Shares of Microsoft (NASDAQ:MSFT | MSFT Price Prediction) gained 7.57% over the past five trading sessions after losing 4.87% the five prior. That brings MSFT’s one-year gain to just 7.70%, including a loss of more than 11% since its all-time high on Oct. 28, 2025.

When the Magnificent Seven member reported Q2 earnings on Wednesday, Jan. 28, shares fell around 7% in after-hours trading despite beating Wall Street estimates for earnings and revenue. The company announced that cloud revenue topped $51.5 billion for the first time, while EPS and revenue came in at $5.16 and $81.27 billion, respectively.

On Oct. 1, 2025, the company announced that it was increasing its Xbox Game Pass subscription by 50%. In its last fiscal year, Microsoft saw more than 8% of revenue derived from its gaming segment, which now boasts 50 million monthly active subscribers and nearly $5 billion in YoY revenue.

Microsoft’s decision in May fire 6,000 employees — or 3% of its workforce — signals the tech giant is serious about cost discipline amid economic uncertainty. With analysts eyeing sustained cloud demand, 24/7 Wall St. conducted analysis to explore whether Microsoft can maintain its upward trajectory and drive long-term growth.

Why Invest in Microsoft

Microsoft navigates challenges, but remains a prime investment due to its AI and cloud dominance. Third-quarter earnings showcased robust demand for its Intelligent Cloud segment, though tariff risks linger. Microsoft’s $80 billion cash reserve fuels its $80 billion investments in cloud and AI infrastructure, with over half in the U.S.

Its Microsoft 365 Copilot, adopted by over 70% of Fortune 500 firms, drives productivity revenue, positioning Microsoft to capture the AI market’s 37% compounded annual growth predicted through 2030. Similarly, partnerships with Oracle (NYSE:ORCL) for multi-cloud solutions bolster its competitiveness against Amazon‘s (NASDAQ:AMZN) AWS.

In June 2025, it was reported that the company will be expanding its AI and cloud investments in Switzerland, committing $400 million to expand its data center infrastructure in the European nation. The additional capacity is expected to support more than 50,000 current customers and expand the availability of AI services for more sectors, including health care, finance government. Microsoft is capitalizing on its Azure platform’s momentum as revenue jumped 39% in FY25 Q4, driven by AI services.

When Microsoft last reported earnings, the EPS beat marked the 16th time in the past 17 quarters that the company surpassed estimates.

Microsoft (MSFT) as a Company

Tariff uncertainties do pose risks, even with the pause on China, as supply chain cost pressures for server hardware are not eliminated. Microsoft’s operating income of $32 billion was tempered by a 5% rise in operating expenses, reflecting heavy AI R&D investments. Despite no revenue from its $13 billion OpenAI stake, Microsoft reported $42.4 billion in Microsoft Cloud revenue, up 20% year-over-year.

Beyond cloud, Microsoft’s gaming segment grew 44% with 43 points of the gain coming from its acquisition of Activision, but bolstered by Xbox content and Bethesda’s Starfield expansion. A partnership with Oracle for multicloud solutions strengthens its enterprise offerings, further diversifying its revenue. Wall Street projects Q4 revenue of $73.8 billion, up 14%, driven by Microsoft’s AI and cloud momentum.

Microsoft as a Stock

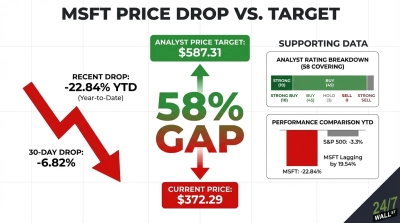

Broadly, 34 Wall Street analysts’ remain bullish, with 32 analysts covering MSFT assigning it a “Buy” rating, two assigning it a “Hold” rating and none assigning it a “Sell” rating. Overall, the stock receives a consensus “Strong Buy” rating. Wall Street’s price targets cover a significant range, spanning $500 per share on the low end to $678 per share on the high end. The median one-year price target for MSFT is $628.98, which represents 41.62% potential upside from today’s share price.

Institutional ownership currently stands at 73.14%, with three of the four largest buy-side firms — Vanguard, BlackRock and State Street — holding a collective 1.570 billion shares of Microsoft.

|

Estimate |

Price Target |

%Change From Current Price |

|

Low |

$450 |

-6.56% |

|

Median |

$618.85 |

28.49% |

|

High |

$678 |

40.77% |

Microsoft (MSFT) Stock Prediction in 2026

Microsoft’s strong Azure revenue growth positions it for cloud and AI market gains. However, $20 billion quarterly capex and tariff risks require caution. Its $80 billion cash reserve and Oracle partnership offer stability, making MSFT stock a buy for growth investors, even as valuation concerns linger.

24/7 Wall St.’s year-end price target for Microsoft in 2026 is $676.36, implying upside potential of 40.43% from the stock’s current price. This cautious target reflects Azure’s strength and FY26 Q1 revenue guidance, balanced against the need for higher capex spending and potential supply chain disruptions, positioning it at a realistic estimate of its leading presence in the space.