United Parcel Service (NYSE: UPS | UPS Price Prediction) shares closed Friday at $96.42, but the real story isn’t the recovery. It’s the stunning collapse in retail investor sentiment following the company’s earnings beat and announcement of 48,000 job cuts.

Social sentiment on UPS has fallen by more than half in two weeks, with Reddit discussions pivoting sharply from cautious optimism to outright skepticism about the quality of the company’s results.

The Earnings Beat That Backfired

UPS delivered impressive headline numbers on October 28. Non-GAAP EPS of $1.74 beat estimates of $1.31 by 33 percent. Revenue of $21.40 billion exceeded expectations of $21.04 billion. Operating profit hit $1.80 billion, adjusted. By any traditional measure, the company crushed expectations. Yet within hours, that narrative evaporated.

The problem wasn’t the earnings; it was the job cuts. The company announced it would eliminate 48,000 positions in management and operations. This represents roughly 6.5% of its total workforce. CEO Carol Tomé framed it as “executing the most significant strategic shift in our company’s history,” but retail investors read it differently. They saw cost-cutting masquerading as operational excellence. They saw a company contracting, not growing.

The underlying fundamentals reinforced those concerns. UPS reported earnings down 14.1% and year-over-year and revenue down 3.7%. The U.S. domestic segment, the company’s core business, declined 2.6% on lower volume. Supply Chain Solutions revenue plummeted 22.1% due to divestitures. This wasn’t a company firing on all cylinders. This was a company under pressure, cutting aggressively to defend margins.

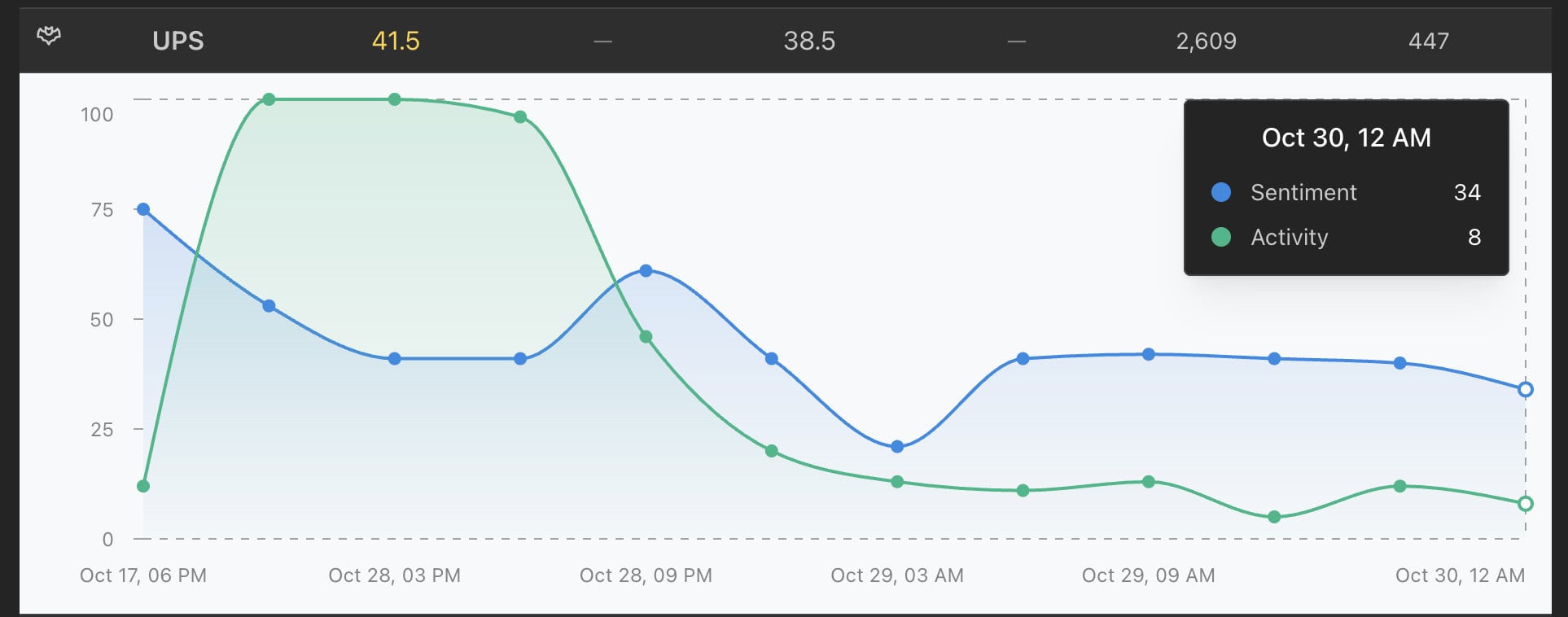

Reddit Sentiment Crashes on Job Cuts Reality

Sentiment tracking shows the dramatic shift. Two weeks ago UPS was riding high with a sentiment of 75/100. It fell a little, then popped back to 70 heading into earnings.

But then the bottom fell out as investors digested the news, getting as low as 24/100. They have since settled back to 34/100 today, but that’s still down 60% from just two weeks ago.

A post on r/stocks titled “UPS Cuts 48,000 Jobs in Management and Operations” accumulated over 2,300 upvotes, dominating discussions across Reddit. The thread generated sustained engagement and consistently negative commentary. Retail investors weren’t celebrating the earnings beat. They were questioning what it meant that UPS needed to slash nearly 50,000 jobs to achieve it. Here’s what drove the pessimism:

- Revenue is contracting year-over-year, signaling weakening demand and a battered US consumer

- Amazon’s volume with UPS fell 21.2%

- The company’s operating margin stands at just 8.64 percent, compressed by pricing pressure

- These job cuts feel like retrenchment, not offense

Stock Gives Back Gains as Institutional Reality Sets In

The disconnect between the earnings beat and investor reaction reveals something crucial. When a company beats estimates primarily through cost-cutting rather than revenue growth, markets eventually recognize it as a sign of structural weakness, not operational excellence. UPS delivered the numbers, but retail investors on Reddit saw the subtext. The company is contracting, not expanding. And no earnings beat changes that narrative.