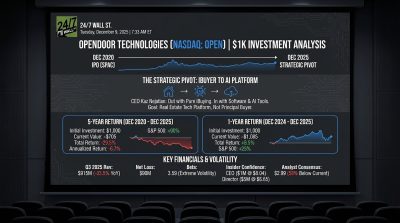

Opendoor Technologies (NASDAQ:OPEN) is up 378% over the past year while retail investors post gambling wins on Reddit and analysts call it a potential 10-bagger. The company burned $595 million in operating cash flow in 2024 and posted a negative 6.7% profit margin. Someone’s math doesn’t add up.

The iBuying Model Already Failed Once

Zillow Group (NASDAQ:Z | Z Price Prediction) tried this exact model and imploded in 2021. The real estate giant accumulated billions in inventory, couldn’t liquidate homes profitably when rates rose, and exited iBuying entirely. Zillow still operates at negative margins despite $2.5 billion in revenue and a $15.7 billion market cap. If a company 10 times Opendoor’s size with an established brand couldn’t make the unit economics work, what makes Opendoor different?

The answer isn’t in the fundamentals. Opendoor’s revenue collapsed 33.6% year-over-year in Q3 2025. The company posted a $90 million net loss that quarter and has burned cash in seven consecutive years. That 378% stock surge? It’s driven by Trump’s proposed $200 billion mortgage bond purchase plan and a single Reddit post celebrating $27,000 in realized gains.

The Cash Flow Illusion

Opendoor’s cash flow statements look schizophrenic because of inventory swings. In 2023, the company reported $2.34 billion in operating cash flow, which sounds impressive until you realize $2.61 billion came from buying homes (inventory buildup). Strip out inventory changes, and core operations burned $269 million. In 2024, operating cash flow went negative $595 million as the company liquidated inventory. Adjusted for inventory, core burn was still $146 million.

This is the iBuying trap. Positive cash flow doesn’t mean profitable operations. It means you’re selling homes faster than you’re buying them. Opendoor’s gross margin sits at 8%, capturing razor-thin spreads on transactions while carrying massive balance sheet risk. One inventory mispricing cycle and the whole model collapses, exactly like Zillow in 2021.

Housing Market Conditions Aren’t Helping

Prediction markets tell a sobering story about 2026 housing. In San Francisco, 51% of traders expect median home values below $1.06 million, pricing in potential declines. NYC markets show 92% conviction for prices in the tight $570,000-$590,000 range, offering minimal margin for error. Only Miami shows strong appreciation expectations above $1.1 million. Opendoor’s success depends heavily on geographic mix and timing, not a uniform housing tailwind.

D.R. Horton (NYSE:DHI), the largest U.S. homebuilder, is up just 11% over the past year despite being profitable. If traditional homebuilders with proven business models are barely moving, why is an unprofitable iBuyer up 378%?

The Verdict: Show Me the Unit Economics

Analyst consensus tells you everything: the average price target is $3.77, representing 42% downside from current levels. Five of nine analysts rate it Hold, with no Buy ratings. The forward P/E of 40x assumes profitability that hasn’t materialized in seven years.

Could Opendoor become a 10-bagger? Sure, if they crack profitable unit economics, rates fall dramatically, and housing inventory loosens. But that’s a lot of ifs for a company that’s already disappointed multiple times. The stock’s 3.65 beta means it swings 3.6 times harder than the market. Right now, that volatility is pricing in hope, not fundamentals. Until Opendoor shows it can make money buying and selling homes, this looks like the same old iBuying dream with better PR.