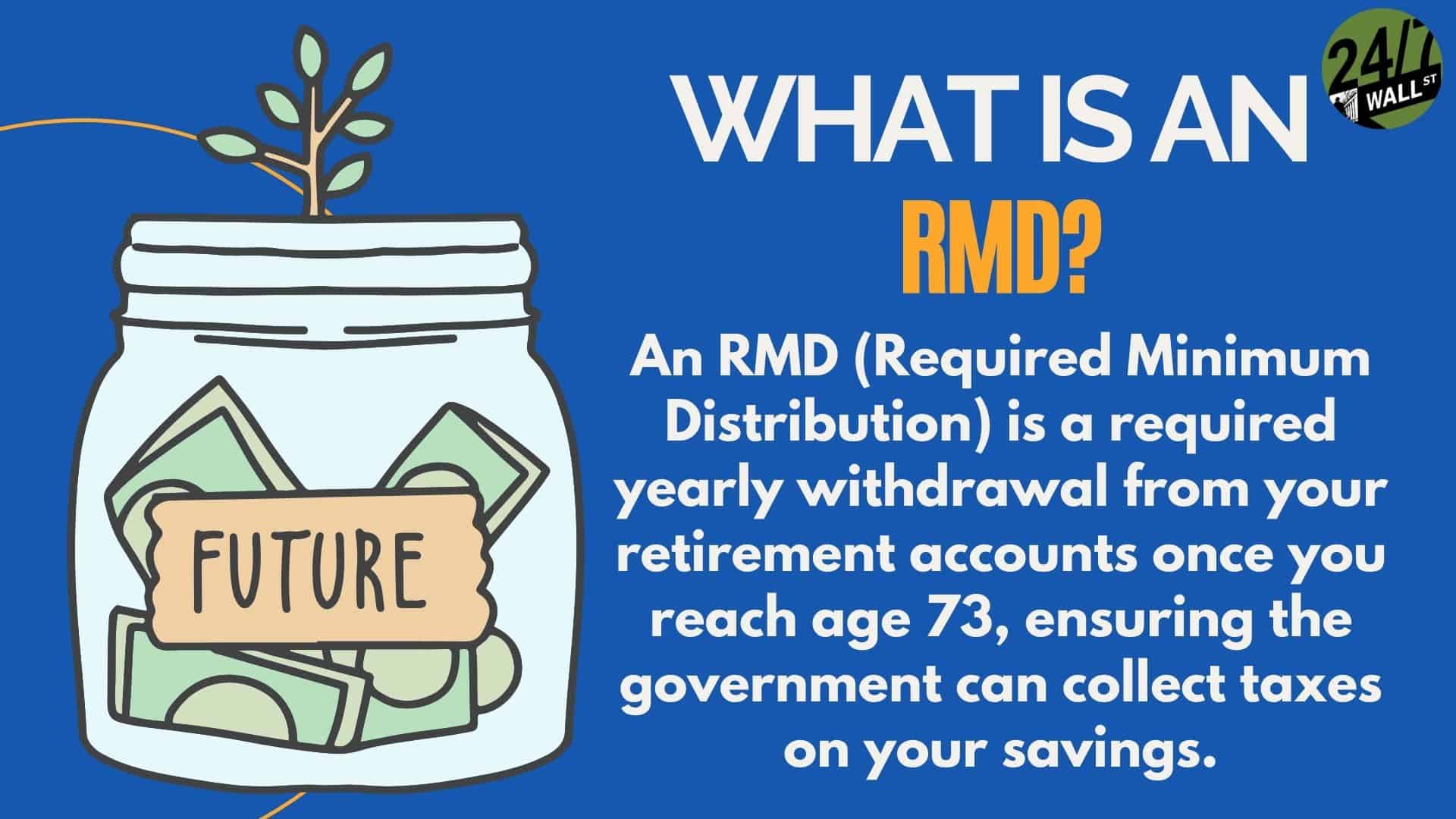

If you’re entering retirement, it’s essential to understand how required minimum distributions, or RMDs, work.

Tax-deferred accounts are subject to RMDs. That means the account holder must take a set amount of money from retirement accounts. However, RMDs are not required for Roth IRA, Roth 4301(k), and Roth 403(b) accounts for original owners.

So that there’s no confusion, or visits from your friendly neighborhood IRS agent, consult with an advisor before calculating.

Unless, of course, you’re a seasoned pro.

No. 1: Secure 2.0 Increased the RMD Age to 73

When we refer to Secure 2.0, we’re referring to legislation passed in late 2022 to expand retirement savings options. All of which helps make it easier for Americans to save by implementing features like automatic enrollment for new plans, adding penalty-free emergency withdrawals, and raising the age for Required Minimum Distributions (RMDs). It also aims to strengthen retirement security through enhanced catch-up contributions for older workers.

Under the new rules, if you were born before July 1, 1949, your RMD starts at the age of 70.5. If you were born between July 1, 1949, and December 31, 1950, you must pull by 72. If you were born between January 1, 1951, and December 31, 1959, the age to pull RMD is 73.

The goal is to give retirement savers more time for their money to compound before they’re forced to withdraw funds.

As noted by T. Rowe Price, “If you have multiple retirement accounts that are subject to RMDs, you must calculate the RMD for each account. However, you can make the actual withdrawal from any of your individual IRAs that are subject to RMDs, as long as the total withdrawal satisfies the total RMD amount required for that year.”

No. 2: Secure 2.0 Reduces RMD Penalty

Under the previous rules, missing an RMD resulted in a 50% penalty on the amount that should have been withdrawn. Now, it’s been reduced to 25%, which gives retirees more breathing room should they happen to miss an RMD.

In fact, according to the Internal Revenue Service, “If an account owner fails to withdraw the full amount of the RMD by the due date, the amount not withdrawn may be subject to an excise tax of 25%, 10% if the RMD is timely corrected within two years.”

No. 3: New Changes to RMD for Some Inherited Accounts

Secure 2.0 also modifies the rules for inherited IRAs and retirement plans.

Under the Secure Act of 2019, non-spouse beneficiaries were required to deplete inherited retirement accounts within 10 years of the account holder’s death. SECURE 2.0 still has this rule but offers new options for designated beneficiaries.

According to Pacific Life, “The IRS recently issued the final regulations for designated beneficiaries (DBs). This rule will impact DBs subject to the original Setting Every Community Up for Retirement Enhancement Act distribution rules, generally known as the 10-year rule. It specifically impacts them in the cases where IRA owners pass away on or after their required beginning dates (RBDs). In these situations, the beneficiary will not only have to drain the account by 12/31 of the year containing the tenth anniversary of the owner’s passing, but he/she also will need to take RMDs in the interim.”

Further information on this topic can be found on this IRS page.

No. 4: Secure 2.0 Increases Catch-Up Contributions

Starting January 1, 2025, individuals ages 60 to 63 can make catch-up contributions up to $10,000 a year to a workplace plan. The catch-up amount for people ages 50 and older is $7,500, but do go over that with a financial advisor.

In addition, according to Fidelity.com, “Starting in 2026, if you earn more than $145,000 in the prior calendar year, all catch-up contributions to a workplace plan at age 50 or older will need to be made to a Roth account in after-tax dollars. Individuals earning $145,000 or less, adjusted for inflation going forward, will be exempt from the Roth requirement.”

Here’s How to Figure Out Your RMD

It’s also important to know how to calculate your required minimum distribution, which you should discuss with your financial advisor.

The IRS uses a formula that includes your total account balances. It also includes your age, your life expectancy, and your beneficiary’s life expectancy.

The agency then divides the total balance by your life expectancy factor, which is the age to which you’re expected to live from your current age. For an example of how that works, here’s a link to the IRS Uniform Lifetime Table.

Even more information on RMD can be found on this IRS page.

If you’d rather avoid the IRS page, here’s how the calculation works.

Let’s say you’re 73 years old. You would have a Life Expectancy Factor of 26.5. If you have an account balance of $250,000 as of December 31 of last year, you would divide $250,000 by 26.5, which would give you your RMD of $9,433.96.

Again, be sure to check with your financial advisor.