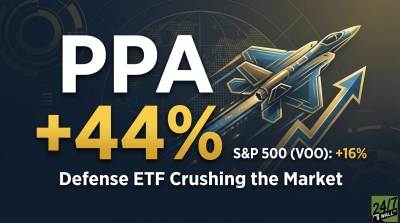

The Themes Transatlantic Defense ETF is riding a surge in defense spending that hasn’t been seen for years, maybe decades. The fund holds a concentrated portfolio of U.S. and European defense contractors, with RTX, GE Aerospace, and Boeing making up nearly a quarter of assets. The ETF is already up 17.5% over the past month as defense budgets expand across NATO countries.

For investors considering NATO or already holding it, the question isn’t whether defense spending will increase. It’s whether the current pace is sustainable and how individual contractors will capture that demand.

The Budget Cycle: When Commitments Turn Into Contracts

The single biggest macro factor for NATO is the timing and magnitude of European defense budget increases. Since Russia’s invasion of Ukraine in early 2022, NATO members have pledged to meet the 2% of GDP defense spending target, with some countries committing to 3% or more. But pledges don’t immediately translate into revenue for defense contractors.

What matters is when those budget increases flow through procurement cycles into actual contracts. Germany announced a €100 billion special defense fund in 2022, but contract awards have been uneven. Poland committed to raising defense spending to 4% of GDP, but the timeline for major platform purchases stretches across years.

Watch for quarterly contract award announcements from NATO governments, particularly for long-cycle programs like fighter jets, missile defense systems, and naval vessels. These typically appear in defense ministry press releases and are compiled by industry publications like Jane’s Defence Weekly. The lag between budget authorization and contract execution can be 12 to 24 months, meaning 2026 may finally reflect commitments made in 2024.

The Lockheed Problem: When Your Holdings Miss Badly

Lockheed Martin, the ETF’s seventh-largest holding at 4.5%, reported a troubling earnings pattern in 2025. The company missed estimates by 77% in Q2 2025, delivering just $1.46 per share against expectations of $6.47. Full-year earnings fell 30% to $15.69, the lowest since 2018.

This matters because it suggests defense contractors may struggle to convert rising budgets into profits due to supply chain constraints, labor shortages, or fixed-price contract structures that don’t adjust for inflation. If Lockheed’s issues spread to other holdings like RTX or Northrop Grumman, the ETF’s thesis weakens.

Monitor quarterly earnings releases and guidance revisions from the top 10 holdings. Production delays or margin compression signal structural problems beyond budget growth.

Consider ITA Instead

For a broader, more liquid alternative, the iShares U.S. Aerospace & Defense ETF (ITA) offers similar exposure with $11 billion in assets, a longer track record since 2006, and a 0.40% expense ratio. It’s more diversified and less concentrated in the top three names, reducing single-stock risk.

The key question for the next 12 months: Will European procurement cycles accelerate fast enough to offset execution risk at major contractors?