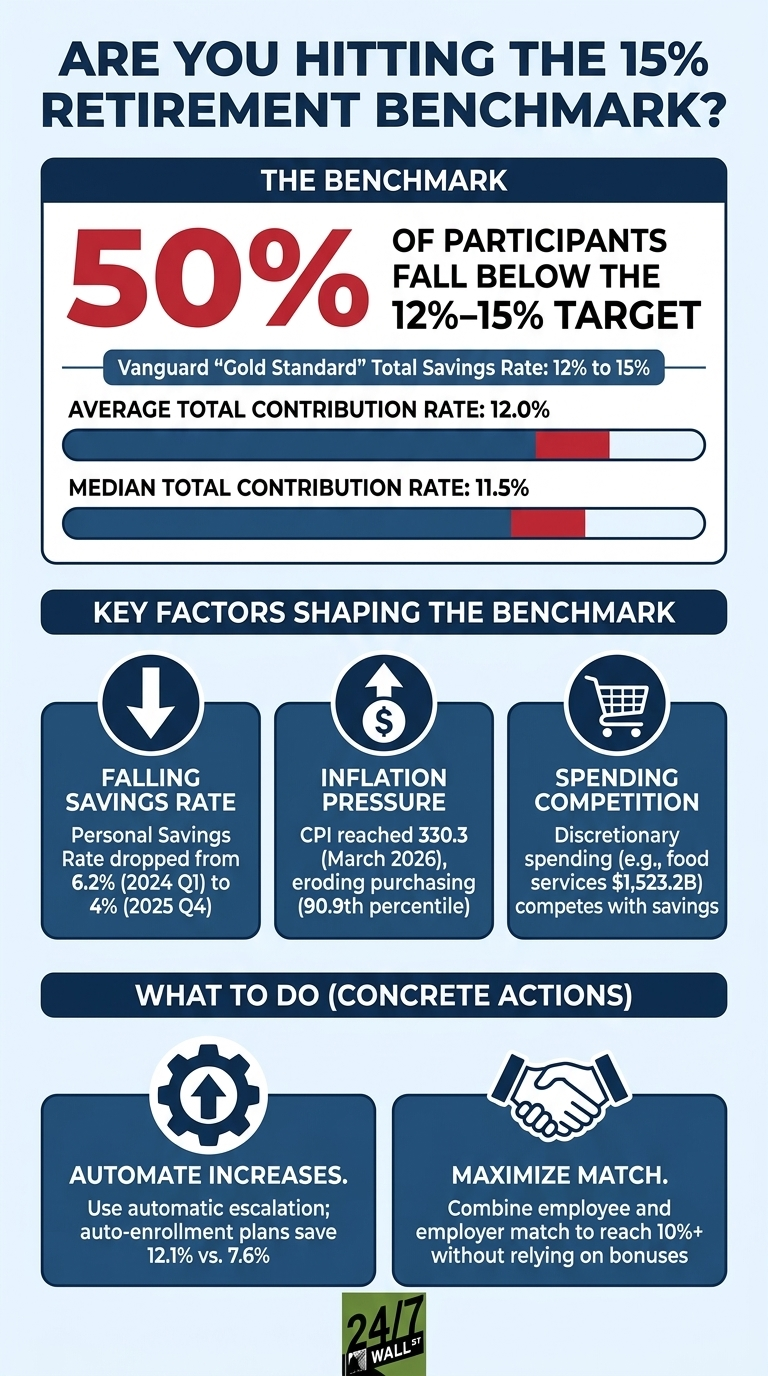

The retirement math for high earners has narrowed to a single question: whether high earners are putting away at least 15% of their income each year, including any employer match. Vanguard’s 2025 How America Saves report puts the “Gold Standard” total savings rate at 12% to 15%, with the higher end specifically aimed at workers earning more than $100,000. The average participant sits almost exactly at the floor of that range, leaving roughly half of savers below it.

The 12% Average Hides a 50% Shortfall

According to Vanguard’s 2025 report, the average total contribution rate, combining employee and employer dollars, is 12.0%, with a median of 11.5%. Because the average sits right at the bottom of the recommended zone, 50% of participants met or exceeded the 12% to 15% target, and the other half landed below it.

Why 15% Is the Benchmark for Higher Incomes

Where the Money Is Going Instead

Mechanics That Move Savers From 12% to 15%

Three mechanisms commonly close the distance between a 12% rate and the 15% target.

- Automatic escalation. Vanguard found that employees in automatic enrollment plans saved 12.1% on average, compared with 7.6% in voluntary plans. Furthermore, 69% of automatic enrollment plans include annual increases in deferrals. In 2024, 45% of all participants raised their deferral rate. A 1% annual auto-increase helps participants reach higher targets without needing to make an active decision each year.

- Full employer match. While many aim for a 15% total, the employer does much of the heavy lifting. The average employer contribution value across Vanguard plans is 4.3%. For a participant to reach the 15% gold standard, a common path involves a 10.7% employee deferral paired with that average 4.3% employer contribution.

- Tax-advantaged accounts and Roth conversions. With 86% of plans now offering a Roth feature, 18% of participants are using it to build tax-free wealth. For those who have already maxed out standard limits and need more room to reach a 15% total on a high income, 24% of plans offer after-tax 401(k) contributions. About 36% of plans also allow in-plan Roth conversions, which is a tool for participants looking to maximize their tax-advantaged space.