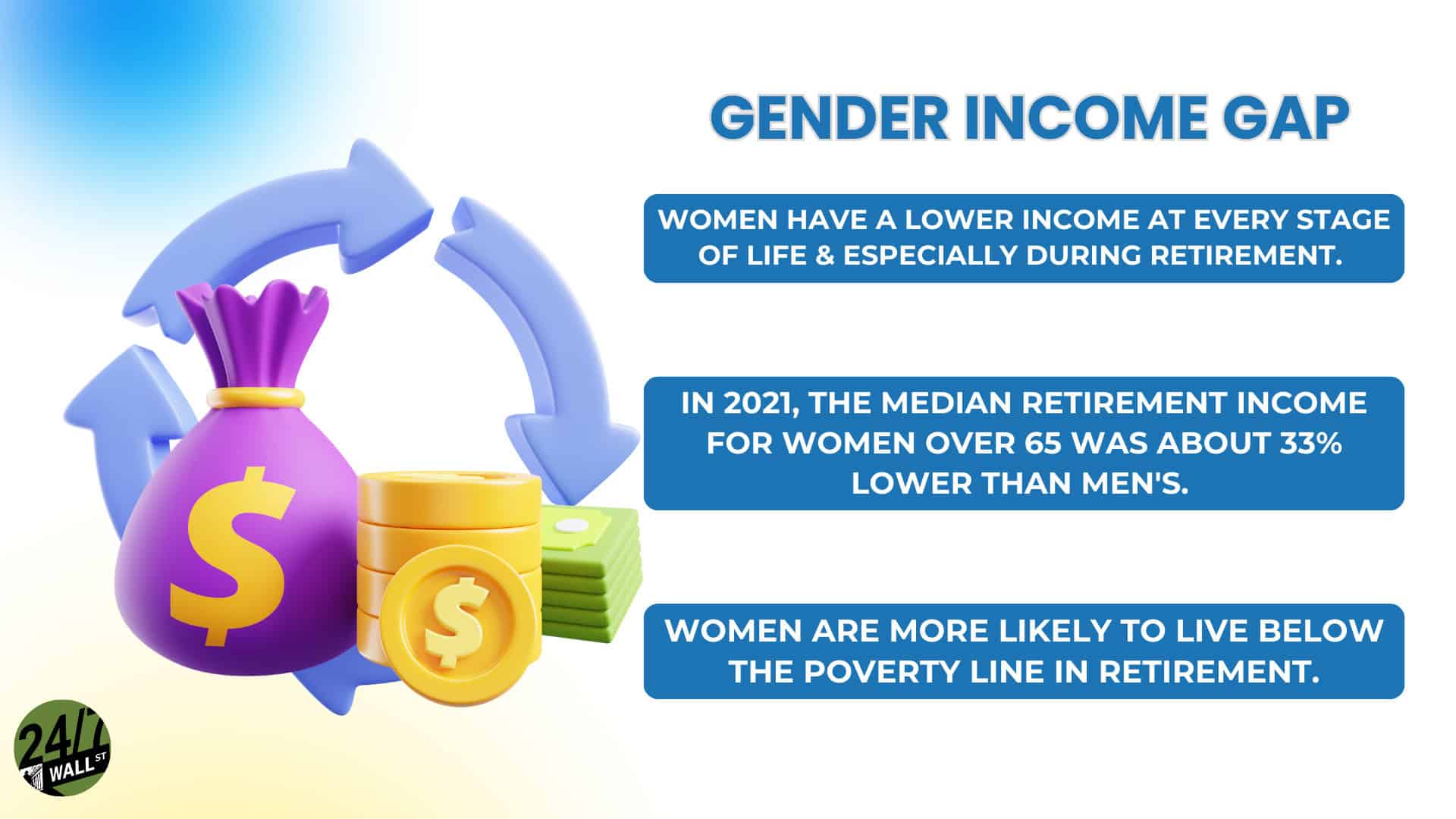

Discrepancies in salaries within a marriage are common and can stem from differences in career fields, education, work experience, or personal choices about balancing family and professional life. While income gaps don’t inherently cause problems, they can create tension if couples don’t openly communicate about expectations, financial responsibilities, or feelings related to money and contribution. Some partners may feel pressure, guilt, or resentment depending on who earns more, while others may struggle with societal norms around gender and income. Healthy relationships tend to navigate these differences by focusing on teamwork—treating the household as a shared unit rather than a competition—and by developing financial plans that reflect mutual goals, transparency, and respect for both partners’ roles.

Unequal individual pre-marriage net worths can exacerbate the awkwardness of even approaching the topic. The following are among the pro and con questions that may crop up:

- Does the couple have a prenup?

- Are there health insurance, tax status declarations, etc. that should change or remain the same?

- What kind of long-term retirement plans can be made that will suit both spouses’ goals and expectations?

This post was updated on November 21, 2025 to include an overview on salary discrepancies within marriage.

A New Bride’s Retirement Concerns

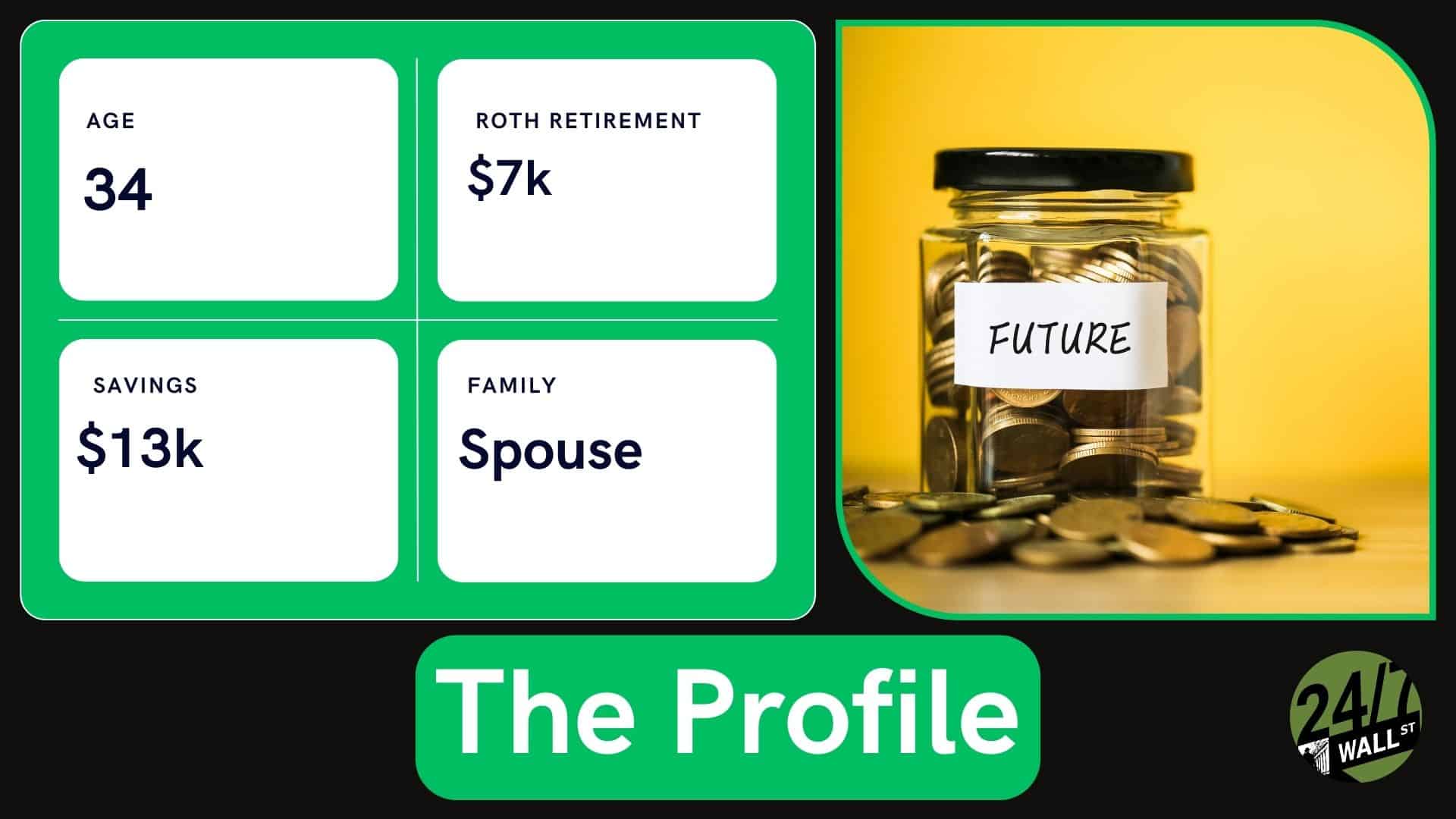

After an 8-year courtship, a 34-year-old recently married woman posted her requests for retirement advice on Reddit. Perhaps the questions stem from financial insecurities and the statistical high rate of divorce. Perhaps they stem from her relative lack of financial management savvy when she compares herself to her husband. The details she disclosed include:

|

Assets |

Him |

Her |

|

Income |

4X |

X |

|

Roth IRA account |

$100K+? |

$7,000 |

|

Savings Account |

$60,000 |

$13,000 |

|

401-K |

$100K+? |

$8,000 |

|

High-Yield Savings Account |

$100K+? |

$0 |

|

Totals |

~$360,000+ |

$28,000 |

The couple have since opened a joint bank checking and savings account, as well as a joint High-Yield Savings Account with $20,000 received as wedding gifts.

The poster’s primary concerns are being screwed over financially when older and being unable to financially provide for herself in her twilight years, while her husband might be enjoying a much better lifestyle.

Setting aside the likelihood that she would inherit her husband’s wealth in the event of his early demise, her concerns seem to stem around a potential divorce down the road, or perhaps a fear that her husband won’t provide for her during retirement. While there is insufficient evidence to make any judgments about their marriage, the fact that the husband has opened a pair of joint banking accounts with her might indicate that the fears are unfounded, However, there are some practical steps that the couple can take to provide for contingencies as well as better plan for their golden years.

Taking the Long View Plan Approach

Taking the Long View Plan Approach

Given the husband’s cooperation to date and the poster’s concerns, a prudent first step would be to create a Joint Retirement Plan. Some of the areas where they need to find agreement entail:

- What age does each spouse want to start collecting social security?

- How to maximize each spouse’s Roth IRA and what type and amount of contributions can the husband possibly contribute to the wife’s smaller IRA?

- What are the best ways to maximize each spouse’s 401-K or employer matched plan?

- What kinds of passive income or freelance work can impact eligibility for retirement benefits and what limitations should be kept in mind in advance?

- What is the desired lifestyle and projected costs for their retirement years?

- What potential retirement locations and housing options would fit with shared goals?

Enlisting the aid of a certified financial planner could also make the couple aware of financial options with which they may be unfamiliar and can structure sufficient contingencies and protections into the retirement plan to give both spouses peace of mind.

The husband, whose earnings are larger, might need to delay his retirement to assist in boosting the wife’s retirement account, while she strives to add her contributions to the joint retirement and benefits fund. By working as a team, they can prioritize communication and avoid conflicts in the marriage as they cohesively build towards their retirement goals together.

This article should be considered as opinion only, and not as professional advice. Readers seeking professional retirement plan counseling should contact a Certified Financial Planner or comparable professional.