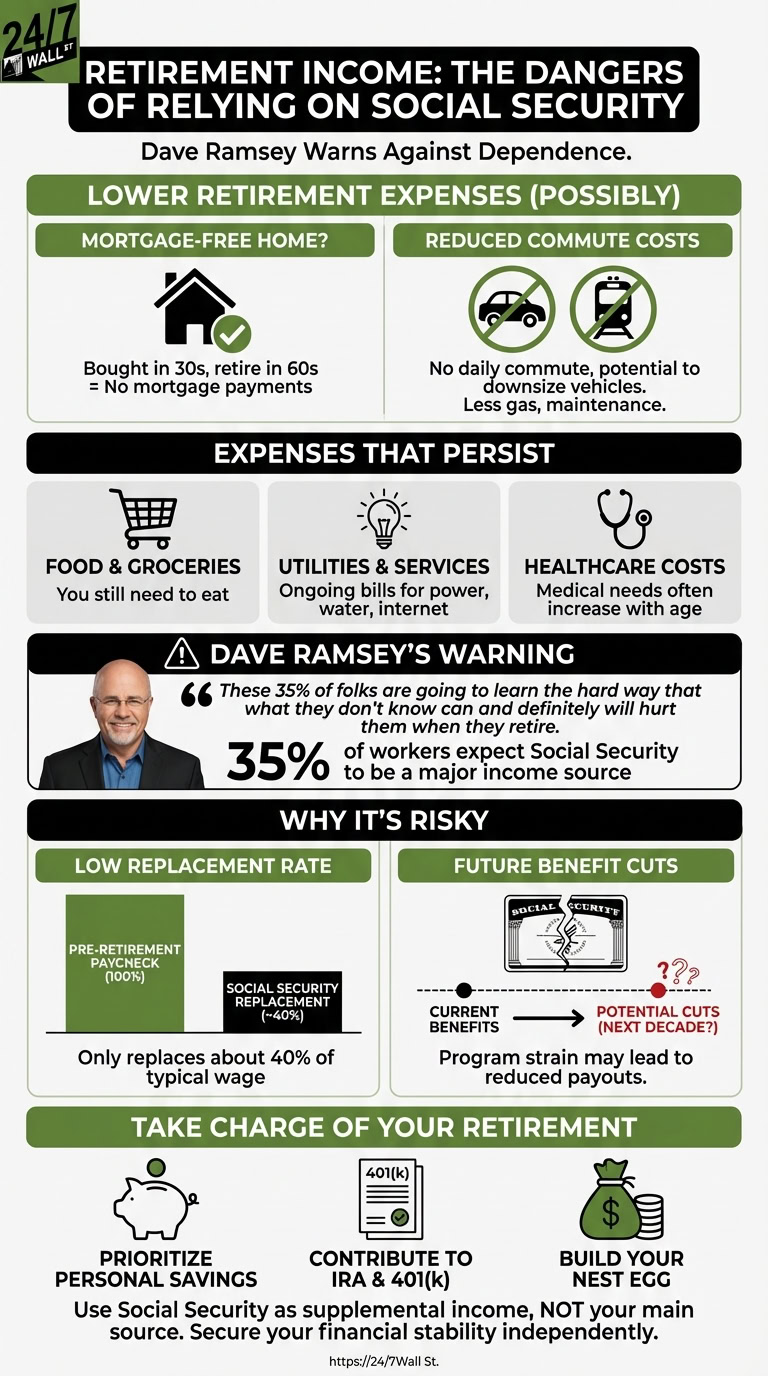

When you retire, you may end up needing less income than what you need during your working years. The reason is because a number of your expenses may be lower.

If you bought your home in your 30s and retire in your 60s, you may no longer have a mortgage by the time your career comes to an end. Not having to make those monthly payments could free up a lot of room in your budget.

Similarly, if you’re used to spending $200 a month to commute to a job, once you’re retired, you won’t have to bear that expense. And you may find that you’re able to downsize from a two-vehicle household to a single vehicle if you and your spouse no longer have jobs to go to, saving yourselves money as retirees.

Still, there’s only so much of a pay cut you can afford in retirement, as many of the expenses you face during your working years will still be in play. You’ll still need to buy food, pay for utility services, and cover the cost of healthcare.

That’s why planning to rely heavily on Social Security in retirement may not be such a smart move. While it’s okay to incorporate those benefits into your retirement income plans, depending on them as a major source of income could come back to bite you.

Dave Ramsey cautions on Social Security dependence

Dave Ramsey is a big advocate of financial security. For this reason, he’s motivated to help people avoid making mistakes that could derail them in retirement.

Recently, Ramsey quoted a survey by the Employee Benefit Research Institute, which found that 35% of today’s workers expect Social Security to be a major source of income for them during retirement. But Ramsey said, “These 35% of folks are going to learn the hard way that what they don’t know can and definitely will hurt them when they retire.”

Ramsey insists that relying too heavily on Social Security for retirement income is a dangerous move. And he’s right for a couple of reasons.

First, Social Security will only replace about 40% of your pre-retirement paycheck if you earn a typical wage. Even if you end up with smaller bills in retirement compared to your working years, they may not be 60% smaller.

Secondly, Social Security is facing benefit cuts in the coming years as older workers retire and file claims, putting a strain on the program. Though benefit cuts aren’t set in stone, they could happen in less than a decade if lawmakers do not find a way to address Social Security’s pending financial shortfall.

For these reasons, Ramsey is right to warn workers not to rely too much on Social Security. And it pays to heed his advice.

Take charge of your own retirement

There’s no reason to write off Social Security in the context of your retirement. However, a smart move is to save on your own for retirement so you’re able to cover the bulk of your expenses based on your personal nest egg. From there, use Social Security as supplemental income — not the other way around.

Ramsey insists that people’s financial stability in retirement should not come from Social Security, especially at a time when benefit cuts are possible. So if you want to increase your chances of being able to enjoy retirement without financial worries, be sure to prioritize IRA or 401(k) contributions while you’re working.