If the Federal Reserve starts cutting rates in 2026, a specific category of stocks could see their valuations expand like a compressed spring finally released. Lower borrowing costs don’t just make debt cheaper; they make future cash flows more valuable, dividend yields more attractive relative to bonds, and growth stories more credible. Here’s how two rate-sensitive stocks might respond based on their financial structures and what analysts expect to see if rates drop this year.

First: Will Rates Drop in 2026?

The Federal Reserve will announce its next interest rate decision tomorrow, January 28th. The overwhelming consensus is that rates will remain unchanged. That is likely to be the case at the Federal Reserve’s next meeting in March as well. Predicting markets currently place 84% odds that the Federal Reserve will leave rates unchanged in its March 16th meeting.

However, Federal Reserve Chair Jerome Powell’s term ends on May 15th, 2026. It’s expected that his replacement will be far more dovish and support rate cuts. If rate cuts are due in the second half of the year, here are a couple of stocks that could benefit handsomely.

Duke Energy: The Debt Refinancing Play

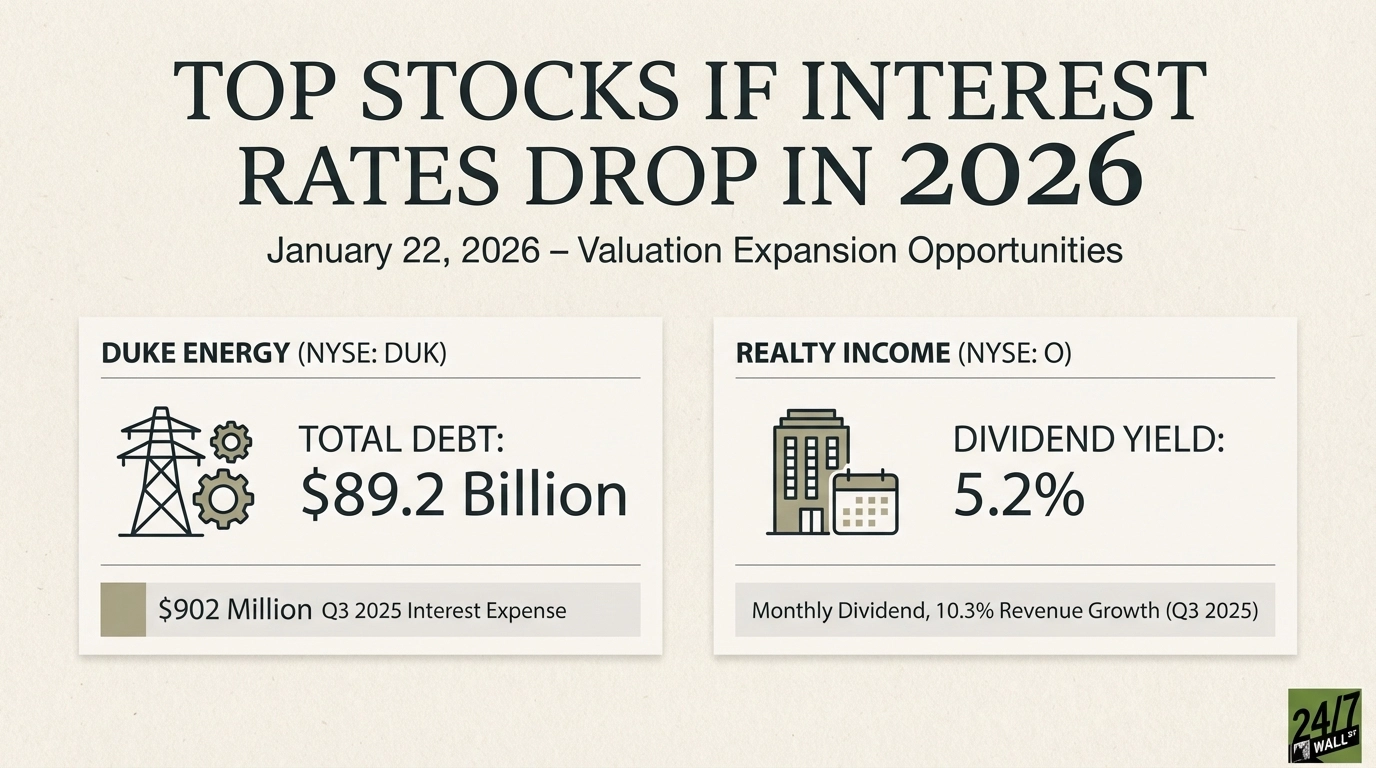

Duke Energy (NYSE:DUK | DUK Price Prediction) carries $89.2 billion in total debt against just $688 million in cash. That’s not a typo. The company’s interest expense hit $902 million in Q3 2025 alone. When you’re servicing nearly $1 billion in interest payments every quarter, even a 50 basis point rate cut translates to tens of millions in savings annually as debt rolls over.

The company generated $15.95 billion in EBITDA over the trailing twelve months with a 27% operating margin. That’s impressive for a regulated utility, but the real story is what happens when refinancing costs drop.

Duke serves 7.7 million customers across six states with a completely regulated business model. Revenue visibility is near-perfect. The company’s 3.51% dividend yield is slightly lower than current 10-year Treasury rates, and the company has increased dividends consistently for over two decades. The quarterly dividend jumped from $1.045 to $1.065 in 2025, a modest but reliable 1.9% increase that demonstrates management’s confidence.

With a beta of just 0.49, Duke won’t give you whiplash. But that’s the point. When rates fall, income investors rotate from bonds into dividend-paying stocks with defensive characteristics. Duke checks every box: stable cash flows, manageable payout ratio, and massive interest expense sensitivity that flows straight to the bottom line.

Realty Income: The Monthly Dividend Amplifier

Realty Income (NYSE:O) carries $28.9 billion in total debt against just $417 million in cash, with quarterly interest expenses of $287 million. The REIT’s 5.2% dividend yield becomes increasingly attractive relative to Treasury bonds as rates decline. The company generated $1.47 billion in revenue during Q3 2025, up 10.3% year-over-year, while maintaining its monthly dividend payment structure that has made it a favorite among income-focused investors. With a forward P/E of 39x compared to its trailing P/E of 58x, analysts anticipate improved earnings as refinancing opportunities emerge at lower rates.

Realty Income could be a particularly attractive option to investors who need reliable passive income as it has paid an incredible 667 monthly dividends (and counting) in a row.