Key Points from 24/7 Wall St.:

- When you plan to retire early, having a bridge account is important. This account acts as the “bridge” between early retirement and the accessibility of tax-advantaged accounts.

- Striking a balance between these two accounts is important. You don’t want to choose just one or the other.

- Also: Take this quiz to see if you’re on track to retire (Sponsored)

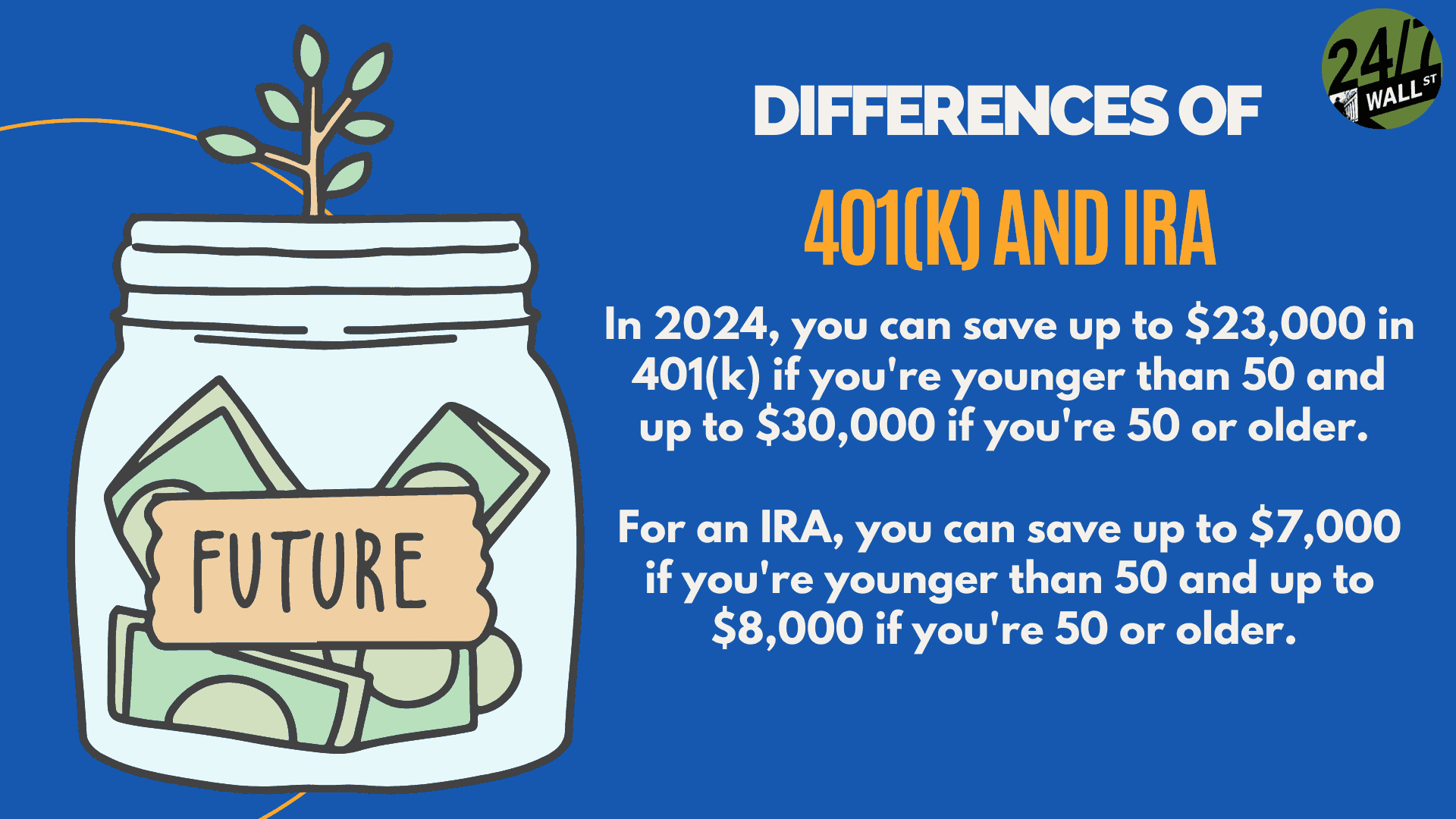

Maxing out retirement accounts refers to contributing the maximum amount allowed by law each year, which can significantly speed up wealth-building and offer greater financial security in retirement. Consistently reaching these thresholds helps take full advantage of tax-deferred or tax-free growth and lessens the risk of outliving your savings. While not everyone has the extra money to max out their contributions, doing so is often seen as the best strategy for those who can afford it. These funds compound over decades, reducing reliance on Social Security or other income sources later in life.

While scrolling through Reddit, I recently came across a post where the user shared a key challenge many in the early retirement community face: balancing contributions to tax-advantaged retirement accounts with building accessible funds for early retirement.

Many in the FIRE community max out their IRA annually, which helps them reach their retirement goal. Low-cost index funds help these accounts grow steadily.

However, this poster was wondering whether they should be prioritizing these tax-advantaged accounts or instead focus on increasing their access to cash. There are pros and cons of each approach.

This post was updated on November 28, 2025 to provide a brief overview of maxing out retirement accounts and how to financial community tends to promote doing so, as well as include a segment on Roth Conversion Ladders.

Here’s my analysis of this dilemma and the key takeaways for anyone in a similar position. Remember, this is just my opinion and not financial advice.

Tax-Advantaged Accounts vs. Bridge Funds

Neither approach is obviously better than the other. Tax-advantaged accounts like IRAs and 401(k)s have serious benefits. They let your investments grow tax-free or in a tax-deferred environment. Both of these facts can help you save money for retirement faster. It is possible for a 401(k) to get potentially too big, though.

However, tax-advantaged accounts also have several restrictions. In many cases, pulling from them is challenging until you reach retirement age and fraught with penalties.

This major downside makes having a “bridge fund” a good idea. This fund is a more accessible account that you can draw from tax-free before your tax-advantaged accounts can be drawn from.

Simply put:

Tax-advantaged accounts allow your funds to grow faster, but a bridge fund is often required for early retirement for flexibility.

The Strategic Benefits of Having Both

You don’t need to choose one type of account over another, though. In most cases, early retirees need tax-advantaged funds and a bridge fund. They work together.

Striking a balance between both of these accounts is the challenge.

Generally, it’s recommended that you focus on tax-advantaged accounts. Over time, you can gradually shift to a bridge fund as you get closer to early retirement.

That said, I also recommend directing any “extra cash” (think bonuses and tax refunds) to your bridge fund, assuming you’re maxing out your traditional accounts.

It’s also worth noting that several strategies exist to access retirement funds early without penalties, including Roth conversion ladders, Rule of 55 withdrawals, and structured distributions under IRS Rule 72(t). Understanding these options can change how much a bridge fund is truly needed.

Roth Conversion Ladders

A Roth conversion ladder is an early-retirement strategy that allows you to access retirement funds before age 59½ without paying early withdrawal penalties. It works by slowly converting portions of a traditional IRA or 401(k) into a Roth IRA each year, paying regular income taxes on the converted amount during the year of the conversion.

After a five-year waiting period for each converted amount, those funds can be withdrawn from the Roth IRA tax- and penalty-free! This money can create a steady stream of accessible income.

When to Shift to a Bridge Fund

So, when should you shift to a bridge fund? In most cases, that depends on how soon you’re considering retirement. If retirement is within 5-10 years, you may want to reduce your IRA contributions and put more toward your bridge fund.

When you’re decades from retirement, it often makes more sense to focus on tax-advantaged accounts to maximize the growth of your funds. As you get closer, the amount of growth you can expect lowers.

Adapt

That said, the most important part of any retirement plan is adapting the plan to your specific situation. Life changes, like increased income, are good opportunities to take a look at your current plan and shift things around as needed.

If you suddenly have extra cash, consider using it to kickstart your bridge fund. Your goal should be to take full advantage of tax-advantaged plans and fund your bridge.