Live: Will Microsoft Soar After Earnings Tonight?

Quick Read

-

Microsoft (MSFT) reports Q2 fiscal 2026 earnings today after five consecutive quarterly beats. Capex hit $19.39B in Q1 for AI infrastructure. We’ll be updating this live blog the moment earnings hit the newwires shortly after 4 p.m. ET.

-

Azure growth must justify Microsoft’s massive capex outlays. Margin pressure from AI spending triggered a Stifel price target cut to $520.

-

Microsoft launched the Maia 200 AI chip to reduce NVIDIA reliance and compete with Google TPU and Amazon Trainium.

Live Updates

Microsoft Announces Q3 Guidance - Shares Fall

Microsoft just announced their Q3 guidance and shares are falling, now down close to 7%. Here’s what they had to say:

(The bottom line, the company’s revenue guide is very close to Wall Street estimates, which is putting additional pressure on company shares.)

Microsoft CFO Amy Hood

Now moving to our Q3 outlook, which unless specifically noted otherwise, is on a U.S. dollar basis. Based on current rates, we expect FX to increase total revenue growth by 3 points. Within the segments, we expect FX to increase revenue growth by 4 points in Productivity and Business Processes and 2 points in Intelligent Cloud and More Personal Computing. We expect FX to increase COGS and operating expense growth by 2 points. As a reminder, this impact is due to the exchange rates a year ago. Starting with the total company.

We expect revenue of USD 80.65 billion to USD 81.75 billion or growth of 15% to 17%, with continued strong growth across our commercial businesses, partially offset by our consumer businesses. We expect COGS of USD 26.65 billion to USD 26.85 billion or growth of 22% to 23%, and operating expense of USD 17.8 billion to USD 17.9 billion or growth of 10% to 11%, driven by continued investment in R&D, AI compute capacity and talent against a low prior year comparable.

Operating margins should be down slightly year-over-year. Excluding any impact from our investments in OpenAI, other income and expense is expected to be roughly $700 million, driven by a fair market gain in our equity portfolio and interest income, partially offset by interest expense, which includes the interest payments related to data center finance leases. And we expect our adjusted Q3 effective tax rate to be approximately 19%.

Next, we expect capital expenditures to decrease on a sequential basis due to the normal variability from cloud infrastructure build-outs and the timing of delivery of finance leases. As we work to close the gap between demand and supply, we expect the mix of short-lived assets to remain similar to Q2.

No Major News So Far

We’re about 25 minutes into the call and Microsoft’ CFO still hasn’t announced any forward-looking guidance. Satya Nadella did just announce figures for Copilot:

“Microsoft 365 Copilot also is becoming true daily habit with daily active users increasing 10x year-over-year. We’re also seeing strong momentum with researcher agent, which supports both OpenAI and Claude as well as agent mode in Excel, PowerPoint and Word. All up, it was a record quarter for Microsoft 365 Copilot seat adds, up over 160% year-over-year. We saw accelerating seat growth quarter-over-quarter and now have 15 million paid Microsoft 365 Copilot seats and multiples more enterprise chat users. “

Microsoft Earnings Call Starting

Microsoft’s earnings call has moved out of the generic investor relations disclosures and CEO Satya Nadella is talking.

Nadella begins describing the business as a ‘token factory.’ On the AI Investor Podcast, we’ve discussed the rise of AI Factories and it appears Microsoft is fully leaning into this concept.

3 Questions That Will Be Critical on Microsoft's Upcoming Conference Call

Microsoft’s conference call starts in about 10 minutes. Here are the key areas to watch:

- Guidance: What will Microsoft say about Q3? The Street expects revenue of $81.25 billion and EPS of $3.96 next quarter.

- Azure ‘Color’: One of the main metrics that is weighing down on Microsoft shares after-hours is Azure’s 39% growth rate, will the company offer an explanation for why growth came in slightly below expectations? Will Microsoft offer more long-term guidance on growth? In constant currency terms, Azure saw growth decelerate from the two most recent quarters.

- RPO Commentary: Microsoft is now showing $625 billion in remaining performance obligations and commercial obligations grew 230% from last year. What commentary will Microsoft provide on this massive OpenAI-fueled rise in backlog?

Meta Announces Massive Productivity Boosts on Its Call

We’re currently on Meta’s conference call and this comment caught our eye:

“We speak a lot about how AI is improving our products, but I’d like to take a moment to give an update on how it’s changing the way we work. Mark mentioned our focus on making Meta a place where individuals can have significant impact. A big focus of this is to enable the adoption and advancement of our AI coding tools where we’re seeing strong momentum. Since the beginning of 2025, we’ve seen a 30% increase in output per engineer with the majority of that growth coming from the adoption of agenetic coding, which saw a big jump in Q4. We’re seeing even stronger gains with power users of AI coding tools, whose output has increased 80% year-over-year. We expect this growth to accelerate through the next half.”

There have been massive advances in agentic coding in recent weeks an Meta is expecting productivity to surge beyond 80% in the second half of 2026. We’d expect Microsoft to trumpet similar efficiences that can cut down on operating costs.

We Will Provide Updates During Microsoft's Conference Call

If you want updates during Microsoft’s conference call leave this page open.

We will provide updates as Microsoft provides guidance. All you have to do is stay on this page and new updates should load automatically!

A Tale of Two Stocks: Microsoft Falls While Meta Rises 8%

While Microsoft shares are down 4.6% after-hours, Meta is now up 8.3%.

The big reason: revenue is accelerating into Q1. Meta is now forecasting 30% revenue growth next quarter and while its capital expenditure growth is massive (between $115 billion and $135 billion this year), the company aims to increase operating profits from 2026.

In Microsoft’s case: Wall Street is fretting over new disclosures around how much OpenAI is contributing to Azure growth and also Azure’s revenue coming in at 39%, which appears to be below Wall Street’s “whisper numbers” for the company’s cloud unit.

It’s an interesting divergence in how Wall Street is reacting to both stocks. We’ll see if the sell-off in Microsoft shares is tempered when they begin their conference call in 45 minutes.

Microsoft Q2 Earnings: Everything You Need to Know

MSFT | Microsoft Q2’26 Earnings Highlights:

- Adj. EPS: $4.14 [✅]; [UP] +24% YoY

- Revenue: $81.3B [✅]; [UP] +17% YoY

- Net Income: $38.5B [✅]; [UP] +60% YoY

Q2’26 Outlook:

- Released on the company’s conference call

Q2 Segment Performance:

- Productivity and Business Processes Revenue: $34.1B [✅]; [UP] +16% YoY

- Intelligent Cloud Revenue: $32.9B [✅]; [UP] +29% YoY

- More Personal Computing Revenue: $14.3B [❌]; [DOWN] -3% YoY

Other Key Q2 Metrics:

- Adj. Operating Income: $38.3B [✅]; [UP] +21% YoY

- R&D Expenses: $8.5B [✅]; [UP] +7% YoY

- Dividends Returned to Shareholders: $12.7B; [UP] +32% YoY

CEO Commentary:

- Satya Nadella: “We are only at the beginning phases of AI diffusion and already Microsoft has built an AI business that is larger than some of our biggest franchises. We are pushing the frontier across our entire AI stack to drive new value for our customers and partners.”

CFO Commentary:

- Amy Hood: “Microsoft Cloud revenue crossed $50 billion this quarter, reflecting the strong demand for our portfolio of services. We exceeded expectations across revenue, operating income, and earnings per share.”

Microsoft Shares Down 4.5%

Microsoft shares have been trading between down 4% and 7% since the company reported earnings.

Our note of caution: wait for the company’s conference call before drawing conclusions.

Microsoft will have plenty of commentary on Azure growth and will provide more forward guidance. Microsoft’s call is scheduled to begin at 5:30 p.m. ET.

More on RPO

Microsoft has disclosed that OpenAI is 45% of their RPO – which is backlog for their cloud computing division.

One of the biggest battles on Wall Street is who has exposure to OpenAI.

This extreme customer concentration could be shaping tonight’s reaction to Microsoft’s earnings.

Reasons Why Microsoft is Down

Why is Microsoft down despite soundly beating earnings? One explanation we mentioned earlier is that despite Azure growing 39% from last year, that number may have been disappointing.

While Wall Street has established ‘consensus’ figures, what money management firms (the “buy side”) is looking for often differs. That’s why NVIDIA will often drop despite topping consensus estimates. Their numbers miss the so-called ‘whisper number.’

It may be that the ‘whisper number’ for Azure was closer to 40%, making last quarter a relative disappointment. Microsoft will provide guidance for next quarter on its conference call, so we’ll see if shares make a big movement from where they sit right now.

Microsoft Stock Rebounding

And we’re beginning to see a rebound in Microsoft’s stock. Shares are now down less than 4% after dropping more than 7% earlier.

The quarter was very solid in our opinions and we were surprised by the initial 7% drop. We’ll continue digging into their earnings and providing insights.

More Figures on Microsoft's Quarter

Q2 capital expenditures came in at $37 billion.

RPO (a measure of backlog) increased 110%, which will likely command a lot of attention on the company’s conference call.

Remember that while the stock is down after hours, it had jumped 7% in the past week.

Meta Has Rebounded, Will Microsoft?

Meta shares plummeted initially after earnings despite beating earnings. Investors were concerned over massive capex spend.

Microsoft shares are still down about 6% after earnings. We’ll see if Microsoft’s stock rebounds after-hours as investors digest what the company just reported.

Azure Growth Looks Strong - But Was it Strong Enough?

Azure growth of 39% looks strong – but Wall Street’s expectations may have been slightly ahead of that number. We’ll continue digging into this.

Shares Now Down 7%

Microsoft is being punished after-hours.

EPS of $4.14 beats estimates of $3.92.

Revenue of $81.27 beats expectations of $80.28.

Earnings Are IN

Microsoft’s earnings are out – shares are immdiately down 5%.

The company beat EPS and revenue last quarter. We’ll give you more analysis shortly.

Earnings Will Hit Right After the Bell

We expect Microsoft’s earnings to hit right after the bell.

Key areas we’ll be watching include Azure growth rates and updates on capital expenditures into the back half of 2026.

Microsoft Shares Down Slightly in Late Trading

Microsoft earnings will be released right after the bell and we’ll begin updating this live blog. Shares are down very slightly in late trading as investors await results.

Microsoft (NASDAQ: MSFT | MSFT Price Prediction) reports second quarter fiscal 2026 earnings today after the bell. After five straight quarters of beating estimates, this report could reset expectations around AI infrastructure spending and Azure growth.

Strong Momentum Meets Rising Costs

Microsoft beat consensus in Q1 with EPS of $3.72 versus the $3.66 estimate. Revenue climbed 18.4% year over year to $77.67 billion, and operating margin held at 48.9%. Since that October report, shares rallied 107% over the past five years but underperformed across the last year with just a 7% gain while many other leading AI stocks soared.

However, the stock jumped 7% in the past week alone, driven partly by a BNP Paribas upgrade to $659 and buzz around the company’s new Maia 200 AI chip. That chip launch positions Microsoft to reduce reliance on NVIDIA and compete directly with Google’s TPU and Amazon’s Trainium processors. Analysts see this as a long-term competitive advantage, though near-term margin pressure remains a concern.

Consensus Estimates

| Metric | Q2 FY2026 Estimate | YoY Growth | Full Year FY2026 Estimate |

|---|---|---|---|

| EPS | $3.91 | +7.1% | $16.55 |

| Revenue | $80.28B | +15.3% | $327.0B |

All Eyes on Azure and Capex Guidance

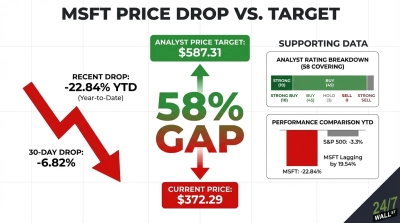

Investors will be watching how management frames AI infrastructure returns. Capital expenditures hit $19.39 billion in Q1, up sharply as Microsoft builds out data centers and custom silicon. Stifel recently cut its price target from $640 to $520, citing margin pressure from AI talent costs and compute spending, even while maintaining a Buy rating.

Azure growth is the critical metric. Analysts expect the Intelligent Cloud segment to drive expansion, supported by OpenAI partnerships and Azure Ignite innovations like Microsoft Foundry. The key question is whether consumption trends justify the massive capex outlays. Operating margin compression would signal that AI investments are eating into profitability faster than revenue can offset.

The market will also parse guidance closely. Morningstar analyst David Sekera warned that if AI spending forecasts don’t continue increasing, investors could face disappointment given elevated valuations. Microsoft trades at 30x forward earnings and 12x sales. Premium multiples demand premium execution.

Reddit sentiment heading into the report has been mixed. While the Maia 200 chip generated strong engagement on r/stocks (399 upvotes), earlier concerns about CEO Satya Nadella sounding “nervous” about AI sparked bearish sentiment in late January. Options traders appear cautious, with lower sentiment scores suggesting hedging activity.

Execution Over Excitement

After five consecutive beats averaging 5.5% above estimates, Microsoft has built credibility. But this quarter tests whether AI investments translate to sustainable margin expansion or just revenue growth with profitability headwinds. The company approved 15 new data centers in Wisconsin and continues expanding network partnerships, signaling confidence in long-term demand.

If Azure exceeds expectations and management provides confident capex guidance without margin erosion warnings, sentiment could shift quickly. If margins disappoint or guidance sounds cautious, the stock’s flat year-to-date performance could extend. This report either validates the AI infrastructure thesis or forces investors to recalibrate expectations around profitability timelines.

Eric Bleeker has been investing for more than 20 years. He began his career working at Microsoft before joining Motley Fool, one of the largest publishers of financial research. In his 15 years at Motley Fool Eric served as the General Manager for Fool.com and led coverage in the Technology & Telecom sector. In addition, he was a featured columnist and has hosted dozens of investing seminars attended by more than a million total investors. Eric has more than 1,000 financial bylines to his name and has been featured in The Wall Street Journal, CNBC, Fox Business, and many other leading publications. He is currently focused on artificial intelligence investing and is a CFA Charterholoder.

© 24/7 Wall St