At 66, losing a spouse forces a complete financial reset. A Reddit user shared her mother-in-law Linda’s situation: newly widowed at 66, living with family, receiving Social Security, and trying to invest $60,000 to $80,000 from her house sale. Another poster described helping his 67-year-old widowed mother navigate $1 million in assets after his father, who handled all finances, passed away. These scenarios highlight a challenging transition: reassessing retirement when the financial landscape suddenly shifts.

Situation Overview

- Age: 66 years old, recently widowed

- Primary challenge: Transitioning from joint to individual financial planning

- Income sources: Social Security survivor benefits, potential portfolio withdrawals

- Key decisions: Asset allocation, spending sustainability, tax planning

- Timeline: Required Minimum Distributions begin at age 73

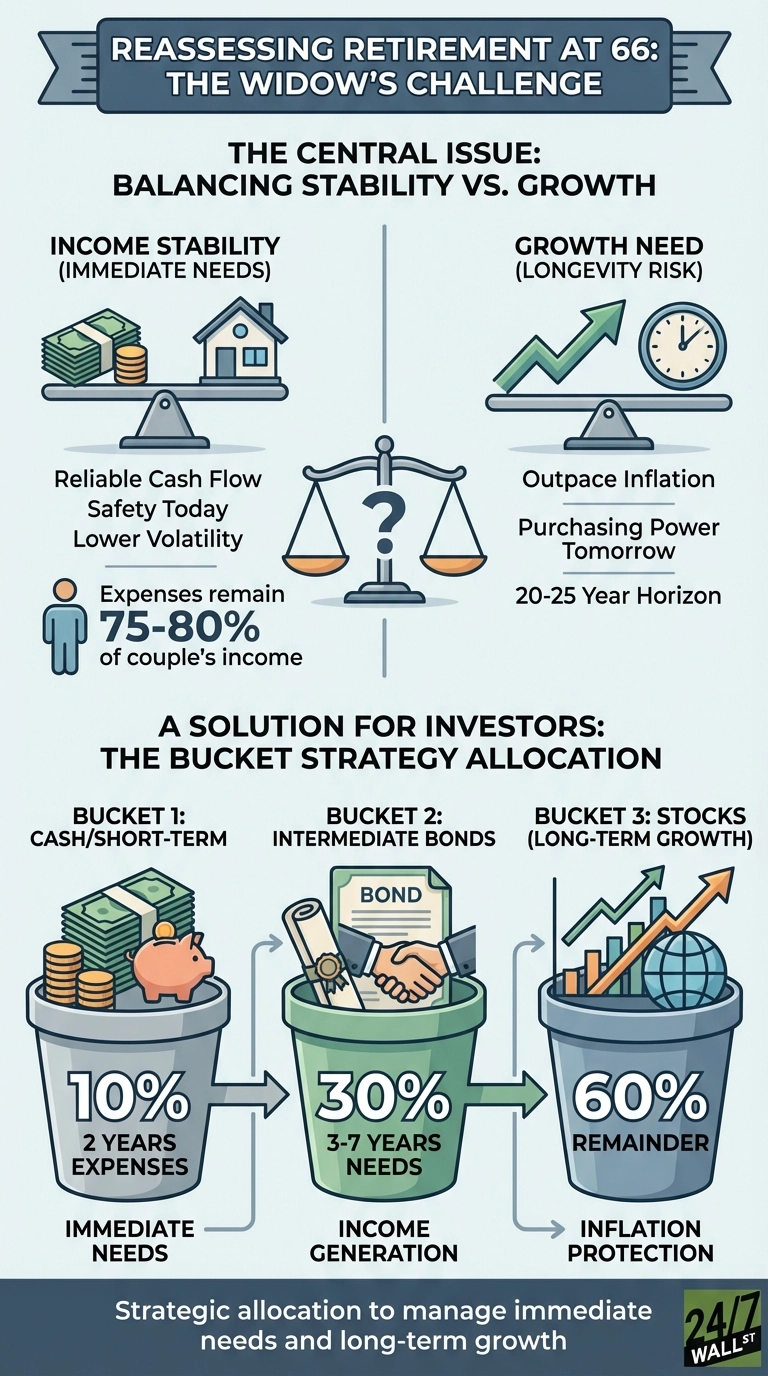

The Core Financial Tension: Income Stability vs. Growth Need

The fundamental challenge centers on balancing immediate income security against longevity risk. With life expectancy potentially extending 20 to 25 years, inflation will erode purchasing power significantly. A woman retiring today at 66 could live into her late 80s or beyond, meaning her portfolio must sustain withdrawals while maintaining growth.

Social Security survivor benefits provide the foundation. A widow receives the higher of her own benefit or 100% of her deceased spouse’s benefit. If she received $2,000 monthly but her husband received $3,200, she now gets $3,200. However, household expenses don’t drop proportionally. Research shows a surviving spouse typically needs 75% to 80% of the couple’s previous income.

Portfolio allocation matters enormously. A conservative 60% bond, 40% stock allocation prioritizes stability but may not outpace inflation over two decades. With long-term Treasury bonds currently yielding around 4.6% (as reflected in TLT’s dividend profile) and stocks returning 14.5% over the past year, the tradeoff is clear: safety today versus purchasing power tomorrow.

Strategic Paths Forward

The most effective approach depends on whether portfolio withdrawals are immediately necessary. When Social Security covers essential expenses, financial advisors often recommend a 60% stock, 40% bond allocation for retirees in this situation, accepting short-term volatility for inflation protection. The Vanguard Balanced Index Fund (VBIAX) exemplifies this approach.

When immediate income is needed, many financial planners use a bucket strategy: two years of expenses in cash or short-term bonds, three to seven years of needs in intermediate bonds, and the remainder allocated to stocks. This prevents forced selling during market downturns like January 2026’s 2% pullback.

Tax planning becomes critical at age 73 when Required Minimum Distributions begin. If the widow has substantial traditional IRA assets, financial advisors often evaluate partial Roth conversions during lower-income years before RMDs start. Converting $20,000 to $30,000 annually at today’s 12% or 22% tax brackets beats paying 24% or higher later when RMDs push income up.

What to Do First

Confirm Social Security survivor benefits are maximized. Verify you’re receiving the higher benefit amount and understand how any personal earnings might affect payments. Second, calculate your true monthly expenses. Many widows discover costs they didn’t previously track. Finally, understand the tradeoffs in different allocation strategies. Financial planners note that bond-heavy portfolios have historically faced inflation erosion over 25-year periods, while stock-heavy portfolios experience higher short-term volatility but have historically provided inflation protection over longer timeframes. Each approach carries distinct risks and benefits depending on individual circumstances.