Retirement is a long-term goal that often requires multiple decades of planning. You have to save money, invest it, and calculate how much you’ll spend each month when you retire.

There are plenty of moving pieces that influence your ability to retire, but a few questions can help you gauge if you are on the right track. Asking yourself these three questions can unveil your retirement progress and help you craft a strategy.

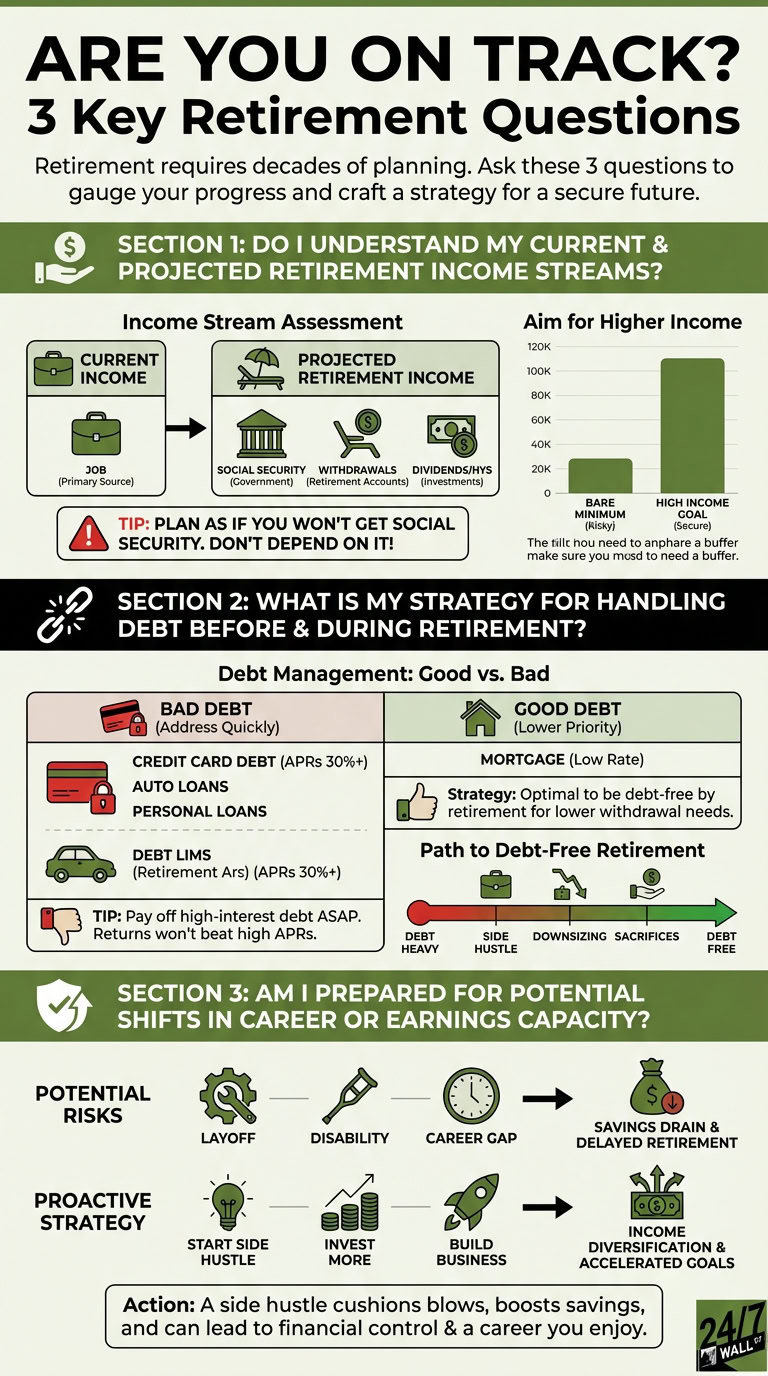

Do I Understand My Current and Projected Retirement Income Streams?

The first step is to assess your income streams. The biggest income stream most people have is that job. However, their income streams will look different in retirement. While you will receive Social Security, it’s best to plan your retirement as if you won’t get Social Security. That way, you aren’t depending on the government to subsidize your retirement lifestyle.

You will have to make withdrawals from your retirement accounts when you walk away from your career. It’s also possible to boost your cash flow with dividend stocks and a high-yield savings account.

Knowing what resources you will use at retirement can help you estimate how much money you need. It’s better to aim for a high income number than it is to retire once you have the bare minimum.

What Is My Strategy for Handling Debt Before and During Retirement?

You are likely to encounter debt on the path to retirement. It’s common for people to take out mortgages to buy properties. You may also need to take out an auto loan or a personal loan. Many people also end up in credit card debt.

The quicker you address bad debt, the easier it is to build wealth. While you shouldn’t rush to pay off a mortgage if you got it at a low rate, credit card debt is always bad. Some cards have APRs above 30%, and you’re unlikely to produce that type of return in the stock market.

It may require picking up a side hustle, downsizing, or making other short-term sacrifices to pay off debt. The more progress you make now, the more smooth your retirement will be.

Some people don’t pay off their mortgage before retiring, but this strategy works better if you are near the end of your mortgage. If you can, it’s optimal to continue working until all of your debt is paid. Then, you can use a lower withdrawal rate to fund your lifestyle.

Am I Prepared for Any Potential Shift in My Career or Earnings Capacity?

Although it’s good to assume you continue to earn at your current level, some people get laid off or end up with a physical disability that inhibits their ability to work. Individuals should consider how their retirement plans would shift if they couldn’t find work for a year. They would have to tap into their savings for that year, which can result in a longer timeframe.

While this thought could lead to fear, it can also inspire action. Picking up a side hustle now will give you more income streams. That way, it’s easier to cushion the blow if you get laid off. In addition, a side hustle allows you to invest more money each month and can get you closer to your long-term goals.

Pursuing a side hustle can even inspire you to start a business that eventually replaces the money you earn at your full-time job. This scenario, when done correctly, can give you much more control over your finances and schedule. You may not want to retire if you have a business or a career that you enjoy.