A dual-income couple approaching retirement with $1.2 million in savings and Social Security benefits faces a critical question: Will this be enough? The answer depends heavily on coordinating Social Security claims and structuring portfolio withdrawals.

The Financial Snapshot

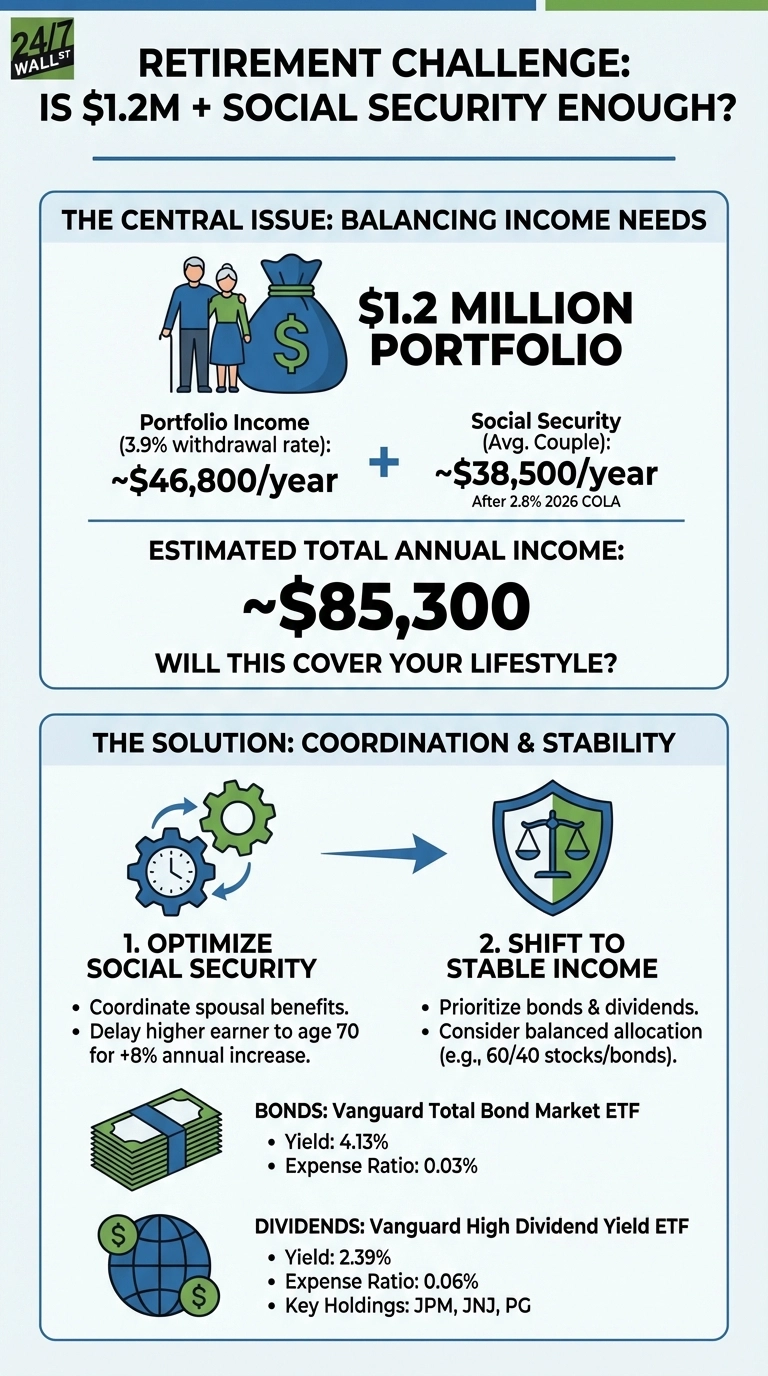

- Portfolio: $1.2 million in retirement savings

- Income source: Social Security benefits from dual earners

- Key challenge: Coordinating spousal benefits with uneven earnings histories

- Critical decision: Withdrawal strategy and claiming timing

The Withdrawal Rate Reality

Morningstar’s 2026 research suggests a 3.9% withdrawal rate for new retirees. Applied to $1.2 million, this generates approximately $46,800 annually, or $3,900 monthly from the portfolio alone.

Social Security adds substantial income for dual-earner couples. The Social Security Administration reports the average aged couple receives approximately $3,208 monthly in 2026, or roughly $38,500 annually after the 2.8% cost-of-living adjustment. Combined with portfolio withdrawals, this creates total annual income around $85,300, or about $7,100 monthly before taxes.

For couples with uneven earnings histories, spousal benefits become crucial. The lower-earning spouse can claim up to 50% of the higher earner’s full retirement age benefit, even if their own work record would produce a smaller payment. This coordination can meaningfully boost household income.

Strategic Paths Worth Considering

The claiming sequence matters enormously. If one spouse earned significantly more, delaying their benefit until age 70 while the lower earner claims earlier can maximize lifetime payouts. Each year of delay past full retirement age increases benefits by 8%, a guaranteed return that’s hard to match elsewhere.

Portfolio allocation should shift toward stability as withdrawals begin. A balanced approach might include 60% stocks for growth and 40% bonds for income and volatility dampening. The Vanguard Total Bond Market ETF currently yields 4.13% with a minimal 0.03% expense ratio, providing tax-efficient fixed income. For equity exposure focused on dividend income, the Vanguard High Dividend Yield ETF offers a 2.39% yield with holdings in established companies like JPMorgan Chase, Johnson & Johnson, and Procter & Gamble.

Tax planning deserves equal attention. Withdrawing from taxable accounts first, then tax-deferred accounts, and finally Roth accounts can minimize lifetime tax bills. For couples with substantial traditional IRA or 401(k) balances, required minimum distributions starting at age 73 will force withdrawals whether needed or not, potentially pushing income into higher brackets.

What to Evaluate First

Request your Social Security statements to understand both spouses’ benefit amounts at different claiming ages. The difference between claiming at 62 versus 70 can exceed 75% for the higher earner. Model several scenarios to see how coordinated claiming affects total household income over 20-30 years.

Calculate your actual spending needs rather than relying on percentage rules. The $7,100 monthly income outlined above works comfortably for couples spending $5,000-$6,000 monthly, but falls short if your lifestyle requires $8,000 or more. Healthcare costs before Medicare eligibility can consume $1,500-$2,000 monthly for couples in their early 60s.

Avoid treating both spouses’ Social Security decisions independently. Your claiming choices interact, especially regarding survivor benefits. When one spouse dies, the surviving partner receives the higher of the two benefits, making it valuable to maximize at least one payment even if it means the lower earner claims earlier for cash flow.