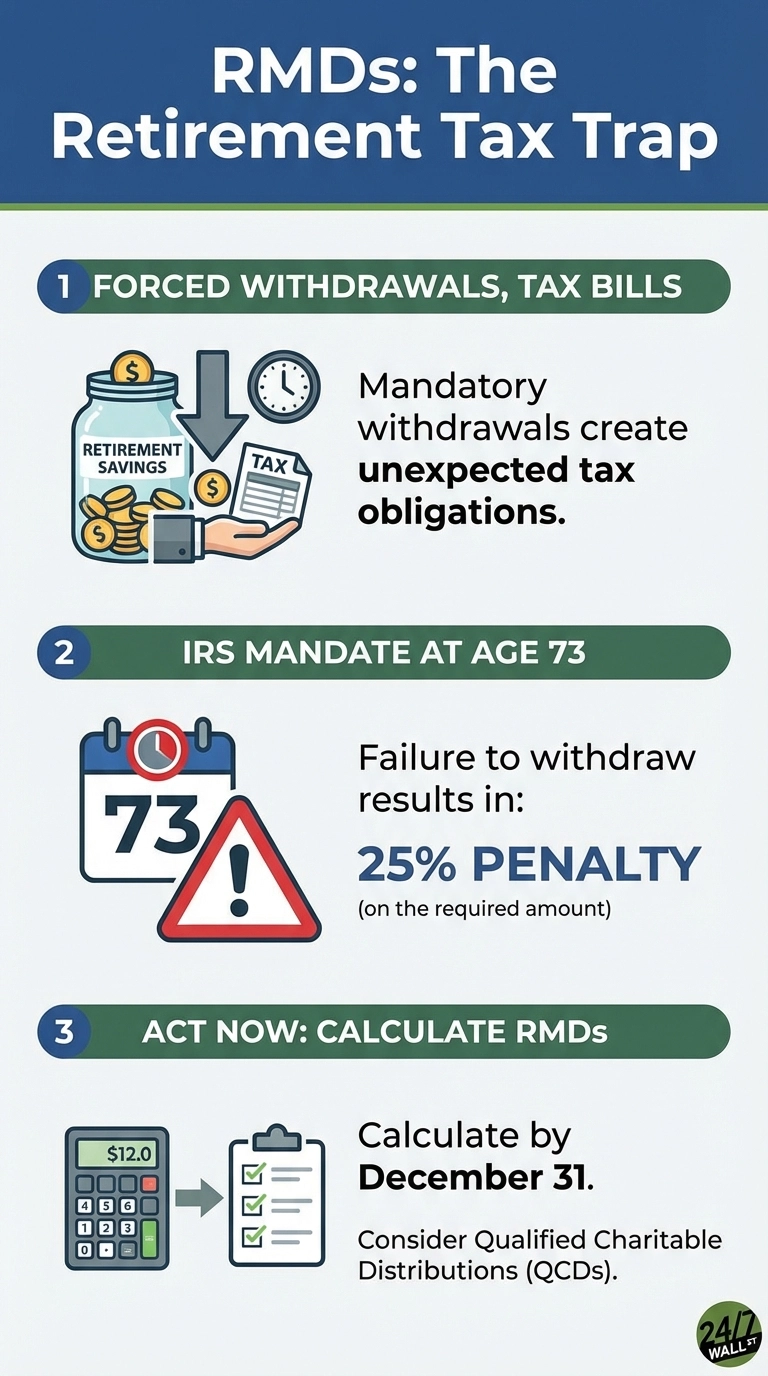

Retirees face a forced withdrawal problem many don’t understand until it hits their bank account. Required Minimum Distributions mandate withdrawals from tax-deferred retirement accounts starting at age 73. The IRS treats these withdrawals as ordinary income, creating unexpected tax bills for retirees who may not need the cash. Missing the deadline carries serious consequences—a penalty that can reach 25% of what you should have withdrawn.

The Situation: When you turn 73, the IRS requires withdrawals from traditional IRAs based on their life expectancy tables. These distributions become ordinary income on your tax return, creating tax obligations you must plan for in your retirement budget.

The tax impact varies by bracket, but the real danger is missing the deadline entirely. The penalty for a missed RMD is 25% of the required amount, and you still face the original tax obligation when you eventually take the distribution. Acting quickly to correct mistakes can reduce that penalty to 10% if you withdraw the shortfall within two years.

The Tax Trap That Drives the Cost

RMDs create a timing problem. You saved for decades in tax-deferred accounts, deferring taxes while working. Now the IRS wants its cut on a schedule it controls, not yours. Recent legislation has adjusted the starting age—currently 73 for most retirees, with further increases planned for younger savers. For anyone currently in their early seventies, the clock is running.

The penalty structure improved significantly under SECURE 2.0 legislation. Previously, missing an RMD meant facing a punishing 50% excise tax on the shortfall. The new rules cut that penalty in half to 25%, recognizing that many mistakes stem from confusion rather than willful neglect. Act quickly to correct errors within two years, and you can reduce the penalty further to just 10% by filing the proper forms with the IRS.

The real cost isn’t just the penalty—it’s forced income recognition you might not need, potentially pushing you into a higher tax bracket or affecting Medicare premiums. Large required distributions can trigger Income-Related Monthly Adjustment Amounts (IRMAA) surcharges that add hundreds per month to Medicare Part B and Part D costs.

Your Correction Options

If you miss an RMD, withdraw the shortfall immediately. Then file IRS Form 5329 with your tax return. The form calculates the excise tax but also lets you request a waiver by attaching a statement explaining reasonable cause, such as illness, adviser error, or account confusion. The IRS frequently grants waivers if you act quickly and demonstrate the failure wasn’t willful neglect.

What Matters Now

Calculate your RMD by December 31 each year using the IRS Uniform Lifetime Table. Your first RMD can be delayed until April 1 of the year after you turn 73, but that means taking two distributions in one tax year. Set a mid-year reminder to avoid year-end scrambling. If you don’t need the cash, consider Qualified Charitable Distributions, which satisfy the RMD without adding to taxable income.

This article is for educational purposes and does not constitute tax or financial advice. Consult a tax professional for guidance specific to your situation.