If you contribute to a 401(k), several rules governing your retirement savings changed over the past three years. The SECURE Act 2.0, signed into law in December 2022, introduced a staggered rollout of changes affecting when you must withdraw money, how much you can save, and whether those savings are taxed now or later.

Most workers don’t track legislative updates to retirement policy. But these changes shift the math on compounding, tax exposure, and withdrawal flexibility for millions of Americans saving through employer-sponsored plans.

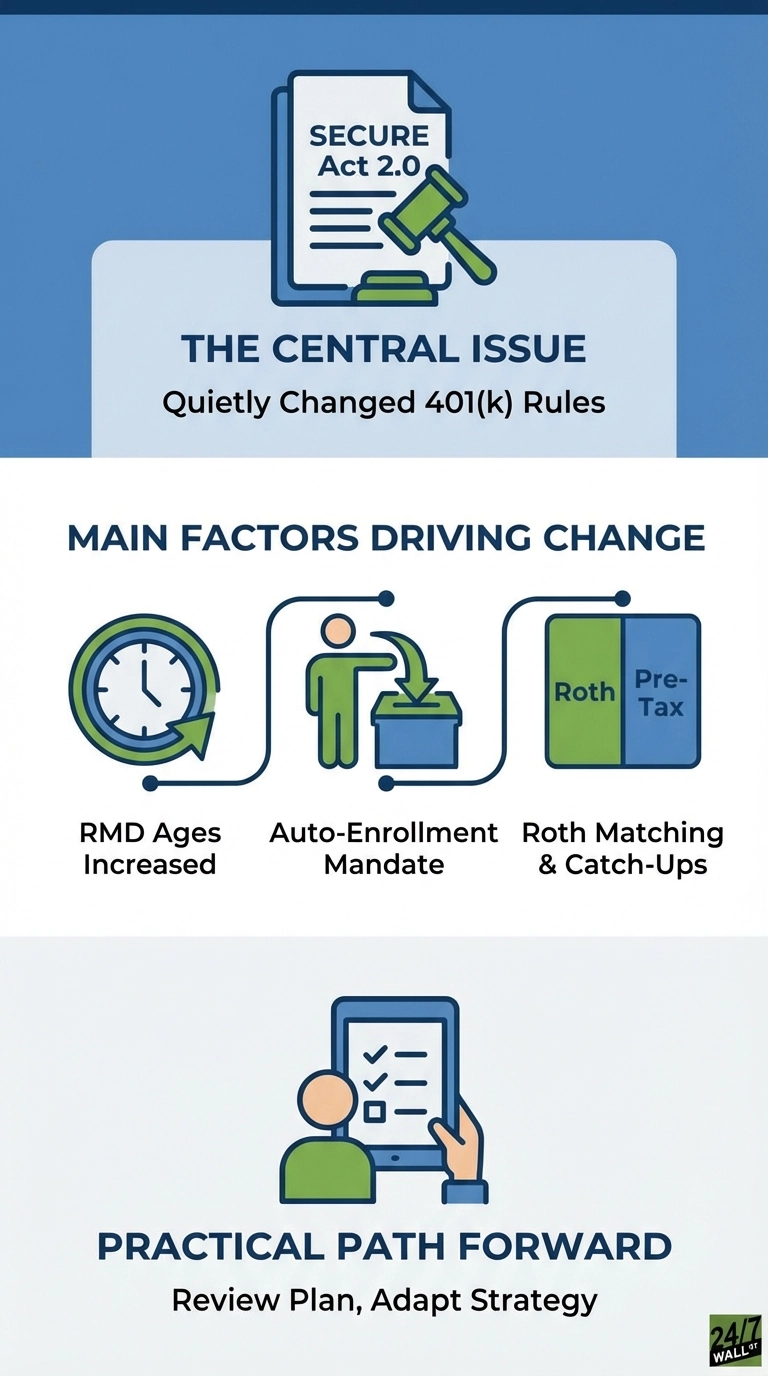

The RMD Age Moved, and Will Move Again

The age when you must start withdrawing from your 401(k) has shifted upward twice in recent years. What was once 72 became 73 in 2023, and will rise again to 75 in 2033 for younger savers. Each additional year of deferral allows your balance to compound tax-free longer, potentially adding tens of thousands in growth for workers with substantial savings.

The extended deferral period gives your savings more time to compound before withdrawals begin. A typical mid-career saver with a substantial balance could see tens of thousands in additional growth from just one extra year of tax-deferred compounding, illustrating why this seemingly small age adjustment matters for retirement outcomes.

SECURE 2.0 also eliminated RMDs entirely for Roth 401(k) accounts starting in 2024. Previously, Roth 401(k)s required withdrawals at the same age as traditional accounts, despite having already been taxed.

New Plans Must Auto-Enroll Workers in 2025

New retirement plans must now automatically enroll workers at a starting contribution rate between 3% and 10%, with annual increases until reaching the 10% threshold. This reverses decades of opt-in enrollment and addresses the behavioral reality that many workers never sign up despite intending to save.

Small businesses with 10 or fewer employees, companies less than three years old, and church or government plans are exempt. For everyone else, this shifts enrollment from opt-in to opt-out.

Catch-Up Contributions Got Bigger and More Complicated

The final years before retirement represent a critical window when many Americans realize they’re behind on savings but still have peak earning power. SECURE 2.0 recognizes this by offering workers aged 60-63 significantly larger catch-up contributions—roughly 50% more than the standard amount. However, starting in 2026, higher earners face a trade-off: anyone making over $150,000 must direct those extra contributions to Roth accounts, paying taxes now rather than getting the immediate deduction.

Employers Can Now Offer Roth Matching

SECURE 2.0 allows employers to make matching contributions to Roth accounts if the plan permits it. Previously, all employer matches went into pre-tax accounts regardless of whether the employee contributed to Roth or traditional.

Roth matches are taxable as income in the year received, but grow tax-free thereafter. This creates a new option for workers who prefer to pay taxes upfront rather than in retirement.

This article is for educational purposes and does not constitute personalized financial advice. Consult a tax professional regarding your specific situation.