You want to talk about irony? Okta Inc (NASDAQ:OKTA | OKTA Price Prediction) sells identity security to enterprises worldwide, and in 2023, hackers breached its own systems. Twice. That’s like hiring a locksmith who leaves your front door wide open. The question isn’t whether those headlines hurt the stock. They did. The question is whether they’ll haunt it forever.

The Security Incidents: How Bad Were They Really?

Let’s be blunt. When you’re selling zero-trust architecture and your own systems get compromised, customers notice. Okta’s 2023 breaches exposed customer data and eroded trust at exactly the wrong time. Identity security is a confidence game. You’re asking enterprises to hand over the keys to their entire digital kingdom. If you can’t protect yourself, why should they trust you with their employees’ credentials?

The stock got hammered. Over five years, shares are down 66%. That’s not just breach fallout. That’s a fundamental repricing of what this company is worth when trust becomes a liability instead of an asset.

The Profitability Pivot: Execution Over Reputation

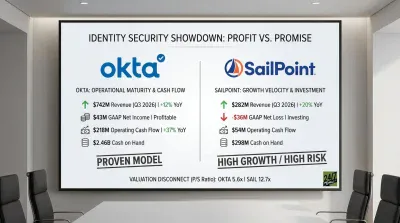

Here’s what the market is starting to notice: Okta is executing. The company just posted its fourth consecutive quarterly earnings beat, with Q3 revenue hitting $742 million and 11.6% growth. More importantly, it swung from chronic losses to profitability in fiscal 2025, with operating margins improving 2,000 basis points year-over-year.

Gross margins expanded to 76.3%, the highest in company history. Management announced a $1 billion share buyback in January 2026, signaling confidence that the stock is undervalued. Analysts at Cantor Fitzgerald see 30% upside, calling it a “contrarian value opportunity.” Jefferies upgraded to Buy with a $125 price target.

But here’s the tension: Okta trades at a forward price-to-earnings ratio of 23x while CrowdStrike (NASDAQ:CRWD) commands 91x despite being unprofitable. CrowdStrike just acquired SGNL, moving aggressively into identity security. That’s Okta’s core market. If CRWD can deliver endpoint security and identity management in one platform, why would customers choose Okta?

Can Trust Be Rebuilt?

The brutal truth is that security companies live and die by reputation. A bank can get robbed and survive if it makes customers whole. But Okta isn’t just selling a product. It’s selling assurance. The breaches didn’t just cost revenue. They cost credibility in a market where credibility is the entire moat.

Customer retention appears solid, but new customer acquisition is the real test. Are enterprises willing to bet their identity infrastructure on a company that failed to protect its own? The stock’s one-year performance is flat, up just 0.5%. That’s not forgiveness. That’s indifference.

Okta’s financial turnaround is real. Revenue growth is steady, margins are expanding, and profitability is sustainable. But the question isn’t whether Okta can operate a profitable business. It’s whether the market will ever price it like a trusted security leader again. Right now, the answer is no. Whether that changes depends on something harder to measure than earnings: whether enterprises believe Okta has earned back the right to be trusted.