The stock market is seeing more volatility in August due to the tariff deadlines expiring. The S&P 500 recovered from the spring selloff through April to June, though July saw more of a plateau that could lead to a downturn in August if a tariff war reignites. Still, almost everyone can agree that the U.S. economy has been far more resilient than expected.

Not only did it avoid multiple recessions that were almost guaranteed, but it has also avoided a big spike in inflation from tariffs. Inflation may worsen later on, but the Federal Reserve should still have room to cut in September due to the discrepancy between the interest and inflation rates.

Undervalued dividend stocks are a smart choice right now since they have good upside potential and many are bottoming out in August. Interest rate cuts should start next month and drive up many of them. Plus, investors may also rotate into these stocks if growth stocks start underperforming again.

Here are the three dividend stocks to look into:

Campbell’s Co (CPB)

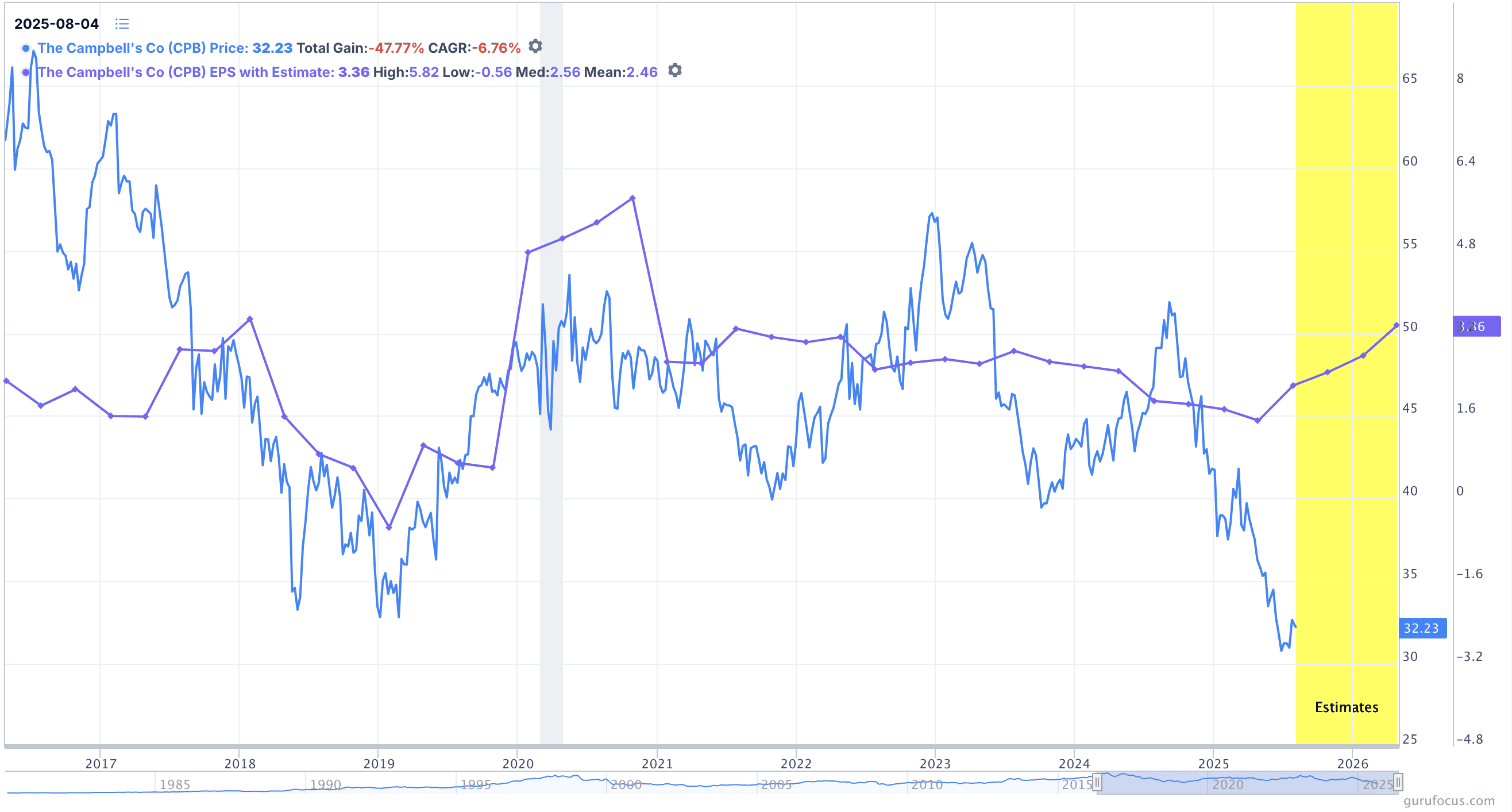

Campbell’s Co (NASDAQ:CPB | CPB Price Prediction) is a branded food and beverage company. It focuses on soups, meals, and snacks. CPB stock is down 35.3% in the past five years as the company struggled with persistent volume declines and stagnation. Inflation and the underperformance in the snacks department caused revenues to slump. Moreover, debt servicing costs rose due to the rate hikes.

A turnaround could be on the horizon as sales stabilize and debt servicing costs come down. The company has managed to reduce its debt load from $7.92 billion at its peak to $6.89 billion in the most recent quarter. It reported $66 million in net income despite posting $80 million in net interest losses. Interest rate cuts should help reduce this burden tremendously.

In Q3 FY 2025, net sales increased 4% to $2.5 billion, though adjusted EPS fell 3% to $0.73. Analysts see earnings recovering soon as tailwinds outweigh the headwinds.

Accordingly, if earnings improve as expected, it could lead to CPB stock making a comeback. In the meantime, you can sit on its 4.84% dividend yield.

Clorox Co (CLX)

Clorox (NYSE:CLX) is a household name that has historically generated solid gains but hasn’t done quite well in recent years. CLX stock is down 47.6% over the past five years as it corrects from the inflated prices of 2021. Right now, it is trading at 2016 prices, and a reversal may be due.

In Q2 2025, revenue rose 4.47% to $1.99 billion and beat estimates by 3.21%. EPS also rebounded significantly by 54.91% and beat estimates by 29.75%.

Analysts expect one more fiscal year of financial deterioration before it finally starts recovering in FY 2027 onwards. Rate cuts will boost the recovery even more.

CLX stock trades at just 19 times earnings today. If you take out one-time items, that PE ratio drops to 16.5. Historically, CLX stock has traded at over 26 times earnings. The decline in CLX stock is warranted due to its recent perils, but I’d expect this household name to eventually bounce back.

It comes with a 3.99% dividend yield. Dividends have been increased for 48 consecutive years.

PepsiCo (PEP)

PepsiCo (NASDAQ:PEP) is one of the biggest victims of the decline snacking stocks have faced since GLP-1 drugs like Ozempic gained popularity. However, PepsiCo has been quite resilient, since the problem is with its margins, not sales.

The company has held onto its revenue, and when the environment is favorable again, it can start raising prices accordingly. I’d buy the dip before that happens.

Revenue increased 1% to $22.73 billion in Q2. Adjusted core EPS beat analyst estimates by 4.43% and reached $2.12. It’s a mainstay of the snacking industry and should eventually make a solid comeback once the storm clears.

Analysts see one more year of EPS decline for all of 2025, with EPS estimated at $8.01, down 1.81% year-over-year. After that, EPS is expected to rebound by 5.62% and build on that momentum.

PEP stock pays you a 4.07% dividend yield with 54 years of consecutive hikes. It’ll get very attractive once interest rate cuts push Treasury yields lower than 4%.