Palantir Technologies (NASDAQ:PLTR | PLTR Price Prediction) and CrowdStrike (NASDAQ:CRWD) both beat expectations this quarter, yet represent two different AI bets.

One is an analytics software company growing rapidly with GAAP profits. The other is a cybersecurity platform rebuilding after a damaging 2024 incident. Which AI exposure belongs in a portfolio?

Palantir Runs Hot. CrowdStrike Runs Steady.

Palantir’s fourth quarter 2025 revenue hit $1.4 billion, up 70% year-over-year, powered almost entirely by the Artificial Intelligence Platform. U.S. commercial revenue surged 137% to $507 million, and U.S. government revenue rose 66% to $570 million. The company closed 180 deals at $1 million or more and 61 at $10 million or more in a single quarter, signaling real enterprise conviction rather than pilot fatigue.

| Business Driver | Palantir (Q4 2025) | CrowdStrike (Q4 FY2026) |

|---|---|---|

| Revenue Growth YoY | 70% | 23.3% |

| GAAP Operating Income | $575M (41% margin) | -$6.9M (near breakeven) |

| Free Cash Flow | $791M | $376M |

| Core Growth Metric | Rule of 40: 127% | Net New ARR: $330.7M (+47%) |

CrowdStrike’s story differs. Q4 FY2026 revenue reached $1.3 billion, up 23.3% year-over-year, and ending ARR grew 24% to $5.25 billion. The key metric was net new ARR: $330.7 million in Q4, up 47% year-over-year, and $1.01 billion for the full year, the first time the company has crossed $1 billion in net new ARR in a single fiscal year. Falcon Flex, the flexible consumption model, reached $1.69 billion in ARR, up over 120% year-over-year.

AIP vs. Falcon Flex: Two Expansion Engines

Palantir’s growth runs through AIP, embedding large language model capabilities into enterprise and government workflows. The strategy concentrates on deepening the AI layer and letting deal size expand naturally. Total contract value closed hit $4.26 billion, up 138% year-over-year. That TCV growth suggests long-term customer commitments, not short trials.

CrowdStrike consolidates. Falcon Flex lets customers start with endpoint protection and gradually adopt identity security, cloud workload protection, next-generation SIEM, and AI detection without friction. Half of the customer base now uses six or more modules, 34% use seven or more, and 24% use eight or more.

CrowdStrike also acquired SGNL for identity, Seraphic Security for browser runtime protection, and Pangea for AI security in the past year, widening the platform.

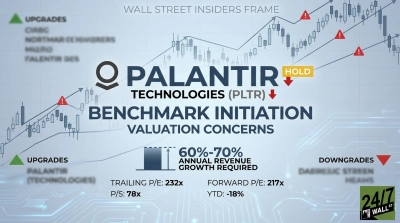

Risk profiles differ. Palantir carries $684 million in stock-based compensation for FY2025 and a trailing P/E of 232x. CrowdStrike still carries the shadow of its July 2024 Falcon sensor incident, which cost $117.7 million in FY2026 charges and contributed to a GAAP operating loss of $293.3 million for the full year.

The Valuation Gap

Palantir’s FY2026 revenue guidance of $7.18 to $7.19 billion implies 61% growth, which is extraordinary. But the stock trades at a forward P/E of 114x and a price-to-sales ratio of 78x.

Even with a Rule of 40 score of 127%, those multiples price in perfection for years. The stock is down 17.64% year-to-date despite the blowout quarter. Analysts target $186.22 on average, but insider activity shows net selling across 69 recent transactions.

CrowdStrike’s forward P/E of 88x is elevated but defensible given its ARR trajectory. Analysts are unified: 42 buy ratings, 14 holds, and zero sells, with a consensus target of $489.86. Insider activity skews toward buying. CrowdStrike is up 8.31% since its March 3 earnings filing, while Palantir is essentially flat over the same period.

Why CrowdStrike Poses Less Portfolio Risk

Both stocks carry real risk. Palantir’s valuation punishes any miss severely, and insider selling deserves attention. CrowdStrike has lingering incident costs and GAAP losses, though both are improving. Watch whether Palantir’s U.S. commercial acceleration continues into Q1 2026, where guidance calls for $1.532 to $1.536 billion in revenue.

For CrowdStrike, the question is whether Falcon Flex keeps pulling customers deeper into the platform and whether the $20 billion ARR target by FY2036 remains credible as competition intensifies.

For a growth-oriented but risk-aware portfolio, CrowdStrike carries lower valuation risk by most conventional metrics. Analyst consensus is cleaner, insider sentiment constructive, and the platform consolidation thesis has structural legs.

Palantir’s growth is remarkable, but at 232x trailing earnings, the margin for error is nearly zero. That setup carries significant downside risk if the AI spending cycle pauses.