Financial advisor, author and podcast host Suze Orman has issued a stark warning to retirees: Your Social Security check is disappearing faster than you think, and the primary culprit might be part of your daily routine.

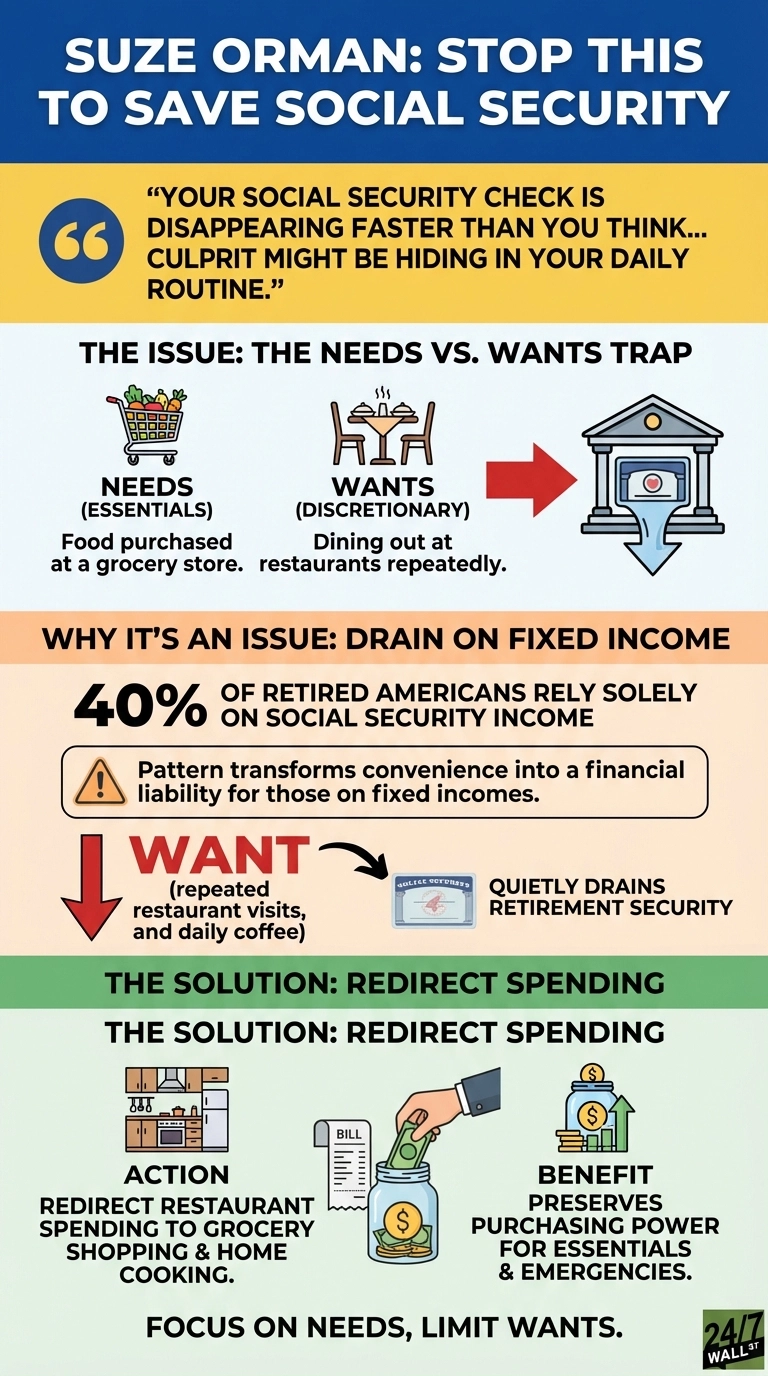

With 40% of retired Americans relying solely on Social Security income — with an average benefit check of about $2,071 per month, there’s little room for error. Yet millions are making one costly mistake that’s quietly draining their retirement security.

The Needs vs. Wants Trap

Orman’s message is direct: Retirees must learn to distinguish between needs and wants. A need is food purchased at a grocery store. A want is dining out at restaurants repeatedly — a pattern that transforms convenience into a financial liability for those on fixed incomes.

The numbers reveal how devastating this habit can be. Consider a retiree who dines out regularly and grabs daily coffee — a routine that can quietly drain over $4,900 annually. This represents more than a quarter of the average Social Security benefit, transforming what seems like harmless convenience into a structural threat to retirees’ financial security.

Americans Are Eating Themselves Into Debt

The problem extends beyond retirees. Many American adults demonstrate willingness to finance discretionary spending on dining and entertainment, creating a dangerous precedent that follows workers into retirement and undermines long-term financial stability.

Economic data supports Orman’s concern about declining financial discipline. The average U.S. personal savings rate has plummeted from 5.2% in early 2025 to just 3.5% by November 2025. This means Americans now save less than four cents of every $1 earned, leaving minimal cushion for emergencies or unexpected expenses.

Meanwhile, retail sales in 2025 continued their upward march, reaching between $5.42 trillion and $5.48 trillion, a 3.2% year-over-year increase from 2024. That pattern reveals a troubling disconnect: Discretionary spending accelerates even as the financial cushion evaporates, creating vulnerability for those approaching or already in retirement.

The divergence between declining savings and rising retail spending illustrates the financial discipline crisis Orman warns about: Americans are prioritizing immediate consumption over long-term security.

What Retirees Should Do Instead

Orman’s advice centers on redirecting restaurant spending toward grocery shopping and home cooking. The math is straightforward: A home-cooked meal costs roughly $8 in ingredients compared to $20 at a restaurant. That $12 difference, repeated consistently throughout the year, preserves nearly $2,000 in purchasing power, which is enough to cover unexpected healthcare costs, handle home repairs or build the emergency fund most retirees lack.

For those already in retirement with limited savings, financial experts emphasize that having any retirement savings provides more security than having none, even if it means adjusting expectations about lifestyle and discretionary spending.

The broader context matters. With headline inflation running at 2.7% year-over-year as of December 2025, Social Security’s cost-of-living adjustments, or COLAs, may not keep pace with actual household expenses, particularly for retirees spending heavily on restaurant meals, which typically inflate faster than groceries (4.1% versus 2.4%, respectively, in December 2025).

Orman’s warning isn’t about eliminating all dining out. It’s about recognizing that repeated restaurant visits represent a structural drain on fixed income. For retirees living on $1,913 monthly, every dollar redirected from wants to needs extends financial security. The question isn’t whether you can afford one meal out. It’s whether you can afford the pattern.