Live: JOBY Earnings Tonight- Can It Stay Hot?

Key Points

-

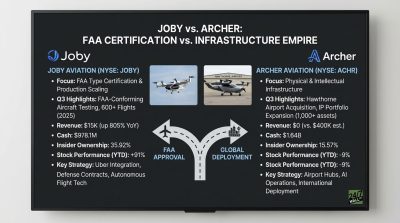

FAA flight testing now 62% complete; full certification remains targeted for 2025.

-

Commercial service in Dubai expected to launch in early 2026.

-

Manufacturing and government partnership updates will be closely watched.

Live Updates

Final Reaction

After a drastic drop immediatly after earnings, JOBY has been gaining momentum and only down 3.12% now. However, the quarter didn’t inspire any confidence for a stock that has been soaring over the past year.

| Period | EPS Estimate | EPS Actual | Revenue Estimate | Revenue Actual |

|---|---|---|---|---|

| Q2 25 | –$0.20 | –$0.41 ❌ | $59.6K | $15K ❌ |

-

🔻 Sentiment: Weak — stock repriced post-rally as cash burn and timelines came into focus

-

🧭 Focus Ahead: FAA TIA in 2025, Blade close, U.S. DoD demos in H2

-

📆 Next Catalyst: Final certification phase + first delivery to Dubai

What Changed This Quarter

-

EPS miss due to non-cash losses: $40.3M in stock issuance, $126M warrant revaluation

-

Adj. EBITDA loss widened to –$131.6M (vs. –$107.2M YoY)

-

Dubai air taxi campaign completed with real-world aircraft

-

First FAA-conforming aircraft assembled — key 2025 target

-

Blade acquisition adds launchpad for 2026 urban ops

-

L3Harris program deepens military dual-use narrative

Milestone & Strategy Update

Execution was strong, but JOBY remains valuation-sensitive given no near-term revenue lift or commercial flight date.

| Area | Q2 2025 Status |

|---|---|

| FAA Certification | 70% complete (Joby side), 53% FAA side |

| Dubai Launch Prep | 21 full-transition test flights completed |

| Aircraft Production | First FAA-conforming aircraft assembled |

| Blade Acquisition | Signed deal for NY & Europe ops |

| Defense (L3Harris) | Hybrid-electric aircraft program launched |

| Cash Balance | $991M |

Guidance/ Updates

No formal financial guidance — business remains in pre-revenue milestone phase

This quarter showcased operational progress — FAA cert, Dubai test flights, defense contracts — but investors wanted more tangible revenue clarity. With EPS missing by a wide margin and no material new commercial deals announced, JOBY’s red-hot YTD rally ran out of fuel post-print.

“Regulatory progress is unlocking global access. Our commercialization strategy is unfolding, and we’re scaling production to meet real demand.”

— JoeBen Bevirt, CEO

The team emphasized production ramp (Marina/Dayton), Blade acquisition, Dubai success, and DoD collaboration — but avoided putting dates on initial passenger service.

Earnings In and Joby Missed the Mark

While Joby hit impressive operational milestones this quarter — including Dubai test flights, FAA certification progress, and the Blade acquisition — the sharp EPS miss and minimal revenue signal continued distance from commercial scale. The market’s reaction reflects fatigue with milestone-only updates amid pre-revenue status.

| Metric | Actual | Estimate | Beat/Miss |

|---|---|---|---|

| EPS | –$0.41 | –$0.20 | ❌ Miss |

| Revenue | $15,000 | $59,600 | ❌ Miss |

Joby Aviation is Down 3% Today

It’s a good day for tech stocks in general; the Nasdaq is up 1.2%. Yet, shares of Joby Aviation are down 3.1%.

It’s worth noting that Archer Aviation is also down about 3.9%, so it might be money moving out of pre-revenue companies in the space. We’ll see if the drop today is just a blip or something concerning before the company announces earnings tonight.

How JOBY Performed After Past Quarters

JOBY has missed EPS estimates in all four prior quarters, but price reaction has generally been positive. The stock tends to move on regulatory and milestone updates rather than financials.

| Quarter | EPS Surprise | 1-Day Move | 7-Day Move | 14-Day Move |

|---|---|---|---|---|

| Q1 2025 | –7.05% | +3.58% | +15.11% | +32.71% |

| Q4 2024 | –0.76% | +0.75% | –1.19% | –3.13% |

| Q3 2024 | –10.32% | +0.59% | +13.02% | +57.79% |

| Q2 2024 | –1.46% | +5.91% | +4.89% | +0.61% |

Joby Aviation (NYSE: JOBY | JOBY Price Prediction) will report Q2 results after the close. With just $59,600 in projected revenue and a $0.20 per-share loss expected, the financials remain secondary to operational progress. Investors are focused on FAA certification milestones, commercial launch prep in Dubai, and updates on strategic partnerships with the U.S. military and U.K. government.

JOBY has been one of the top stocks in the first half of 2025, up 142% year-to-date, but investors should be worried the stock has been overheated heading into Q2 earnings release.

We’ll be updating this live blog with news and analysis right after Joby Aviation’s earnings hit the newswires. To receive updates, all you have to do is leave this page open, and updates will post automatically.

What to Expect

- Revenue: $59.6 thousand

- EPS (Normalized): –$0.20

- FY 2025 Revenue: $1.46 million

- FY 2025 EPS: –$0.63

Consensus implies a 900% YoY increase in full-year revenue off a small base.

Key Areas to Watch

FAA Type Certification and TIA testing

Joby reiterated that it is “now 62% of the way through the FAA certification process” with its third aircraft now in flight testing. TIA (Test Inspection Authorization) remains on track over the next 12 months.

Dubai air taxi launch and regulatory progress

CEO JoeBen Bevirt confirmed that Joby will ship the first production aircraft to Dubai in Q3 ahead of an “early 2026” launch. The team has worked closely with Dubai’s GCAA to align certification timelines.

Manufacturing capacity and U.S. expansion

Joby is scaling production at its Marina, California facility and ramping up hiring at its Dayton, Ohio manufacturing site. Aircraft #4 and #5 are expected to begin production this quarter.

U.S. DoD and U.K. military programs

Joby completed its first multi-aircraft delivery to the U.S. Air Force in Q1 and expanded its Joint Test Plan with the DoD. The company was also selected as a preferred supplier for the U.K. Ministry of Defence’s Future Flight program.

Sales strategy and Virgin Atlantic partnership

CFO Matt Field said the company is “exploring multiple revenue pathways,” including direct-to-consumer, partnerships, and government contracts. The Virgin Atlantic partnership remains in development for future U.K. deployment.

Joel South covers large-cap stocks, dividend investing, and major market trends, with a focus on earnings analysis, valuation, and turning complex data into actionable insights for investors.

He brings more than 15 years of experience as an investor and financial journalist, including 12 years at The Motley Fool, where he served as an investment analyst, Bureau Chief, and later led the Fool.com investing news desk. He has also co-hosted an investing podcast and appeared across TV and radio discussing market trends.

© 24/7 Wall Street