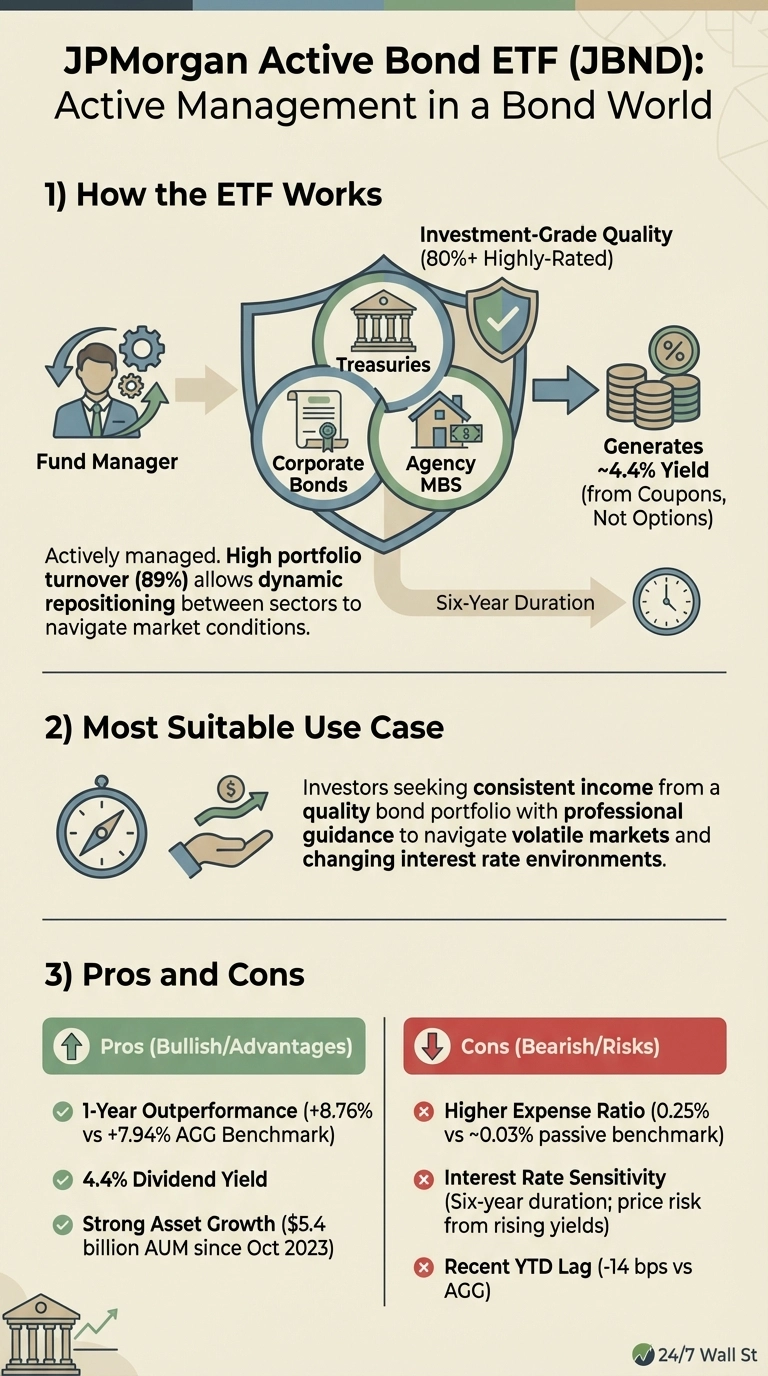

The JPMorgan Active Bond ETF (NYSEARCA:JBND | JBND Price Prediction) charges a premium for active management, but has attracted $5.4 billion since its October 2023 launch by delivering outperformance when markets get volatile. The real test ahead is whether managers can continue generating alpha as corporate bond spreads compress to levels not seen in two decades.

The Spread Squeeze That Could Define 2026

Corporate bond spreads have compressed to their tightest levels in two decades, creating a challenging environment for active managers. This compression matters because JBND allocates roughly 15% to corporate bonds, and Breckinridge Capital Advisors expects modest spread widening ahead as the market normalizes.

JBND’s 89% portfolio turnover rate signals aggressive repositioning by managers navigating compressed spreads. With bond returns likely coming from coupon income rather than price appreciation, Breckinridge estimates investment grade bonds could deliver around 5% from coupons this year, making active sector selection critical.

Rising Treasury yields pose the primary risk for JBND holders. JPMorgan Chase. (NYSE:JPM)’s 2026 outlook projects 10-year yields could reach 4.35%, and the fund’s six-year duration means price sensitivity to those moves will be significant. How managers position for this rate environment will determine whether the active management premium pays off.

Income Consistency in an Options-Free World

Unlike many popular income ETFs that juice yields through options strategies, JBND generates its 4.4% yield by owning bonds that pay interest. Distribution consistency depends entirely on the fund’s holdings and their coupon payments, not on options premiums or equity volatility.

JBND’s managers favor securitized products for their yield advantage over Treasuries while maintaining investment grade quality. The fund holds roughly 30% in agency mortgage-backed securities and asset-backed securities, which offer income pickup but carry prepayment risk that behaves differently than corporate bonds during stress.

Monitor JBND’s monthly fact sheets on JPMorgan’s website to track how sector allocations shift. The fund’s active mandate means managers can move quickly between sectors, but your exposure today might look different in three months. Pay attention to the corporate bond allocation. If managers are increasing corporate exposure while spreads remain tight, they’re betting on continued economic stability. If they’re trimming corporates in favor of Treasuries, that’s a more defensive posture.

Consider This Alternative

The iShares Flexible Income Active ETF (NYSEARCA:BINC) manages $15.1 billion with broader mandate flexibility at a 0.40% expense ratio. That 70 basis point cost advantage translates directly to BINC’s higher 5.1% yield, which could prove more valuable than active management alpha if bond prices remain range-bound through 2026.

Bottom Line

Watch corporate credit spreads for signs of widening and monitor JBND’s monthly sector allocations to understand how managers are positioning for a year where income, not price appreciation, will likely drive returns.