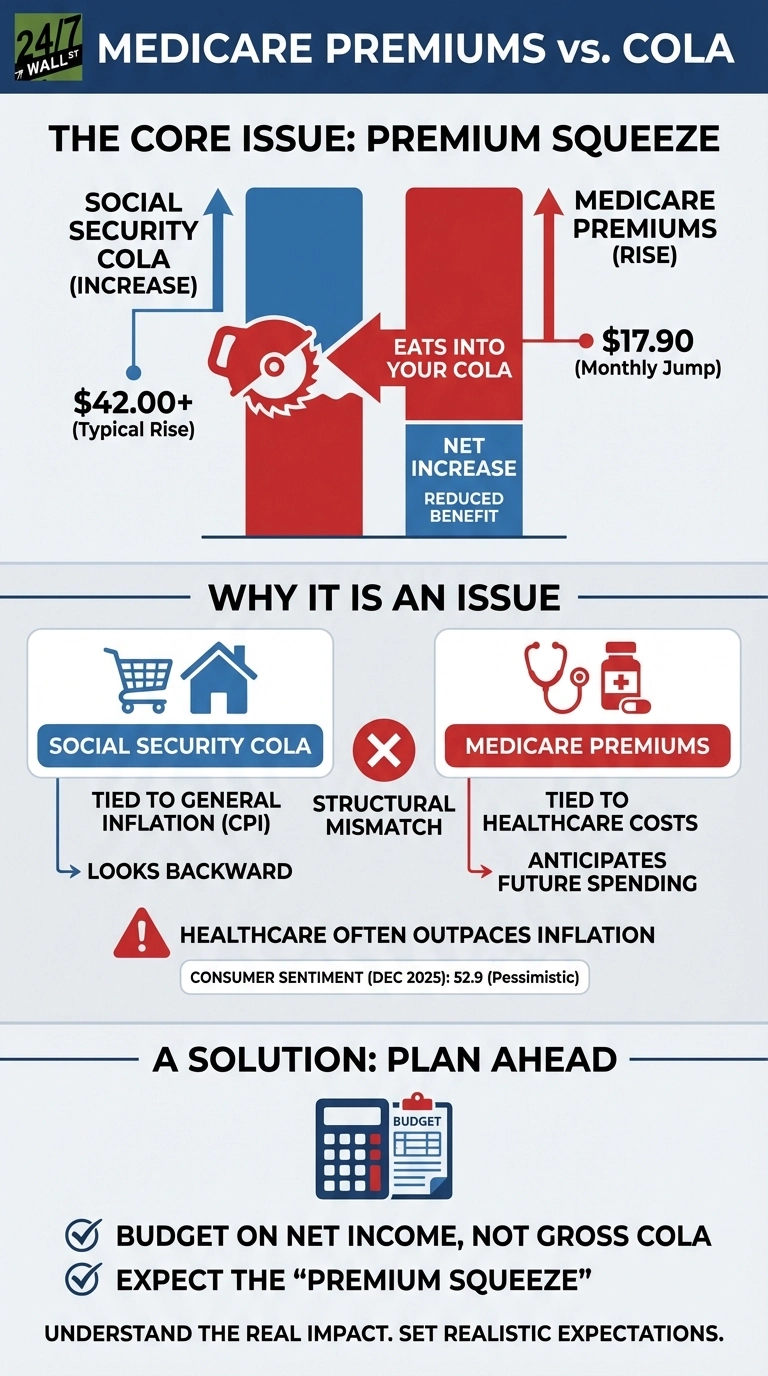

When Social Security announced its 2026 cost-of-living adjustment, many retirees expected meaningful relief from inflation. Instead, Medicare Part B premiums jumped by $17.90 per month, consuming much of the increase before retirees saw any benefit. This pattern of healthcare costs rising faster than income adjustments creates a persistent squeeze on fixed-income households.

This disconnect surprises people because both adjustments happen simultaneously each January, yet they measure fundamentally different economic forces. Social Security looks backward at general inflation trends, while Medicare premiums must anticipate future healthcare spending. The result is a structural mismatch where retirees’ income adjustments rarely keep pace with their largest expense category.

Why Healthcare Costs Move Independently

Medicare premiums track healthcare inflation, not the broader Consumer Price Index that determines Social Security COLAs. Medical care costs consistently outpace general inflation due to expensive new treatments, an aging population requiring more services, and rising prescription drug prices. Medicare premiums rise to cover projected healthcare spending, including physician services and medical equipment costs. Administrative intervention helped contain the 2026 increase—without action to curb spending on certain treatments, retirees would have faced an even steeper jump.

Most retirees don’t realize Medicare premiums are recalculated annually based on expected program costs for the coming year. Social Security uses trailing inflation data from the third quarter of the previous year, creating a structural mismatch. One measures what happened; the other estimates what’s ahead.

Planning Around the Premium Squeeze

This dynamic matters most for retirees relying heavily on Social Security with limited savings. When premiums claim a larger share of the COLA, purchasing power erodes even as the nominal benefit rises. The impact scales with benefit levels—higher earners retain more of their increase, while those with smaller checks see a greater percentage consumed by Medicare costs.

Recent consumer sentiment data reflects this strain. As confidence measures declined through late 2025, the pattern revealed how retirees on fixed incomes feel the squeeze when essential costs outpace their income adjustments.

Understanding this mismatch helps set realistic expectations. COLA announcements represent gross increases, not what lands in your bank account. For Medicare enrollees, the headline number overstates the benefit. Small differences compound over time, making it essential to budget based on net increases rather than the percentage Social Security advertises each fall.