Verizon Communications (NYSE:VZ | VZ Price Prediction) offers income investors a 6.9% yield, roughly double the S&P 500’s dividend return. The telecom giant has raised its dividend for 21 consecutive years, four years from Dividend King status. But the stock has underperformed the broader market in recent years. Is that 7% yield safe income or compensation for trouble brewing?

The Dividend Checks Out, Barely

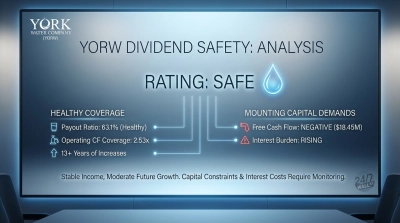

Verizon paid $11.2 billion in dividends during 2024 against $18.9 billion in free cash flow, producing a 59% payout ratio. That’s sustainable but not generous. The company generated $36.9 billion in operating cash flow and spent $18.0 billion on capital expenditures, covering the dividend 1.7 times over.

| Metric | 2024 | Assessment |

|---|---|---|

| Operating Cash Flow | $36.9B | Stable |

| Capital Expenditures | $18.0B | Elevated |

| Free Cash Flow | $18.9B | Adequate |

| Dividends Paid | $11.2B | 1.7x covered |

| FCF Payout Ratio | 59% | Tight but manageable |

The earnings-based payout ratio sits around 58%, using trailing twelve-month EPS of $4.69 against an annual dividend of $2.72. These ratios are borderline for a mature business. Verizon can maintain the dividend but has limited cushion for aggressive growth.

The Debt Load Is the Real Problem

Verizon carries $170.5 billion in total debt, producing a debt-to-equity ratio of 1.6x. That’s improved from 2.2x in 2020 but still represents a massive obligation. Interest expense nearly doubled from $3.6 billion in 2022 to $6.7 billion in 2024 as rates rose. That’s $6.7 billion annually that can’t go to dividends or growth.

| Metric | Current | Assessment |

|---|---|---|

| Total Debt | $170.5B | Elevated |

| Debt-to-Equity | 1.6x | Moderate |

| Interest Expense (2024) | $6.7B | Rising fast |

| Net Debt-to-EBITDA | 3.2x | Manageable |

Net debt-to-EBITDA sits at 3.2x, manageable but leaving little room for error if earnings decline. The $20 billion Frontier Communications acquisition adds more debt and capital commitments ahead.

Aristocrat Status Matters

Management values that 21-year dividend increase streak. Cutting the dividend would trigger institutional selling and crater the stock. That cultural commitment provides protection but creates risk. Companies that hold dividends too long often cut deeper when forced to act.

Recent increases have been modest. The dividend grew 2.7% in 2025, 2.4% in 2024, and 2.2% in 2023, barely keeping pace with inflation. The company prioritizes safety over growth.

This Dividend Is Safe, But Dead Money

Dividend Safety Rating: Safe

The 7% yield appears sustainable based on current cash flows and management’s commitment to the aristocrat streak. Free cash flow covers the dividend 1.7 times, and the balance sheet, while leveraged, isn’t in crisis. Verizon hasn’t missed a payment in decades.

But you’re buying an income stream, not a growth story. The stock has shown limited price appreciation because the business is mature, capex needs are high, and T-Mobile (NASDAQ:TMUS) is taking share. Verizon works for income if you need reliable cash flow and can accept zero capital appreciation. Be cautious if competitive pressures worsen or debt refinancing costs spike further. This isn’t too good to be true. It’s exactly what it looks like: a high yield from a low-growth utility facing structural headwinds.