Live: Will Bloom Energy Soar After Earnings Tonight?

Quick Read

-

Bloom Energy (BE) reports Q4 results tonight after a 469% gain over the past year. We’ll be updating this live blog with news and analysis the moment Bloom Energy’s earnings go live. Simply stay on this page and new updates will load automatically below.

-

Microsoft, Google, Amazon and Meta plan over $250B in 2026 infrastructure spending. Bloom Energy’s forward guidance matters more than Q4 results.

-

Bloom Energy trades at 196x forward PE with a $34.85B market cap and must prove it can execute at scale.

Live Updates

Bloom Shares Now in the Red

Well, we called it, Bloom shares are now down 2%.

Sell it off 40% tomorrow for all I care, would love to pick up shares on such an exceptional company at a massive discount.

Just remarkable – while every hyperscaler is increasing capex estimates 15% to 30% over already hyper bullish estimates, the reaction is to sell off suppliers?

I’m happy to take the opposite side of this bet as the dust clears.

Bloom Gains Fade

It’s an incredibly tough market for growth stocks, so its not ‘surprising’ that Bloom’s gains are fading.

The company’s call is still on going, but there was just a massive drop in Bloom’s share price.

It’s hard to say what caused it, there was a question about Oracle warrants (and Oracle is currently absolutely toxic in the market), so maybe the market didn’t like that.

Yesterday American Superconductor issued great earnings and was up 25% after-hours, by noon shares were negative.

By the close they were down 6%.

After hours tonight they’re down another 3%.

It’s just the current market sentiment (panic?) that’s taken over. I’d be surprised to see Bloom’s shares in the green tomorrow morning.

That says less about their fantastic results and more about current sentiment.

Bloom's Conference Call Highlights New Geographic Hotspots

Bloom’s conference call noted how demand is moving from California and the Northeast into new regions.

Of course, this speaks to rabid datacenter demand and the company’s shifting value proposition:

“The geographic mix of our U.S. backlog is noteworthy. 2 years ago, over 80% of our U.S. backlog was composed of installations in California and the Northeast, traditionally, the high cost of power states. But this year, over 80% of our backlog comes from other states with lower power costs. This geographic shift highlights 2 important dynamics at play: first, companies are locating factories and data centers in states where they can quickly secure reliable and affordable power either from the grid or on site.

The states where we are growing fastest, have robust natural gas infrastructure and favorable regulatory and policy frameworks for on-site power generation; second, in these states with lower power costs, Bloom is cost competitive, our value proposition, fast time to power, higher reliability and lower emissions strongly resonates for our customers.”

In short, Bloom Energy’s future is now in Texas.

Bloom Energy's CEO Discusses AI Demand on the Company's Conference Call

Here’s what Bloom’s CEO had to say about AI demand on the start of the company’s conference call:

“Good afternoon, and thank you for joining us today. Bloom is rapidly becoming the standard for on-site power as evidenced by our excellent fourth quarter, capping our best year act. We delivered record revenue, gross margin and operating margin for the year. Our product backlog increased 140% year-over-year to about $6 billion. Our Service business has been profitable for 8 quarters in a row. And in the fourth quarter, we achieved 20% gross margin in Service with around $14 billion of Service backlog and a growing product backlog that is 100% attached to service.

Bloom is well positioned for durable growth in Service revenue and profits in the years ahead. Our growth has been fueled by seismic changes in customer attitudes towards power, Bring Your Own Power has become the mantra for data centers and power hungry factories. On-site power has moved from being a decision of last resort to a vital business necessity. This shift has led large power users to seek Bloom to fulfill their needs. Our demand from data center and commercial and industrial or C&I customers is secular and growing in 2026, we will further invest in our commercial team to capitalize on growing sales opportunities.

AI is a huge tailwind for the power industry and a big catalyst for Bloom’s growth. The backlog we reported today includes half a dozen hyperscale and neo cloud end customers compared to just 1, a year ago. Bloom has a master contract structure to enable these customers to keep returning to us for repeat orders, much as we have expanded with our C&I customers. And we are also experiencing surging demand in our C&I business. C&I backlog grew over 135% year-over-year, and it consists of several verticals: telecom; manufacturing; logistics; retail; health care; and education; digitization; automation; electrification; and reshoring are driving C&I customers to seek on-site power. And our C&I sales pipeline is stronger than ever.”

Bloom Energy's Conference Call is Starting Now

If you want updates leave this page open, we’ll post updates as it goes.

Bloom Earnings In Summary

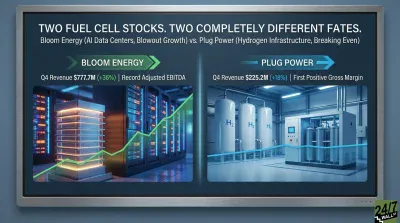

Bloom Energy’s 8.8% after-hours surge following its Q4 earnings beat appears measured given the fundamentals. The company delivered $0.45 EPS versus $0.30 expected and $777.7M revenue versus $671.7M consensus—a significant 41% earnings beat paired with 16% revenue outperformance.

What justifies caution: The stock already rallied 44% over the past month and trades at 196x forward earnings, pricing in substantial growth. The broader clean energy sector (ICLN) has pulled back 2.2% this week, creating headwinds.

What supports the move: Management’s $3.1-3.3B revenue guidance for 2026 implies over 50% growth from the $2.02B FY2025 revenue. The $20B total backlog and $418M Q4 operating cash flow validate execution capability in AI infrastructure power demand.

The reaction appears rational, not euphoric—appropriate for a high-beta name delivering transformational guidance in a risk-off market.

The Need to Know Figures from Bloom Energy's Q4 Earnings Release

BE | Bloom Energy Q4’25 Earnings Highlights:

- Adj. EPS: $0.45 (Est. $0.30) [✅];

- Revenue: $777.7M [✅]; [UP] +35.9% YoY

- Adj. Gross Margin: 31.9% [✅]; [DOWN] -7.4 bps YoY

- Free Cash Flow: $418.1M; [UP] +86.5% YoY

- Operating Income: $87.5M; [DOWN] -16.4% YoY

2026 Outlook:

- Revenue: $3.1B – $3.3B (Est. $2.57B) [✅]

- Bloom Energy anticipates continued growth driven by demand in the AI data center industry and commercial & industrial sectors.

- Strategic investments are expected to enhance operational efficiency and product offerings.

Q4 Segment Performance:

- Product Revenue: $638.5M; [UP] +35.3% YoY

- Installation Revenue: $67.3M; [UP] +86.5% YoY

- Service Revenue: $61.7M; [UP] +14.0% YoY

- Electricity Revenue: $10.2M; [DOWN] -5.3% YoY

Other Key Q4 Metrics:

- Adj. Operating Income: $132.9M; [UP] +0.4% YoY

- Adj. Operating Expenses: $115.0M; [UP] +20.5% YoY

- R&D Expenses: $55.9M; [UP] +41.5% YoY

- Effective Tax Rate: 40.0% (vs. 1.0% YoY)

- Cash and Cash Equivalents: $2.5B; [UP] +205.5% YoY

- Current Backlog: ~$20B; [UP] +150% YoY

CEO Commentary:

- KR Sridhar: “Bring-your-own-power has shifted from a slogan to a business necessity for AI hyperscalers and manufacturing facilities. This shift is secular and growing. We have built a solid state digital power platform for the digital age that is superior to any legacy solution.”

CFO Commentary:

- Maciej Kurzymski: “Fourth quarter reflects the progress we are making on the fundamentals—reducing product cost, driving operating leverage, and executing with discipline and consistency. We are confident in our trajectory and the strategic investments that position Bloom for accelerating growth.”

[Estimates fetched from AlphaVantage]

Full Year Guidance

Bloom issued full year guidance of $3.1 billion to $3.3 billion.

That is significantly ahead of Wall Street’s expectations of $2.57 billion.

Gains Holding at 10%

Bloom Energy has to issue an absolutely massive beat to see gains as the market continues selling off any uncertainty this earnings season and the company delivered.

Shares were originally up 15% but have fallen back to about 10%.

We’ll post more thoughts on Bloom momentarily, simply leave this blog open to keep receiving updates as we scan their earnings.

Bloom Shares Skyrocketing - Up 15% Right After Earnings Release

Bloom Energy just reported earnings. Here’s the headline figures:

- EPS:$.45

- Revenue: $777.7M

As a reminder, here’s what Wall Street expected:

- EPS: $.30

- Revenue: $645.3M

Still No Earnings

We’re still waiting on Bloom’s earnings. It’s worth noting that Super Micro had very delayed earnings this week and still issued a significant beat, so I wouldn’t read too much into the delay.

Still no earnings from Bloom...

We’re still waiting for Bloom earnings and will update when they cross newswires.

Earnings Expected at 4:05 p.m. ET

We expect Bloom Energy earnings to drop shortly after the closing bell. Here’s what you need to do to get prepared:

- Know the numbers to watch: Wall Street expects revenue of $645 million and EPS of $.30.

- Stay on this live blog for updates: We’ll be posting news and analysis right after earnings drop, simply stay on this live blog and new updates should appear automatically.

- Check out the AI Investor Podcast: Make sure to subscribe to our AI Investor Podcast to get all the biggest news and stock recommendations delivered to your favorite podcast player. On our next episode we’ll be issuing 10 to 15 new buy ideas, and Bloom Energy could be among them!

Bloom Energy Shares Hammered Today

Yesterday saw one of the largest momentum sell-offs of the 21st century as investors rotated out of risk.

The sell-off is continuing today. Bloom shares are down another 8.5% in late trading.

The message is pretty clear, Bloom will need to deliver exceptional earnings or could see a dramatic sell-off tomorrow. The market has been absolutely punishing growth stocks that deliver anything but perfection this past week.

Bloom Energy (NYSE: BE) reports fourth-quarter 2025 results tonight after the bell. After landing a 900 MW AI power fuel cell deal and riding a wave of hyperscaler infrastructure spending, this report will show whether the company can convert momentum into sustained execution.

Expected Results

Here’s what Wall Street expects tonight:

- Adjusted EPS: $.30

- Revenue: $645 million

And Q1 figures are currently projected at:

- Adjusted EPS: $.07

- Revenue: $464.2 million

The company said they expect to beat their full-year guidance during their Q3 conference call – $1.65 billion to $1.85 billion in revenue and approximately 29% non-GAAP gross margin.

Wall Street is currently expecting 2025 revenue of $1.9 billion, so that ‘beat’ has been priced in.

Management has hinted at a strong finish, noting that “based on what we see today, we expect 2025 to be better than our previously stated annual guidance.”

Recent Share Performance

Shares have surged 59% year-to-date and 469% over the past year, trading at about $136 in late trading today.

The stock hit $176.49 in recent months before pulling back over the past week. When the company reported Q3 results on October 28, 2025, it beat estimates handily with $0.15 EPS versus $0.10 expected and revenue of $519 million versus $439 million expected. That marked the fourth consecutive quarter of profitability and beats after a rocky 2024.

Key Areas Wall Street Is Watching

I’ll be watching order book strength and new contract wins. CEO K.R. Sridhar said on the Q3 call that “commercial momentum is clearly accelerating and it’s palpable… It’s accelerating not just in AI, our traditional commercial and industrial segments are doing the same.”

Revenue guidance for 2026 matters more than Q4 results. Hyperscalers just announced massive CapEx increases. Microsoft, Google, Amazon, and Meta are collectively spending over $250 billion on infrastructure in 2026. If Bloom can’t translate that into aggressive forward guidance, the AI power thesis weakens fast.

Gross margins need to hold or expand. The company posted 30.4% gross margin in Q3, up 510 basis points year-over-year. Management has delivered double-digit product cost reductions annually for over a decade. If margins slip, it signals pricing pressure or execution issues.

Capacity expansion is the final piece. The company is doubling manufacturing capacity to 2 gigawatts by December 2026. Sridhar promised they’d “never be the constraint to our customer on growing their data center.” If demand is as strong as management claims, we should see concrete plans to expand beyond 2 GW in the not-so-distant future.

Why It Matters

This is the quarter where Bloom either proves it can scale with AI infrastructure spending or reveals it’s just riding a hype cycle. The company has the technology advantage with its 800-volt DC architecture that competitors can’t match.

The question is whether they can execute on the pipeline fast enough to justify a $34.85 billion market cap and 196x forward PE ratio. Tonight’s guidance will tell us if the AI power story is real or if we’re pricing in perfection that won’t arrive.

Eric Bleeker has been investing for more than 20 years. He began his career working at Microsoft before joining Motley Fool, one of the largest publishers of financial research. In his 15 years at Motley Fool Eric served as the General Manager for Fool.com and led coverage in the Technology & Telecom sector. In addition, he was a featured columnist and has hosted dozens of investing seminars attended by more than a million total investors. Eric has more than 1,000 financial bylines to his name and has been featured in The Wall Street Journal, CNBC, Fox Business, and many other leading publications. He is currently focused on artificial intelligence investing and is a CFA Charterholoder.

© 24/7 Wall St