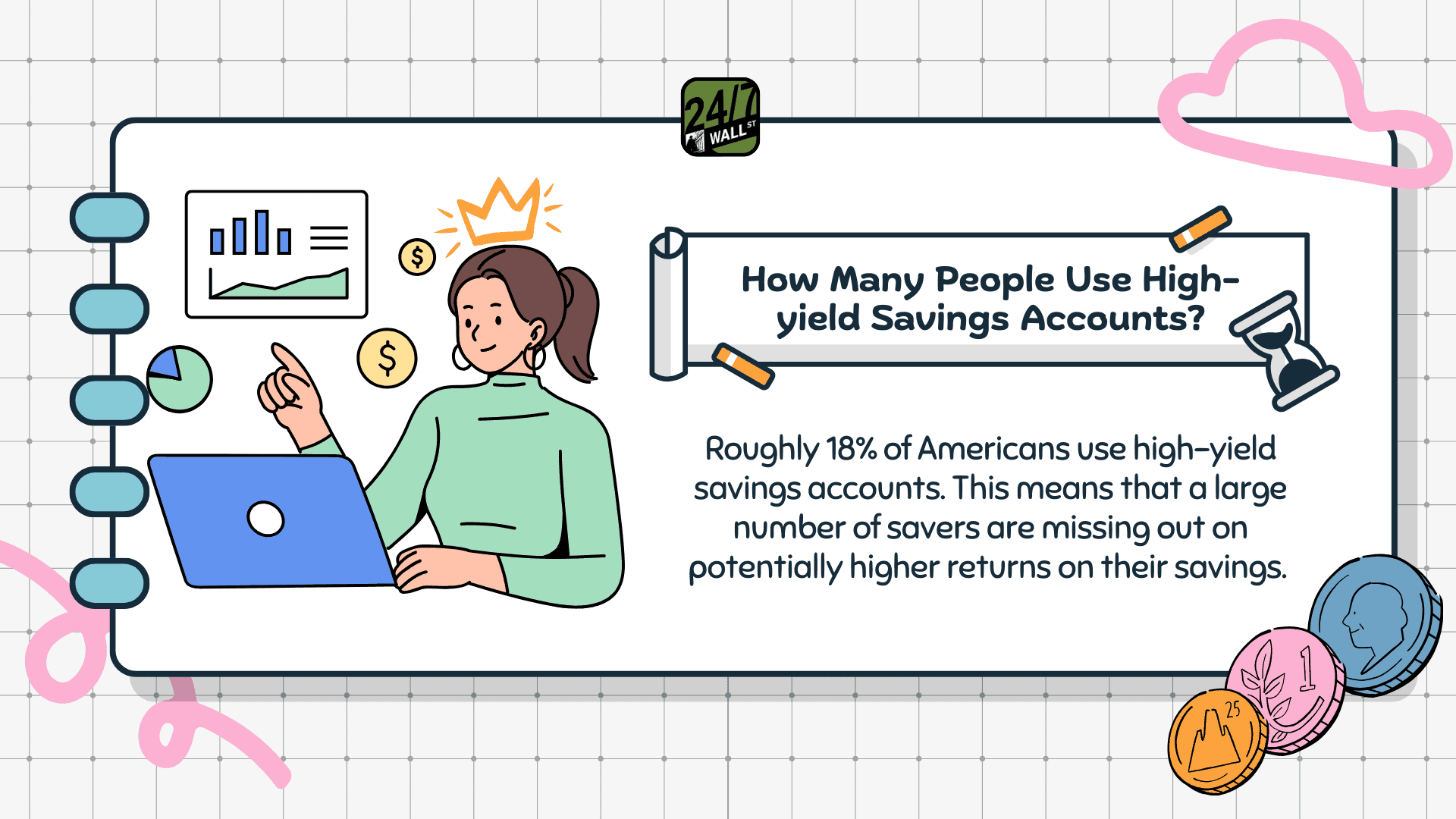

There are certain financial products that not everyone needs. Annuities, for example, can be a good source of predictable income for retirees, but they’re not suitable for everyone. Similarly, a lot of families can benefit from whole life insurance, but it’s not the right choice for many folks.

A high-yield savings account is different in that pretty much everyone, regardless of age, assets, or income, can benefit from one. And if you’re new to having a savings account, here are some basic things you should know before you dive in.

Not all savings account APYS are created equal

The amount of interest you’re able to earn on your savings will depend on your APY, or annual percentage yield. There are no rules with regard to APYs – each bank can set its own.

APYs on savings accounts typically rise and fall in line with the federal funds rate, which is what banks charge one another for overnight borrowing. Right now, many high-yield savings accounts are paying around 4%, but savings account APYs also aren’t set in stone and can change with market conditions.

It’s important to read the fine print before opening a savings account based on its APY. There may be certain requirements you need to meet to snag the advertised rate you see, like a minimum balance you may or may not have.

It’s important to understand the terms of your account

It’s natural to chase a high-yield savings account with the best APY you can find. But it’s also important to know what terms you’re signing up for.

It’s not unheard of for bank accounts to charge different fees, so look closely at what those might entail. Also, see if your account is subject to withdrawal limits or any other rules that might be a problem.

There’s no reason not to have protection

When you invest money, you risk losing out on principal if your portfolio value tumbles. The nice thing about high-yield savings accounts is that your principal is protected in the amount of up to $250,000 per depositor, per account, provided your bank is FDIC-insured.

Given the number of banks that have FDIC insurance, this shouldn’t be a difficult requirement to meet. If you’re not sure whether the bank you’re thinking of opening an account with is FDIC-insured, you can use this tool to find out.

You must have realistic expectations

The purpose of opening a savings account – and the reason everyone needs one – is to have a safe place to house your cash. You need money in savings at all times for emergency expenses, like home repairs or to cover your bills in the event you’ve been laid off. And you can’t take the risk of investing money you’re earmarking for emergencies, because if you need funds at a time when your portfolio is down, it could have unfavorable long-term consequences.

At the same time, your best bet is to use a savings account as a home for your cash – not as a means of meeting your long-term financial goals. If you’re putting funds away for retirement, or if your kids are very young and you’re saving to pay for their college education, investing your money is likely to yield better results than earning interest in a savings account.

Remember, too, that high-yield savings accounts are paying pretty generously today, but that streak may gradually come to an end. That’s not a reason to ditch your savings account. Rather, it’s a reason to use other accounts to meet major goals, and to use a savings account to earn some interest on your money while keeping it secure.