Joby Aviation (NYSE: JOBY | JOBY Price Prediction) and Archer Aviation (NYSE: ACHR) reported Q3 earnings revealing two electric air taxi makers pursuing certification through different paths. Joby focused on FAA milestones and production scaling. Archer bought an airport and expanded its patent portfolio.

Certification vs. Infrastructure: How Each Quarter Landed

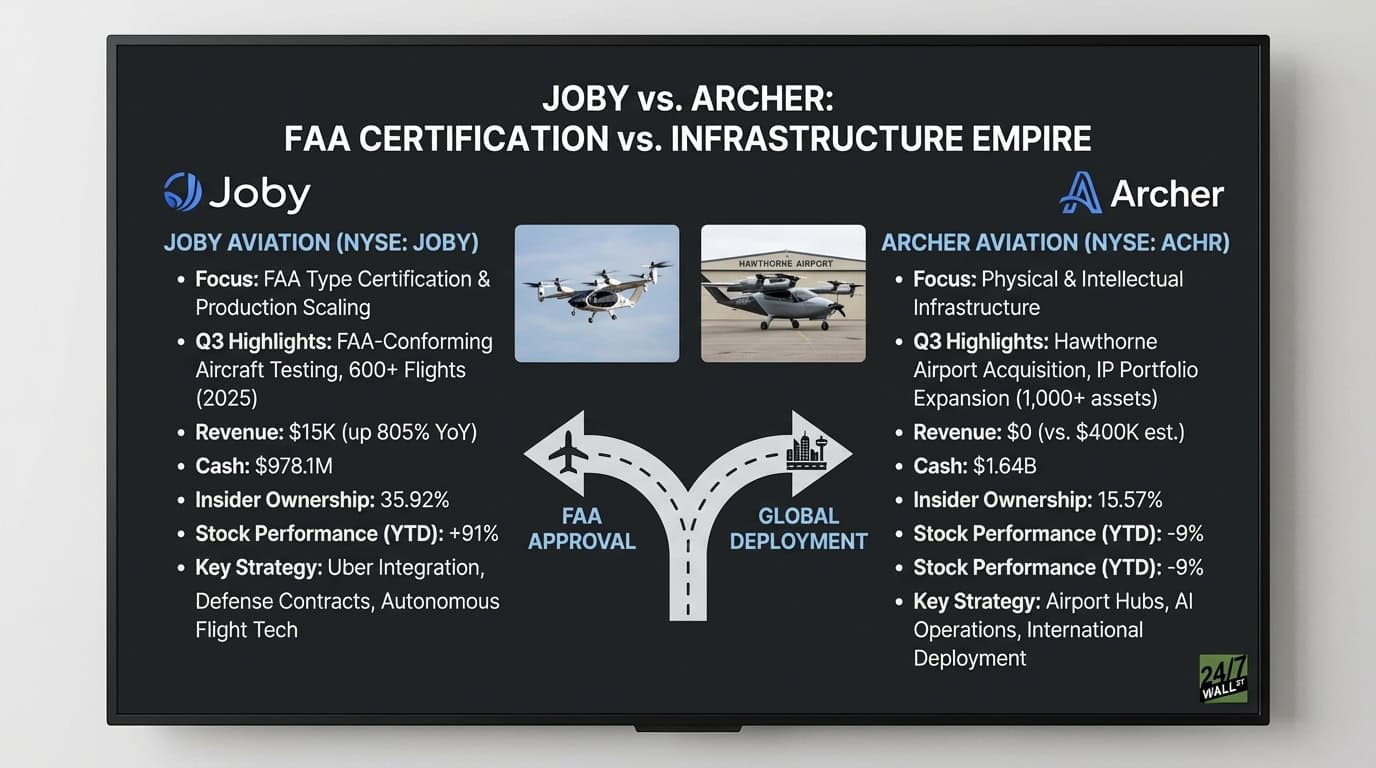

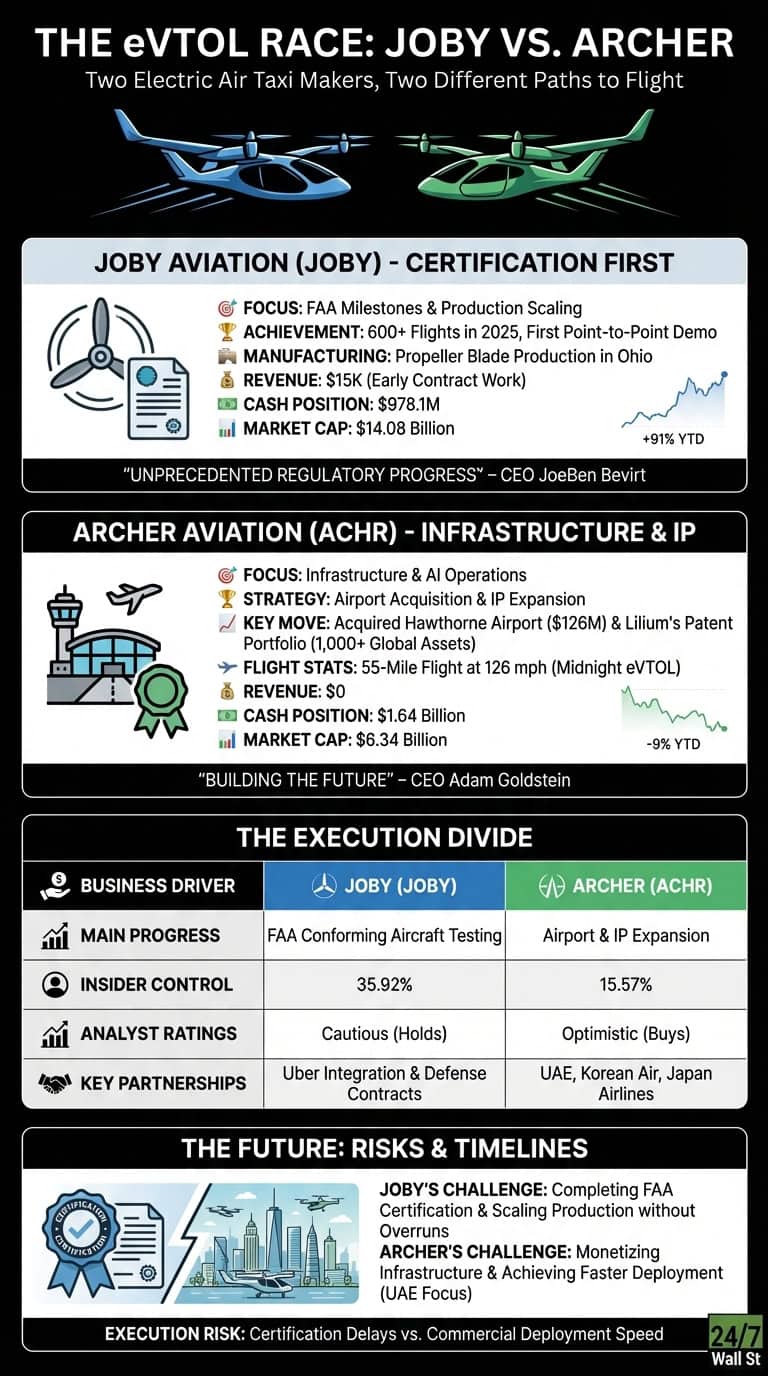

Joby began power-on testing of its FAA-conforming aircraft and completed over 600 flights in 2025, including its first point-to-point demonstration. CEO JoeBen Bevirt called the regulatory progress “unprecedented.” The company started manufacturing propeller blades in Ohio while adding 100+ production roles. Revenue hit $15,000, beating the $12,600 estimate, though this represents early contract work rather than commercial operations. Net loss reached $324.7 million with cash at $978.1 million following a $576 million equity raise.

Archer achieved a 55-mile flight at 126 mph and reached 10,000 feet altitude with its Midnight eVTOL. The company acquired Hawthorne Airport in Los Angeles for $126 million to serve as a strategic hub and AI testbed. It also bought Lilium’s patent portfolio, expanding to over 1,000 global IP assets. Revenue came in at zero versus a $400,000 estimate, with a net loss of $129.9 million. Cash stood at $1.64 billion after a $650 million raise. CEO Adam Goldstein said the company is “building” the future rather than waiting for it.

| Business Driver | Joby | Archer |

| Main Progress | FAA conforming aircraft testing | Airport acquisition, IP expansion |

| Revenue | $15K (up 805% YoY) | $0 (vs $400K est.) |

| Cash Position | $978M | $1.64B |

| Management Focus | Type Certification, production | Infrastructure, AI operations |

One Chases Approval. The Other Builds an Empire.

Joby is executing a certification-first playbook. The company integrated deeper with Uber through expanded Blade services and pursued defense contracts focused on autonomous flight technology, including its Superpilot system with over 7,000 miles logged. Insiders control 35.92% of shares, more than double Archer’s 15.57%. The stock gained 91% year-to-date.

Archer is building physical and intellectual infrastructure before commercial launch. The Hawthorne Airport purchase positions the company to control ground operations and test AI-powered logistics. Partnerships with UAE operators, Korean Air, and Japan Airlines emphasize international deployment over domestic regulatory sprints. Heavy insider selling followed RSU vesting in mid-November, with executives including the CTO and Chief Legal Officer offloading shares at $7.49. The stock is down 9% in 2025.

Which Path Holds Up Through Certification Delays?

Joby’s next test is completing FAA Type Certification while scaling propeller production without cost overruns. Defense contract progress and autonomous flight demonstrations will clarify whether the technology can monetize beyond air taxis. Archer needs to show that owning airports and patents translates into faster commercial deployment, particularly in the UAE where it’s pursuing certification ahead of U.S. approval.

Joby trades at $15.46 with a $14.08 billion market cap. Archer sits at $8.67 with a $6.34 billion valuation. Analysts rate Joby cautiously with six Hold ratings and two Sells, while Archer holds six Buy or Strong Buy ratings with zero Sells.

Key Differences in Execution Risk and Timeline

Joby’s FAA testing progress and 35.92% insider ownership reflect management’s confidence in the certification timeline. Archer’s infrastructure strategy and lower valuation come with higher execution risk given zero revenue and recent insider selling. The UAE certification timeline versus FAA approval will be a key factor in determining which strategy proves more effective.