People who work for companies large enough to offer 401-K plans are fortunate if their employers include matching contributions. The additional retirement funds can be a welcome accelerant towards wealth building via a combination of growth and dividend compounding. However, failure to monitor one’s 401-K account particulars and details can result in missed opportunities and thousands of dollars unnecessarily left on the table. An unfortunate anonymous employee found this out the hard way, and took to Reddit to both vent and warn others about the hard lesson he learned.

401-K Basics – A Review

The use of pre-tax funds in a 401-K plan defers the taxes until retirement age, giving the participant extra leverage for wealth building during their productive years.

A quick overview of 401-K Basics helps to both frame and delineate some of the elements that may have contributed to the poster’s confusion:

- A 401-K plan is a company-sponsored retirement account. Employees contribute their designated percentage of their income to be allocated. Employers often may offer to match at least a portion of these contributions. Contributions are made with pre-tax funds.

- There are two types of 401-K account categories: traditional and Roth—which differ primarily in how they’re taxed. Assuming one is over age 59 ½, traditional 401-K withdrawals are taxed as income at the participant’s income bracket at the time of withdrawal, while Roth contributions are made with after-tax funds, so subsequent withdrawals are tax-free.

- Employer contributions can be made to both traditional and Roth 401-K plans while solo 401-K companies provide plans for people without employers.

- There are specific rules governing when one can withdraw money from a 401-K account without penalty.

ERISA Compliance

Michael Douglas won an Oscar for his portrayal of corporate raider Gordon Gekko in the film “Wall Street”, where his character plans to raid an airline pension fund in violation of ERISA laws.

In the film, Wall Street (1987), Michael Douglas’ Gordon Gekko antagonist is arrested for insider trading. However, the target of his insider trading, Blue Star Airlines, was with the intent to acquire the company and raid its pension fund upon liquidation. This would have been a blatant violation of ERISA laws, and Gekko would have few, if any options to conceal it, so Feds would have inevitably raided his offices anyway.

ERISA is the acronym for the Employee Retirement Income Security Act. It is the legal Federal guideline rulebook governing the handling of pension and retirement account monies that are managed by private sector employers on behalf of their employees. ERISA rules and protections include:

- Worker Protections: ERISA provides a comprehensive framework to ensure the integrity and legality of employee benefit plans, which covers most employer-sponsored 401-K plans.

- Fiduciary Duties: 401-K plan fiduciaries are required to act solely in the best interests of the retirement investors, a rule designed to safeguard retirement savings. However, this errs towards principal safety as an overriding imperative over any growth initiatives. Most fiduciaries preselect a range of different Exchange Traded Funds, Closed End Funds, and/or mutual funds of different compositions and objectives to suit a wide range of investor goals and risk tolerances.

- Compliance: ERISA compliance requirements are essential for plan sponsors to maintain a current legal and health status of their benefit plans.

- Disclosure Requirements: 401-K plan administrators must file annual reports, such as the Form 5500, and provide plan participants with important documents like Summary Plan Descriptions (SPD), which explain the plan’s features and benefits.

Depending on the nature of the violation, ERISA penalties can range from daily fines of $1,000 to 10-year jail sentences for willful violations, with fines as high as $500,000 or greater.

Why Reading The Fine Print For Each 401-K SPD Is So Important

Ignoring his new job’s 401-K plan Summary Plan Descriptions (SPD) disclosure from the company’s fiduciary cost the Reddit poster tens of thousands of dollars in potential gains.

The aforementioned Reddit poster explained his dilemma as follows:

- He was hired by a new company two years ago. He was informed that his 401-K funds would be contributed to a Fidelity SPAXX account.

- Two years in, the poster looked at his account and saw only minimal gains.

- His previous employer had investments with Vanguard that displayed considerably greater growth.

- The poster pondered whether he should move the account out of SPAXX.

A number of items immediately became apparent to both respondents as well as Reddit readers at large:

- The poster has never bothered to look more closely at his investments in either job. He assumed generically that Vanguard automatically invested for capital appreciation and that Fidelity would do likewise.

- He clearly never familiarized himself with the 401-K SPD documents to be aware of his investment options, nor had he ever spoken with the HR department about a discussion with a financial advisor.

- It is only serendipitous that he took notice early enough to take steps to change the makeup of his 401-K portfolio to start regaining loss growth opportunities over the past 24 months.

The poster has subsequently invested his 401-K account in S&P 500 Index ETFs. Had he read the SPD, he would likely have realized that the fiduciary was awaiting instructions from him as to which menu options he wished to invest the 401-K account in, and what the percentage of allocations would be. Since fiduciaries are very wary of staying compliant with ERISA rules, they cannot exercise discretion over the account, and must keep funds safe in a money market account like SPAXX until they receive participant client instructions.

Bringing ERISA Into The 21st Century

President Trump signed the Democratizing Access for 401(k) Investors Executive Order on August 7, 2025, which seeks to change ERISA restrictions on lucrative alternative assets like real estate, private equity, and cryptocurrencies, which have been prohibited in 401-K accounts since ERISA went into effect.

Due to its overriding concerns over principal protection above all else, ERISA restrictions have hampered many 401-K plans from capitalizing on certain types of investments that have proven lucrative. For example, Life Settlement Policies, which companies like Coventry Direct buy and sell in the secondary market, are prohibited. Another asset class is precious stones, such as diamonds, emeralds, and rubies. Real estate and private equity investments are also not allowed.

In acknowledgement of how much better information access is now available due to the internet, President Trump signed the Democratizing Access for 401(k) Investors Executive Order on August 7, 2025. The EO instructs the U.S. Department of Labor and other federal agencies to re-examine guidance under the Employee Retirement Income Security Act of 1974 (ERISA) regarding fiduciary duties related to alternative asset investments in 401(k) plans and to consider issuing rules and regulations that include fiduciary “safe harbors” that may curb the risk of fiduciary litigation. The alternative assets in question include: cryptocurrency, real estate, and private equity.

The EO also directs the SEC to consider revising the definitions of “accredited investor” and “qualified purchaser” to expand access to alternative assets for plan participants in defined contribution plans. Current SEC restrictions set a high bar that a majority of plan participants are unable to meet for qualification inclusion status.

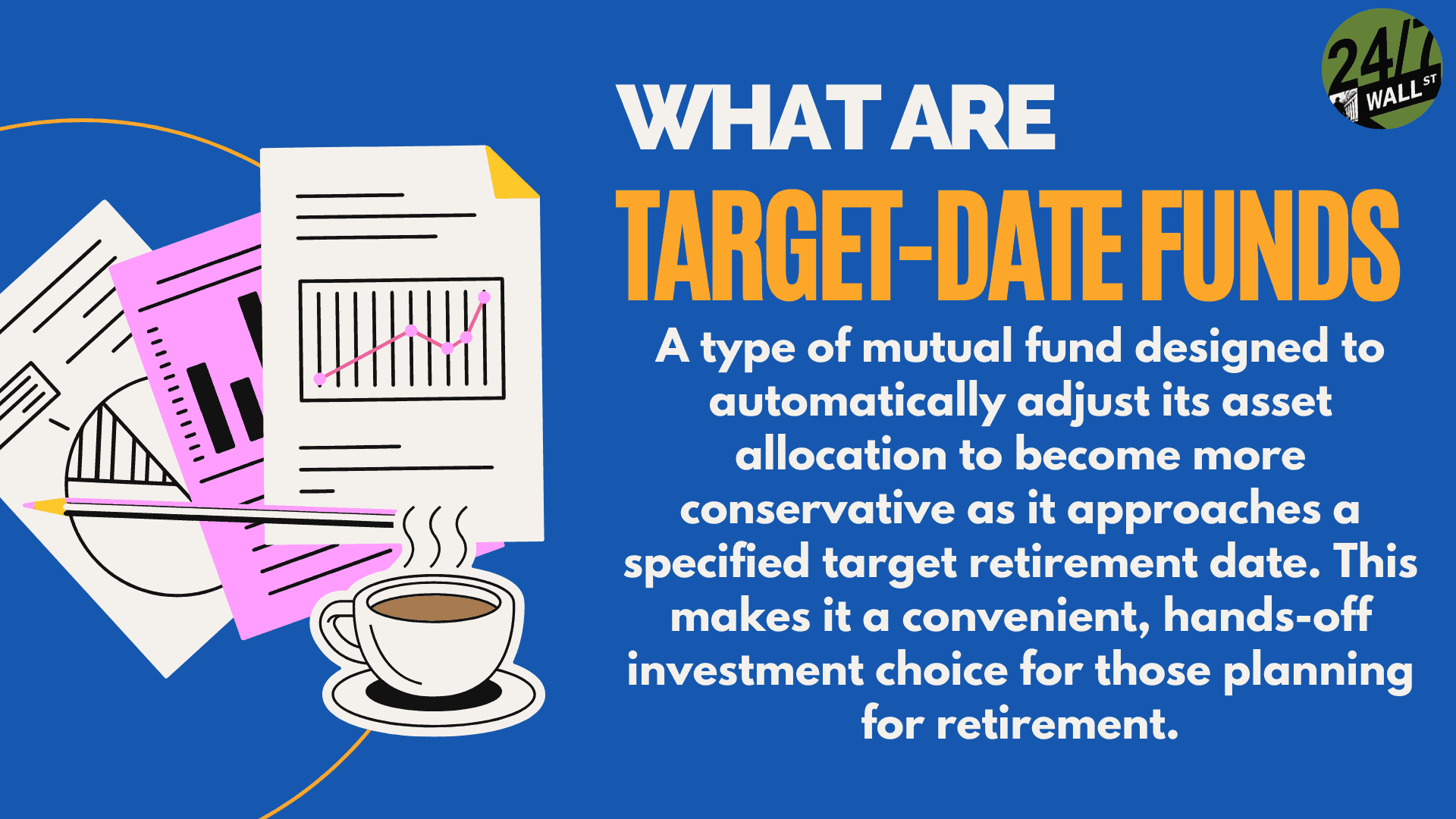

Target Date Fund

Target Date Funds are the ultimate in “set it and forget it” autopilot investments for those who have no interest in learning about their investment product options.

While participants deserve a greater deal of flexibility for their 401-K account investment options, there is a significantly large contingent that prefer not to engage in researching the various types of investments and in weighing the corresponding merits and pitfalls of each. For those people, there is a simple option: if available, invest in a target date fund. This is usually in conjunction with a Vanguard, Fidelity, or other large institution.

One submits the dates in which they will turn 65, when they plan to retire and their financial goals. The target date fund algorithm then calculates the projected returns from within its family of funds to maximize growth in the early years and then gradually switch asset classes as the target date approaches to reduce risk. It is the ultimate in “set it and forget it” convenience.